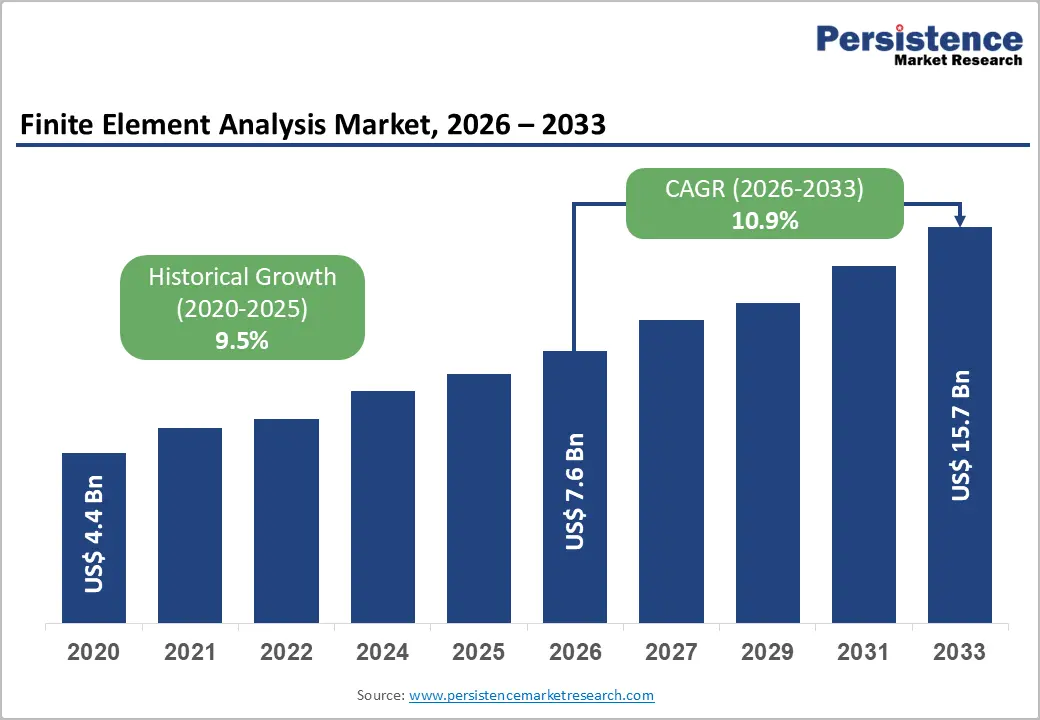

The global Finite Element Analysis (FEA) market is entering a new era of growth as industries increasingly rely on virtual prototyping, digital engineering, and simulation-driven product development. The market is projected to grow from US$7.6 billion in 2026 to US$15.7 billion by 2033, registering a robust CAGR of 10.9% during the forecast period. Rising demand for lightweight materials, rapid product development cycles, and stringent safety regulations are accelerating the adoption of advanced simulation tools across automotive, aerospace, electronics, construction, and manufacturing sectors.

Finite Element Analysis has become a cornerstone of modern engineering by enabling organizations to evaluate structural, thermal, fluid, and multiphysics performance before building physical prototypes. As businesses seek to reduce development costs while improving product reliability, FEA software is evolving from a specialized engineering tool into a strategic component of digital transformation initiatives.

Growing Demand for Virtual Prototyping Fuels Market Expansion

One of the primary drivers behind the growth of the finite element analysis market is the widespread adoption of virtual prototyping. Traditional product development processes often require multiple physical prototypes, resulting in higher costs and longer development cycles. FEA allows engineers to simulate real-world conditions and identify potential design flaws before manufacturing begins.

Automotive manufacturers increasingly use FEA to optimize vehicle weight, improve crashworthiness, and enhance fuel efficiency. The transition toward electric vehicles has further intensified the need for simulation tools, as automakers seek to validate battery systems, thermal management solutions, and lightweight structural components.

Similarly, aerospace companies rely heavily on FEA to analyze aircraft structures, engines, and composite materials. The ability to predict stress distribution, vibration behavior, and fatigue performance helps manufacturers meet strict regulatory standards while reducing development risks.

As organizations continue to prioritize cost reduction and faster time-to-market strategies, virtual prototyping is expected to remain a key growth engine for the FEA market.

