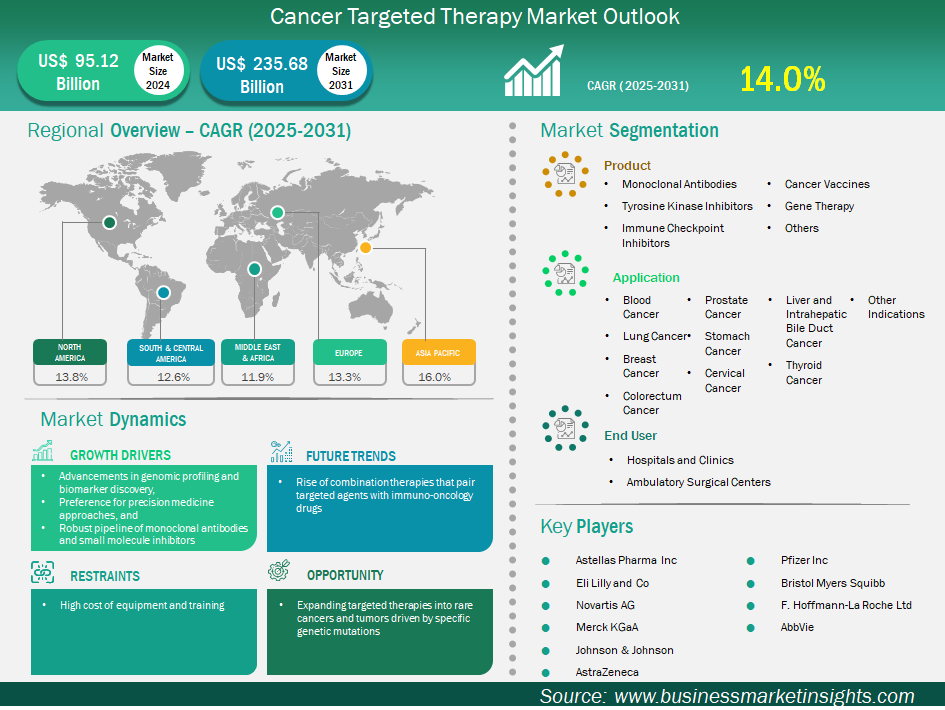

The Cancer Targeted Therapy Market segmentation framework, as detailed in this Cancer Targeted Therapy Market Report, provides a comprehensive and clinically structured view of the industry across three key dimensions: therapy type, indication, and end-user. This segmentation enables stakeholders to identify the most commercially significant targeted therapy categories, understand the clinical evidence and regulatory approval drivers behind segment leadership, and align product development and market entry strategies with the highest-value growth opportunities across the global precision oncology market. The market is valued at US$ 95.12 billion in 2024 and is forecast to reach US$ 235.68 billion by 2031 at a CAGR of 13.84%.

Request Sample Pages of this Research Study @ https://www.businessmarketinsights.com/sample/BMIPUB00031706

By Therapy Type

The therapy type segment covers monoclonal antibodies, tyrosine kinase inhibitors, immune checkpoint inhibitors, cancer vaccines, gene therapy, and others. Monoclonal antibodies dominated in 2024 through their ability to specifically bind target antigens on cancer cells with agents including trastuzumab, bevacizumab, and rituximab as standard of care. AbbVie's telisotuzumab vedotin (Emrelis) is an antibody-drug conjugate within the monoclonal antibody category combining targeting precision with cytotoxic payload delivery. Tyrosine kinase inhibitors serve the large EGFR, ALK, and BRAF mutation-positive cancer populations. Immune checkpoint inhibitors represent the fastest-growing category. Gene therapy represents the highest-innovation frontier segment.

By Indication

The indication segment covers blood cancer, lung cancer, breast cancer, colorectum cancer, prostate cancer, stomach cancer, cervical cancer, liver and intrahepatic bile duct cancer, thyroid cancer, and others. Lung cancer held the largest share in 2024 through high incidence of actionable genetic mutations including EGFR, ALK, and ROS1, with both AbbVie's Emrelis c-Met NSCLC approval and the broad EGFR TKI market making lung cancer the most targeted therapy indication globally. Breast cancer is the second largest through trastuzumab, pertuzumab, and Eli Lilly's Verzenio expanded indication addressing HER2-positive and hormone receptor-positive populations.

By End-User

The end-user segment covers hospital pharmacies, retail pharmacies, and online stores. Hospital pharmacies dominated in 2024 through specialized handling requirements and IV delivery modes of most cancer targeted therapies requiring clinical administration settings.

Frequently Asked Questions

Which therapy type leads the Cancer Targeted Therapy Market? Monoclonal antibodies dominated in 2024 for their broad applicability across cancer types with established agents including trastuzumab, bevacizumab, and rituximab as standard of care, and active innovation demonstrated by AbbVie's Emrelis ADC approval expanding the antibody-drug conjugate category with targeted cytotoxic payload delivery.

Which indication leads the Cancer Targeted Therapy Market? Lung cancer dominated in 2024 through the highest density of clinically actionable genetic mutations including EGFR, ALK, ROS1, KRAS, MET, and HER2 that serve as targets for approved and pipeline therapies, with biomarker testing now routine in NSCLC enabling systematic identification of targetable mutations across the large global lung cancer patient population.

What makes antibody-drug conjugates the most innovative monoclonal antibody subcategory? ADCs combine the tumor-targeting precision of monoclonal antibodies with potent cytotoxic payloads that are released specifically within cancer cells, delivering chemotherapy directly to tumor cells while minimizing systemic toxicity, with AbbVie's Emrelis targeting c-Met overexpressing NSCLC representing the frontier of ADC development expanding into new tumor targets beyond the established HER2 ADC trastuzumab deruxtecan.

Why do hospital pharmacies dominate the cancer targeted therapy end-user segment? Cancer targeted therapies including monoclonal antibodies, ADCs, and immune checkpoint inhibitors are predominantly administered intravenously in clinical settings requiring specialized drug reconstitution, cold chain storage, patient monitoring for infusion reactions, and combination with supportive care that only hospital pharmacy and oncology clinic infrastructure can provide, making hospital pharmacies the primary distribution channel for the majority of targeted therapy revenue.

About Us

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us: Contact person: Ankit Mathur Email: sales@businessmarketinsights.com Phone: +16467917070