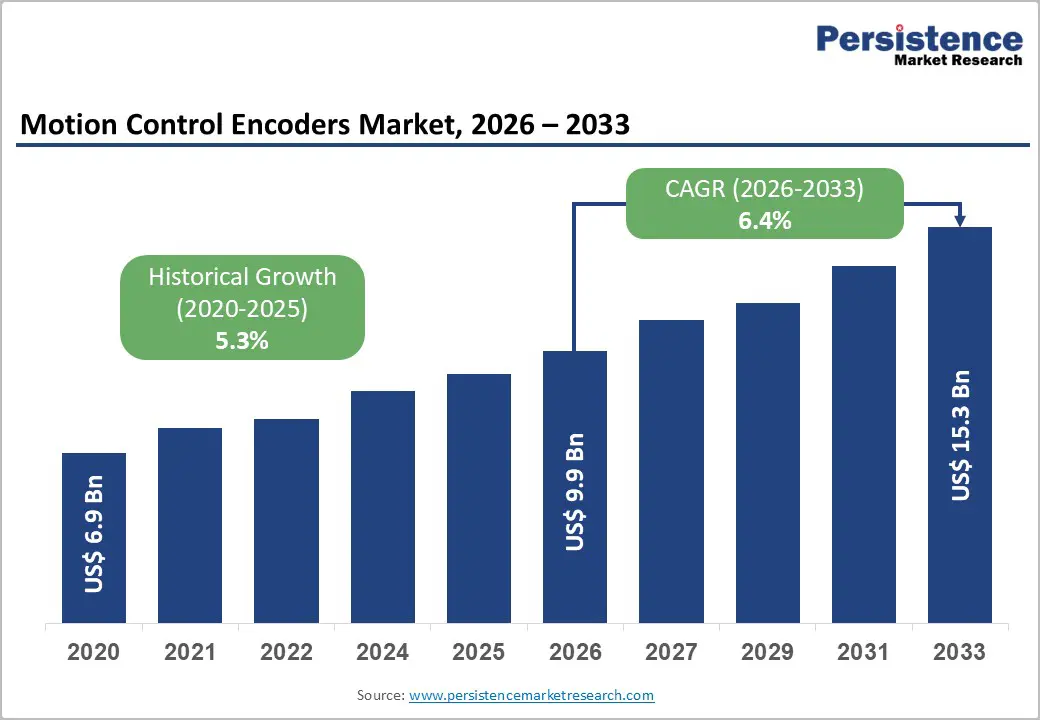

The global motion control encoders market is witnessing sustained expansion as industries accelerate automation adoption and demand increasingly precise motion feedback technologies. The market size is likely to be valued at US$ 9.9 billion in 2026 and is projected to reach US$ 15.3 billion by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033. Growth momentum is being fueled by rising investments in industrial automation, robotics integration, smart manufacturing systems, and precision-driven applications across healthcare, automotive, electronics, and aerospace sectors.

Motion control encoders play a vital role in determining speed, position, direction, and displacement in automated systems. These components enable accurate feedback mechanisms within motors, robotic systems, conveyor systems, CNC machinery, and medical devices. As manufacturers increasingly prioritize efficiency, precision, and operational reliability, encoder technologies are becoming essential components in modern industrial ecosystems.

The emergence of Industry 4.0 and the Industrial Internet of Things (IIoT) has further transformed the market landscape. Smart factories rely heavily on interconnected systems that require real-time motion feedback and continuous monitoring. Encoders facilitate these functions by providing highly accurate data that enhances synchronization, reduces machine downtime, and supports predictive maintenance strategies. The integration of AI-powered analytics and digital monitoring tools into industrial operations is expected to create additional opportunities for advanced encoder deployment.

Rising Automation Trends Strengthen Market Expansion

One of the strongest growth drivers for the motion control encoders market is the rapid adoption of industrial automation technologies. Manufacturers across sectors are modernizing production facilities to improve productivity, reduce labor dependency, and enhance quality control. Motion control encoders are fundamental to automation systems because they deliver precise positional and speed feedback that ensures machinery operates accurately and efficiently.

Industries such as automotive manufacturing, semiconductor fabrication, and electronics assembly increasingly depend on robotic systems and CNC machines for high-volume precision production. Encoders allow these systems to maintain synchronization and deliver consistent output quality. Their role becomes especially important in environments where even minor positional deviations can affect productivity or product quality.

Government-backed industrial modernization programs are also accelerating automation adoption globally. Public initiatives focused on advanced manufacturing, digital infrastructure, and smart factory implementation encourage companies to upgrade equipment and adopt intelligent control systems. As factories become more digitized, demand for high-resolution and real-time motion control feedback technologies continues to rise.

The growing use of collaborative robots, automated guided vehicles (AGVs), and machine vision systems is further expanding encoder applications. These technologies require reliable motion sensing and positional accuracy to operate safely and efficiently in dynamic industrial environments.