AI and Machine Learning Revolutionizing Simulation Workflows

Artificial intelligence and machine learning are reshaping the finite element analysis landscape by introducing greater automation, predictive intelligence, and computational efficiency.

Modern AI-powered simulation platforms can learn from historical datasets and automatically identify optimal parameters for simulation scenarios. These capabilities significantly reduce engineering effort and improve design accuracy. Machine learning algorithms can also accelerate meshing processes, automate model preparation, and optimize simulation convergence, reducing overall analysis time.

Generative design is another transformative application gaining momentum. Engineers can define performance objectives, material constraints, and manufacturing requirements, allowing AI-driven systems to generate optimized design alternatives automatically. This approach enables innovative product development while minimizing material usage and production costs.

The launch of advanced AI-enhanced simulation platforms, such as Ansys 2024 R1, demonstrates the industry's commitment to integrating intelligent automation into engineering workflows. These innovations are expected to drive wider adoption of simulation technologies across both large enterprises and small-to-medium businesses.

Cloud-Based Simulation Accelerating Market Accessibility

The increasing adoption of cloud computing is creating significant opportunities for finite element analysis vendors and users alike. Traditionally, advanced FEA required expensive high-performance computing infrastructure and specialized IT resources. Cloud-based deployment models are changing this dynamic by providing scalable computing resources through subscription-based services.

Cloud FEA platforms enable organizations to access powerful simulation capabilities without significant capital investment. Engineering teams can perform complex analyses remotely, collaborate across geographies, and scale computing resources according to project requirements.

This flexibility is particularly valuable for small and medium-sized enterprises that previously faced financial barriers to adopting advanced simulation tools. Cloud-native solutions offered by companies such as Autodesk, Siemens, and Rescale are helping democratize access to engineering simulation technologies.

As digital engineering ecosystems become increasingly interconnected, cloud deployment is expected to experience the fastest growth among deployment models during the forecast period.

Lightweight Materials Drive Demand Across Key Industries

The growing use of lightweight materials is significantly expanding the application scope of finite element analysis. Industries are increasingly adopting advanced composites, high-strength alloys, and engineered polymers to improve performance while reducing weight.

In the automotive sector, lightweight materials play a critical role in improving electric vehicle efficiency and extending battery range. Engineers rely on FEA to evaluate structural integrity, crash performance, and fatigue characteristics of these materials under real-world operating conditions.

The aerospace industry is similarly investing in lightweight composite structures to reduce fuel consumption and lower emissions. Finite element simulations enable manufacturers to validate material performance, optimize structural designs, and ensure compliance with safety standards.

The trend toward sustainable engineering and energy-efficient product development is expected to further increase demand for sophisticated material simulation capabilities.

Skills Shortage Remains a Significant Market Challenge

Despite strong growth prospects, the finite element analysis market faces notable challenges related to workforce expertise and operational complexity.

Effective implementation of FEA requires specialized knowledge in numerical methods, material science, structural mechanics, and computational modeling. Engineers must possess a deep understanding of boundary conditions, mesh generation, and simulation validation techniques to achieve reliable results.

Many organizations struggle to find qualified simulation specialists, creating a gap between software investment and actual utilization. This shortage often results in longer deployment timelines, reduced productivity, and delayed return on investment.

Furthermore, increasingly complex multiphysics simulations demand advanced technical capabilities and significant computational resources. For regulated industries such as aerospace and defense, additional requirements related to cybersecurity, data governance, and validation further complicate implementation efforts.

Addressing these skill gaps through training programs, educational partnerships, and AI-assisted automation will be essential for unlocking the market's full potential.

Structural Analysis Continues to Dominate Applications

Structural analysis remains the largest application segment within the finite element analysis market, accounting for approximately 54% of market share in 2026.

This dominance reflects the fundamental role of structural simulation in product validation, infrastructure development, and engineering design. Organizations rely on structural analysis to assess stress distribution, deformation behavior, fatigue life, and failure mechanisms under various operating conditions.

Automotive crash testing, bridge design, industrial equipment validation, and aircraft structural analysis represent some of the most common applications. Advanced simulation capabilities allow engineers to optimize designs while maintaining safety and regulatory compliance.

