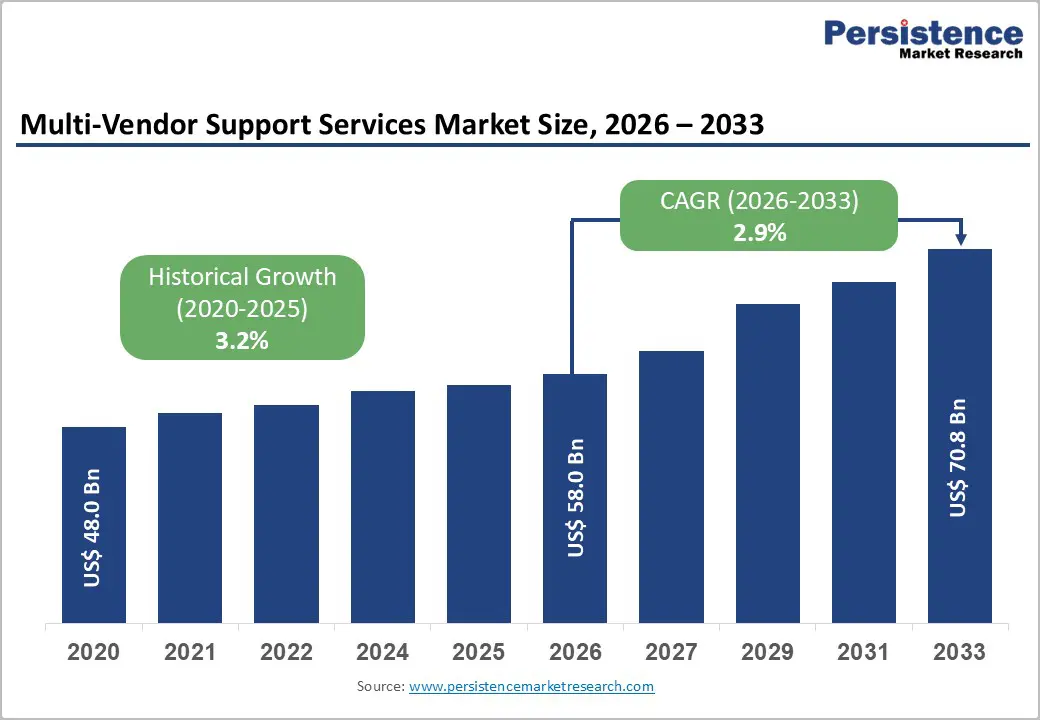

The global Multi-Vendor Support Services Market is entering a phase of steady, structurally driven growth as enterprises increasingly adopt complex, hybrid IT environments composed of technologies from multiple vendors. The market is expected to be valued at US$ 58.0 billion in 2026 and is projected to reach US$ 70.8 billion by 2033, expanding at a CAGR of 2.9% during 2026–2033.

This growth reflects a broader transformation in enterprise IT strategies, where organizations prioritize “best-of-breed” technologies rather than relying on single-vendor ecosystems. While this approach enhances flexibility and performance, it significantly increases operational complexity—creating strong demand for centralized, vendor-agnostic support services.

Market Overview

Modern enterprises operate highly distributed IT infrastructures that include servers, storage systems, networking hardware, cloud platforms, and edge computing environments. These systems are often sourced from multiple global vendors such as Cisco Systems, Hewlett Packard Enterprise, Dell Technologies, IBM, and NetApp.

As a result, IT environments have become fragmented and difficult to manage using traditional, vendor-specific support models. Multi-vendor support services address this challenge by offering:

- Unified maintenance across heterogeneous systems

- Centralized monitoring and troubleshooting

- Lifecycle management for hardware and software

- Coordinated service-level agreements (SLAs)

- Predictive maintenance and performance optimization

The increasing adoption of hybrid cloud architectures, edge computing, and distributed IT frameworks is further amplifying the need for integrated support services.

Key Market Highlights

- Market Size (2026): US$ 58.0 Billion

- Forecast (2033): US$ 70.8 Billion

- CAGR (2026–2033): 2.9%

- Historical CAGR (2020–2025): 3.2%

Regional and Segment Leaders

- Leading Region: North America (38% share in 2025)

- Fastest-Growing Region: Asia Pacific

- Leading Service Type: Hardware Support (62% share in 2025)

- Leading Enterprise Segment: Large Enterprises (68% share in 2025)

- Top Opportunity Area: AI-driven predictive maintenance

Market Drivers

- Rising Complexity of Multi-Vendor IT Environments

Enterprises are increasingly deploying heterogeneous IT infrastructures combining solutions from multiple providers. A typical enterprise may use:

- Servers from Dell Technologies

- Storage systems from NetApp

- Networking equipment from Cisco Systems

While this improves performance and vendor flexibility, it creates:

- Integration challenges

- Fragmented support contracts

- Increased downtime risk

- Higher operational overhead

Multi-vendor support services simplify these challenges by offering a single point of accountability, ensuring faster issue resolution and improved system reliability.

- Expansion of Cloud, Hybrid, and Edge Computing

The shift toward hybrid IT environments is one of the strongest growth drivers in the market. Enterprises now distribute workloads across:

- Public clouds such as AWS and Microsoft Azure

- Private cloud environments

- On-premises data centers

- Edge computing nodes

This distributed architecture increases system complexity and requires continuous monitoring across platforms. Multi-vendor support providers help by delivering:

- Cross-platform troubleshooting

- Real-time performance monitoring

- Integrated incident response systems

- Predictive analytics for infrastructure health

Market Restraints

- Cybersecurity and Regulatory Compliance Complexity

Regulatory frameworks such as GDPR and DORA require organizations to maintain strict data governance and security standards across all IT systems. Managing compliance across multiple vendors creates:

- Increased audit requirements

- Complex security coordination

- Higher governance overhead

- Risk of inconsistent policy enforcement

These challenges may slow adoption, especially in highly regulated industries.

