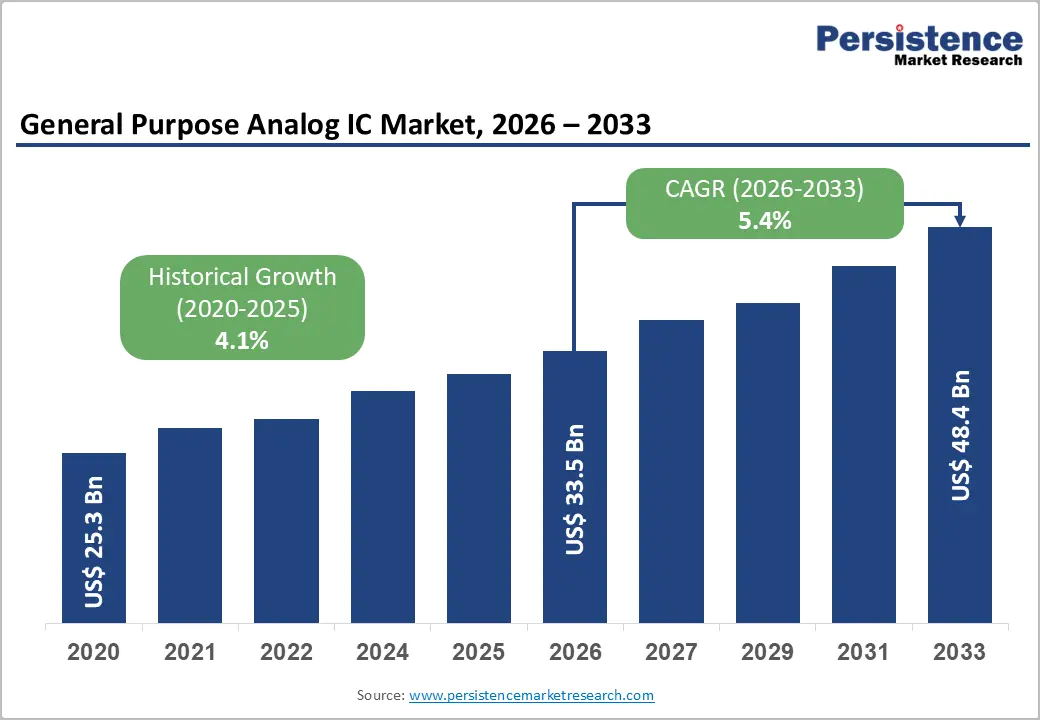

The global General Purpose Analog Integrated Circuit (IC) market is entering a new phase of sustained expansion, supported by rapid technological transformation across automotive, telecommunications, industrial automation, healthcare, and consumer electronics industries. Valued at approximately US$ 33.5 billion in 2026, the market is projected to reach US$ 48.4 billion by 2033, registering a compound annual growth rate (CAGR) of 5.4% during the forecast period.

Analog ICs play a critical role in modern electronic systems by processing real-world signals such as temperature, sound, pressure, voltage, and current. Unlike digital ICs that handle binary information, analog chips convert and manage continuous signals, making them indispensable in virtually every electronic device. From smartphones and electric vehicles to industrial robots and medical equipment, analog semiconductors serve as the foundation for power management, signal conditioning, timing, and data conversion.

As industries increasingly adopt smart technologies and connected systems, demand for high-performance analog components continues to grow, creating significant opportunities for manufacturers worldwide.

Rising Automotive Electrification Driving Analog IC Demand

One of the strongest growth drivers for the general purpose analog IC market is the accelerating adoption of electric vehicles (EVs). Global automotive manufacturers are rapidly expanding EV production to meet stricter environmental regulations and evolving consumer preferences for cleaner transportation.

Electric vehicles require substantially more semiconductor content than traditional internal combustion engine vehicles. Analog ICs are particularly important in EV architectures because they support critical functions such as battery management, power conversion, motor control, thermal monitoring, voltage regulation, and current sensing.

Battery management systems depend heavily on precision analog circuits to monitor cell health, optimize charging cycles, and ensure vehicle safety. Similarly, onboard chargers and traction inverters require sophisticated power management ICs capable of handling high voltages and demanding operating conditions.

As global EV sales continue to rise, semiconductor content per vehicle is increasing, creating long-term demand for analog solutions. Government initiatives supporting semiconductor manufacturing further strengthen supply chain resilience and position analog IC suppliers to capitalize on automotive electrification trends.

Industry 4.0 and Smart Factories Accelerate Market Growth

The rapid adoption of Industry 4.0 technologies is transforming manufacturing operations worldwide. Smart factories increasingly rely on connected sensors, programmable logic controllers, industrial robots, and real-time monitoring systems that require advanced analog semiconductor components.