Industrial Modernization in Emerging Economies Creates Opportunities

Emerging economies are becoming major contributors to motion control encoder demand due to rising industrial investments and expanding manufacturing capabilities. Countries across Asia Pacific, Latin America, and parts of the Middle East are increasingly modernizing production facilities to improve competitiveness and integrate into global supply chains.

Governments in these regions are supporting industrial digitalization through incentive programs, infrastructure investments, and workforce training initiatives. As a result, manufacturers are upgrading conventional production lines with robotics, programmable logic controllers (PLCs), and advanced sensor networks. These systems require precise motion control technologies, significantly boosting encoder adoption.

Industrial modernization also supports higher production efficiency and improved quality assurance. Manufacturers operating in export-oriented industries such as automotive, electronics, and industrial machinery increasingly deploy advanced encoder systems to meet stringent international production standards and compliance requirements.

The rapid expansion of semiconductor manufacturing facilities and electronics assembly operations in Asia Pacific is particularly beneficial for the market. Precision manufacturing processes in these industries require highly accurate feedback systems capable of operating continuously under demanding conditions.

Technological Advancements Improve Encoder Performance

Continuous innovation in encoder technology is significantly improving product capabilities and expanding application possibilities. Manufacturers are developing advanced encoder systems with higher resolution, miniaturized designs, improved durability, and enhanced environmental resistance.

Absolute encoders are gaining strong adoption due to their ability to retain positional information even during power interruptions. These encoders provide reliable feedback in applications where maintaining precise positioning is critical, such as robotics, aerospace systems, and medical equipment.

Hybrid encoders, which combine optical and magnetic sensing technologies, are emerging as high-growth products within the market. These systems offer the precision of optical encoders while delivering the robustness of magnetic technologies. Hybrid designs perform efficiently in harsh industrial environments exposed to dust, vibration, moisture, and temperature fluctuations.

Wireless communication compatibility and IoT integration are becoming increasingly important in encoder design. Smart encoders capable of transmitting real-time operational data help manufacturers implement predictive maintenance strategies and improve system diagnostics. These capabilities reduce downtime and enhance operational efficiency.

Miniaturization trends are also expanding encoder use in compact devices, including surgical robotics, portable medical instruments, wearable technologies, and compact industrial equipment.

High Costs Remain a Key Market Constraint

Despite favorable growth prospects, the motion control encoders market faces challenges related to the high cost of advanced encoder systems. Precision manufacturing processes, sophisticated electronics integration, and specialized materials significantly increase production costs for high-resolution encoder technologies.

Optical encoders and advanced multi-turn absolute encoders often require complex fabrication techniques and high-performance components, making them more expensive than conventional alternatives. For small and medium-sized enterprises, these costs can create barriers to adoption, particularly in price-sensitive industries.

In addition to initial purchase costs, integration and maintenance expenses further impact adoption rates. Retrofitting advanced encoders into existing automation systems often requires engineering support, calibration, interface modules, and software customization. These additional expenses can extend return-on-investment timelines for manufacturers.

Operational environments also influence lifecycle costs. Encoders used in harsh industrial conditions require ruggedized designs and periodic maintenance to ensure reliable performance. As a result, some companies prefer phased automation upgrades rather than large-scale immediate deployments.

Integration Complexity Challenges Market Penetration

Compatibility issues and integration complexity continue to restrain broader encoder deployment across legacy industrial systems. Many manufacturing facilities still operate older equipment that lacks compatibility with modern industrial communication standards and digital control frameworks.

Integrating advanced encoders into legacy PLCs, distributed control systems, and outdated network architectures often requires extensive customization and middleware development. These processes increase implementation timelines and technical complexity.

Fragmentation of industrial communication standards further complicates integration efforts. Different automation platforms utilize varying protocols, making seamless interoperability difficult in some industrial environments. Motion control algorithms often require customized calibration and software configuration to interpret encoder feedback accurately.

Manufacturers with limited technical expertise may delay automation upgrades due to concerns regarding compatibility, implementation risks, and operational disruptions. However, ongoing standardization efforts and advancements in industrial communication technologies are expected to gradually reduce these challenges over time.

Medical Technology Emerges as a High-Growth Application

The healthcare sector is becoming one of the fastest-growing application areas for motion control encoders. Rising adoption of surgical robotics, automated diagnostic systems, rehabilitation devices, and laboratory automation technologies is creating substantial demand for highly precise motion feedback systems.

Medical applications require exceptional positional accuracy, reliability, and repeatability. Motion control encoders enable robotic surgical systems to perform delicate procedures with sub-millimeter precision while ensuring stable movement and real-time responsiveness. These capabilities improve procedural safety, reduce human error, and enhance patient outcomes.

Encoders also support advanced imaging equipment, automated sample handling systems, and catheter guidance technologies. Integration with computer-assisted control systems allows devices to adapt to patient-specific anatomical variations and improve treatment precision.