- High Initial Integration Costs

Implementing multi-vendor support frameworks requires:

- Infrastructure mapping and audits

- System integration and configuration

- SLA alignment across vendors

- Migration and testing processes

These upfront costs can be significant, particularly for SMEs with limited IT budgets, limiting adoption in cost-sensitive markets.

Market Opportunities

- Digital Transformation in Emerging Economies

Emerging markets, particularly India, China, and Southeast Asia, are undergoing rapid digital transformation. Government initiatives such as “Digital India” and “Make in India” are accelerating:

- Data center expansion

- Cloud adoption

- Smart infrastructure development

- Enterprise IT modernization

As organizations deploy increasingly complex IT systems, demand for vendor-agnostic support services is expected to rise significantly.

- AI and Predictive Maintenance Integration

Artificial intelligence is transforming IT support operations by enabling:

- Predictive failure detection

- Automated diagnostics

- Real-time anomaly identification

- Self-healing infrastructure systems

Tools from providers such as Google Cloud and IBM Watson AIOps are helping enterprises move from reactive to proactive support models. This shift significantly enhances uptime and reduces operational costs.

Segment Analysis

Service Type

Hardware Support (Dominant Segment)

Hardware support accounts for 62% of the market in 2025, driven by:

- Large-scale data center deployments

- Enterprise server maintenance needs

- Networking and storage infrastructure complexity

Software Support (Fastest Growing)

Software support is expanding rapidly due to:

- Cloud application proliferation

- Hybrid IT environments

- Increasing need for cross-platform compatibility

Enterprise Size

Large Enterprises (Market Leader)

Large enterprises dominate with 68% share due to:

- Complex multi-vendor ecosystems

- Large IT budgets

- High dependency on uptime and performance

SMEs (Fastest Growing)

SMEs are increasingly adopting outsourced support services to:

- Reduce internal IT burden

- Access specialized expertise

- Support digital transformation initiatives

Delivery Model

Remote Support (Leading Model)

Remote support holds 55% share, enabled by:

- Advanced monitoring tools

- Cloud-based diagnostics

- Faster incident resolution

Hybrid Support (Fastest Growing)

Hybrid models combine:

- Remote troubleshooting

- On-site hardware servicing

- Flexible SLA-driven support

Industry Vertical

IT & Telecom (Largest Segment)

This sector leads due to:

- High infrastructure complexity

- Large-scale networking systems

- Continuous uptime requirements

Healthcare (Fastest Growing)

Healthcare is expanding rapidly due to:

- Digital health systems

- Telemedicine adoption

- Connected medical devices

- Regulatory compliance requirements

Regional Analysis

North America

North America leads the market with 38% share in 2025, driven by:

- Advanced enterprise IT infrastructure

- Strong presence of major vendors

- High adoption of hybrid cloud systems

The U.S. remains the dominant contributor, supported by innovation hubs and large-scale data center ecosystems.

Europe

Europe is experiencing steady growth with a projected CAGR of 4.2%, supported by:

- Industry 4.0 initiatives

- Strong cybersecurity regulations

- Expanding cloud adoption

Countries like Germany, the UK, and France are leading adoption.

Asia Pacific

Asia Pacific holds 32% market share and is the fastest-growing region due to:

- Rapid digital transformation

- Expansion of 5G networks

- Government-backed infrastructure investments

- Rising enterprise IT adoption in India and China

Competitive Landscape

The market is moderately consolidated, with major players focusing on:

- Global service expansion

- AI-driven support tools

- Predictive maintenance capabilities

- Strategic acquisitions and partnerships

Leading companies include:

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- Cisco Systems

- Microsoft Corporation

- Oracle Corporation

- Fujitsu Ltd.

- NEC Corporation

- NetApp Inc.

- Tata Consultancy Services (TCS)

Recent Developments

- IBM (2024): Enhanced multi-vendor management with Watson AIOps for automated incident detection.

- Cisco Systems (2024): Expanded edge support capabilities through AWS collaboration.

- HPE (2025): Strengthened diagnostics and predictive maintenance through acquisition of analytics firm.

Future Outlook (2026–2033)

The multi-vendor support services market is expected to evolve along three major trajectories:

- AI-First Support Models – Increasing reliance on predictive and automated systems

- Hybrid Infrastructure Expansion – Continued blending of cloud, edge, and on-premises systems

- Service Consolidation – Growth of unified, vendor-agnostic global service providers

While growth remains moderate in percentage terms, the structural importance of multi-vendor support services will continue to rise as IT environments become increasingly complex and interconnected.

Conclusion

The Multi-Vendor Support Services Market is steadily expanding as enterprises embrace diverse, multi-vendor IT ecosystems. Growth is primarily driven by rising infrastructure complexity, hybrid cloud adoption, and the increasing need for centralized support frameworks.

Although challenges such as compliance complexity and high integration costs persist, advancements in AI, predictive analytics, and automation are transforming service delivery models. Between 2026 and 2033, the market will continue shifting toward intelligent, unified, and proactive support systems that enhance enterprise efficiency and resilience.