Leading software platforms continue to enhance structural analysis functionality through nonlinear solver technologies, automation tools, and multiphysics integration, reinforcing the segment's market leadership.

Thermal Analysis Emerges as the Fastest-Growing Segment

Thermal analysis is expected to witness the fastest growth during the forecast period, driven by increasing thermal management challenges in electronics, electric vehicles, and advanced manufacturing systems.

As electronic devices become more compact and powerful, effective heat dissipation has become a critical design consideration. FEA enables engineers to simulate heat transfer mechanisms, identify thermal bottlenecks, and optimize cooling strategies.

Electric vehicle battery systems represent another major growth area. Battery performance, safety, and longevity depend heavily on thermal management efficiency. Advanced thermal simulations help manufacturers evaluate temperature distribution, cooling system effectiveness, and thermal runaway risks.

The expansion of high-performance computing, 5G infrastructure, and renewable energy technologies is expected to create additional demand for sophisticated thermal analysis solutions.

North America Maintains Market Leadership

North America is projected to account for approximately 33% of the global finite element analysis market in 2026, making it the largest regional market.

The region benefits from substantial research and development investments across aerospace, defense, semiconductor, and advanced manufacturing industries. High adoption rates of digital engineering technologies, coupled with strong regulatory support for simulation-based certification, continue to drive market growth.

The United States serves as the regional innovation hub, hosting major software providers and technology developers. Strong collaboration between software companies, government agencies, and defense contractors supports ongoing advancements in simulation capabilities.

The growing adoption of digital twins, cloud computing, and AI-powered engineering tools is expected to further strengthen North America's leadership position throughout the forecast period.

Asia Pacific Emerges as the Fastest-Growing Region

Asia Pacific is anticipated to be the fastest-growing regional market due to rapid industrialization, expanding manufacturing capabilities, and increasing digital transformation initiatives.

China continues to lead regional growth through aggressive investments in electric vehicles, smart manufacturing, high-speed rail infrastructure, and industrial automation. Government-supported digitalization programs are accelerating adoption of advanced simulation technologies across multiple sectors.

India is also emerging as a major engineering services hub, supported by growing investments in simulation centers, technical education, and software deployment. The country's expanding automotive, aerospace, and industrial sectors are creating substantial opportunities for FEA providers.

Meanwhile, Japan's mature automotive and electronics industries continue to invest heavily in precision engineering and simulation-driven innovation.

Collectively, these factors position Asia Pacific as a critical growth engine for the global finite element analysis market.

Competitive Landscape Focuses on AI and Digital Engineering

The finite element analysis market remains moderately consolidated, with major players including ANSYS, Dassault Systèmes, Siemens Digital Industries, Altair Engineering, Autodesk, Hexagon, and COMSOL dominating the competitive landscape.

Competition increasingly centers on AI integration, cloud deployment, digital twin capabilities, and end-to-end engineering workflows. Vendors are investing heavily in automation, predictive analytics, and multiphysics simulation technologies to differentiate their offerings.

Recent developments highlight the industry's innovation momentum. Siemens expanded its Simcenter portfolio with AI-enhanced fatigue analysis capabilities, while Dassault Systèmes strengthened Abaqus with advanced nonlinear analysis functionality. Autodesk's acquisition of Wonderdyn further reinforces the trend toward cloud-based simulation accessibility.

As organizations continue their digital transformation journeys, software vendors that successfully combine AI, cloud computing, and advanced engineering simulation are expected to capture significant market opportunities.

Future Outlook

The future of the finite element analysis market is closely tied to broader trends in digital engineering, artificial intelligence, and smart manufacturing. As simulation becomes increasingly integrated into product lifecycle management and digital twin ecosystems, demand for advanced FEA solutions will continue to rise.

The convergence of AI, cloud computing, and high-performance simulation is transforming how engineers design, validate, and optimize products. Organizations that embrace simulation-driven innovation will gain significant competitive advantages in terms of speed, cost efficiency, and product quality.

With expanding applications across automotive, aerospace, electronics, healthcare, energy, and infrastructure sectors, the finite element analysis market is well-positioned for sustained long-term growth, reaching US$15.7 billion by 2033 and establishing itself as a foundational technology for the next generation of engineering innovation.