The growing focus on minimally invasive procedures and digital healthcare infrastructure further strengthens encoder adoption in medical technology applications. Increasing hospital investments in advanced medical equipment and laboratory automation are expected to support long-term market growth.

Product Type Insights

Absolute encoders are projected to dominate the motion control encoders market in 2026, accounting for approximately 45% of market revenue. Their ability to maintain positional data during power interruptions makes them highly valuable in industrial automation, robotics, aerospace, and medical systems.

These encoders provide accurate single-turn and multi-turn positional feedback that improves operational precision and reduces system errors. Integration with PLCs and digital control systems enables efficient communication and real-time process optimization.

Hybrid encoders are expected to witness the fastest growth during the forecast period. Their combination of magnetic and optical sensing technologies delivers improved environmental durability alongside high-resolution performance. These systems are increasingly utilized in AGVs, mobile robotics, industrial automation equipment, and medical devices operating in challenging environments.

Application Insights

Industrial automation is anticipated to remain the dominant application segment, accounting for nearly 55% of market revenue in 2026. Manufacturing facilities increasingly rely on motion control encoders to improve process accuracy, synchronization, and operational safety.

Encoders are widely used in conveyor systems, robotic arms, CNC machinery, and automated assembly lines. These technologies support reduced operational errors, optimized energy consumption, and enhanced production efficiency.

Medical technology is expected to emerge as the fastest-growing application segment between 2026 and 2033. Expanding use of robotic surgery systems, laboratory automation platforms, diagnostic imaging equipment, and rehabilitation robotics is driving rapid demand for compact and highly accurate encoder solutions.

Regional Analysis

Asia Pacific

Asia Pacific is expected to dominate the global motion control encoders market with more than 40% market share in 2026. Strong industrial automation adoption, large-scale robotics deployment, and expanding electronics manufacturing operations are driving regional growth.

Countries such as China, Japan, South Korea, and India continue investing heavily in smart manufacturing initiatives and precision engineering capabilities. Semiconductor fabrication, automotive production, and consumer electronics assembly facilities significantly contribute to encoder demand across the region.

Asia Pacific is also forecasted to be the fastest-growing regional market between 2026 and 2033 due to rapid digital transformation and increasing investments in factory modernization.

North America

North America maintains a strong market position due to advanced industrial infrastructure and widespread automation adoption across automotive, aerospace, and electronics industries. The region demonstrates high demand for precision motion control systems integrated with robotics, servomotors, and CNC equipment.

Significant investments in research and development support innovation in encoder miniaturization, IoT integration, and predictive maintenance technologies. Strong quality standards and advanced manufacturing ecosystems further reinforce market stability.

Europe

Europe remains an important market driven by its mature manufacturing base and focus on Industry 4.0 implementation. Automotive engineering, aerospace manufacturing, and industrial machinery production continue to generate strong demand for advanced encoder technologies.

The region’s emphasis on sustainability, energy efficiency, and smart factory development supports adoption of low-power and high-precision encoder solutions. Partnerships between industrial automation providers and system integrators are accelerating deployment across manufacturing facilities.

Competitive Landscape

The global motion control encoders market is moderately consolidated, with several multinational corporations and specialized regional manufacturers competing through innovation and technological advancement. Major companies focus on developing high-resolution, durable, and smart encoder solutions tailored for industrial automation, robotics, healthcare, and precision manufacturing applications.

Leading players include Kübler Group, Hohner Automation S.L., Baumer India Pvt. Ltd., SICK AG, HEIDENHAIN, Panasonic Industry Co., Ltd., AMETEK, Inc., Renishaw plc., US Digital, and Broadcom.

Strategic collaborations with system integrators and OEMs are helping companies strengthen distribution networks and improve customer support capabilities. Research and development investments continue focusing on smart encoders, wireless communication technologies, environmental durability, and compact high-performance designs.

Key Industry Developments

In December 2025, Geehy introduced its G32R430 encoder microcontroller unit specifically designed for high-precision motion control applications in industrial automation and robotics.

In July 2025, Maxon launched an encoder-free BLDC motor control technology capable of generating precise feedback using Hall sensor data, reducing design complexity while improving motor efficiency.

In May 2025, FLUX GmbH partnered with SEUM Tronics to expand the distribution of advanced encoder technologies within the South Korean industrial market.

Future Outlook

The future of the motion control encoders market remains highly promising as industrial automation, robotics adoption, and digital manufacturing transformation continue accelerating worldwide. Expanding applications in healthcare, autonomous systems, precision manufacturing, and smart factories will sustain long-term demand for advanced encoder technologies.

Continuous advancements in miniaturization, hybrid sensing, wireless communication, and IoT-enabled feedback systems are expected to redefine encoder capabilities and broaden their deployment across emerging industries. As manufacturers increasingly prioritize precision, efficiency, and predictive maintenance, motion control encoders will remain indispensable components within next-generation automation ecosystems.