Analog ICs play a crucial role in industrial automation by enabling accurate signal acquisition, sensor interfacing, data conversion, and process control. Precision measurements are essential in automated production environments where operational efficiency, safety, and product quality depend on real-time decision-making.

Industrial robots, machine vision systems, predictive maintenance platforms, and smart manufacturing equipment all require analog front-end architectures to collect and process data effectively.

As manufacturers continue investing in automation to improve productivity and reduce labor costs, demand for analog integrated circuits is expected to increase steadily. The growing deployment of connected industrial equipment will further expand the market for signal conditioning ICs, timing devices, and data converters.

5G Infrastructure Deployment Creates New Opportunities

The global rollout of 5G networks is generating significant opportunities for analog semiconductor manufacturers. Telecommunications infrastructure relies heavily on analog ICs to maintain signal integrity, synchronize network timing, and manage power consumption efficiently.

5G base stations require highly precise timing ICs, power management devices, and signal conditioning circuits to support ultra-fast data transmission and low-latency communication. Analog components also play a critical role in radio frequency systems, network equipment, and edge computing infrastructure.

As telecom operators continue expanding network coverage and increasing base station density, the demand for analog IC solutions will continue to grow. The emergence of edge computing, artificial intelligence at the network edge, and next-generation communication technologies further enhances the importance of high-performance analog semiconductors.

Governments worldwide are actively investing in digital infrastructure projects, creating favorable conditions for long-term market growth.

Consumer Electronics Remains the Largest End-Use Segment

Consumer electronics is expected to account for approximately 38% of the total market share in 2026, making it the largest end-use segment for general purpose analog ICs.

Modern electronic devices such as smartphones, tablets, laptops, smartwatches, wireless earbuds, gaming consoles, and smart home appliances depend heavily on analog components. These devices require power management solutions, sensor interfaces, signal processing capabilities, and battery optimization technologies to deliver high performance while maintaining energy efficiency.

The increasing popularity of wearable devices, Internet of Things (IoT) products, and connected home ecosystems is creating additional demand for analog semiconductors. Consumers continue to seek more powerful, compact, and energy-efficient devices, encouraging manufacturers to integrate advanced analog functionalities into product designs.

The expansion of electronics manufacturing in emerging economies such as India, Vietnam, and Thailand is also contributing to market growth by increasing production volumes and strengthening regional supply chains.

Power Management ICs Lead Product Segment

Among various product categories, power management ICs are expected to dominate the market, accounting for approximately 35% of total revenue in 2026.

Power management devices perform essential functions including voltage regulation, power conversion, battery charging, and energy optimization. They are widely used across automotive, industrial, telecommunications, healthcare, and consumer electronics applications.

As electronic systems become increasingly sophisticated, efficient power management has become a critical design requirement. Electric vehicles, renewable energy systems, data centers, and portable electronics all rely on advanced power management technologies to maximize performance and reduce energy consumption.

Manufacturers are investing heavily in next-generation power solutions, including gallium nitride (GaN) and silicon carbide (SiC) technologies, which offer improved efficiency and higher power density compared to conventional silicon-based devices.

These innovations are expected to strengthen the market position of power management ICs throughout the forecast period.

Data Converters Emerging as Fastest-Growing Segment

While power management ICs currently dominate market revenues, data converters are projected to be the fastest-growing segment through 2033, expanding at a CAGR of approximately 6.8%.

Analog-to-digital converters (ADCs) and digital-to-analog converters (DACs) serve as essential bridges between real-world analog signals and digital processing systems. They enable accurate data acquisition, sensor communication, and signal reconstruction in numerous applications.

Industries such as industrial automation, robotics, healthcare diagnostics, autonomous vehicles, and IoT devices increasingly require high-precision data conversion capabilities.

Advanced Driver Assistance Systems (ADAS), medical imaging equipment, smart sensors, and industrial control platforms all depend on high-performance data converters to process information accurately and efficiently.

As connected devices become more intelligent and data-driven, the importance of precision conversion technologies will continue to increase.

Healthcare Modernization Boosting Precision Analog IC Adoption

The healthcare sector is becoming an increasingly important growth avenue for analog semiconductor suppliers. Hospitals, diagnostic laboratories, and medical device manufacturers are investing heavily in advanced equipment that relies on precision analog technologies.

Medical imaging systems, patient monitoring devices, wearable health trackers, and portable diagnostic tools require high-accuracy signal conditioning, low-noise amplification, and reliable data conversion capabilities.

Analog ICs help ensure diagnostic accuracy, patient safety, and regulatory compliance in healthcare applications. The growing prevalence of remote patient monitoring, telemedicine, and connected healthcare ecosystems is creating additional opportunities for analog semiconductor providers.

Aging populations across developed economies are also driving demand for sophisticated medical equipment, supporting long-term market expansion in this high-value segment.

Asia Pacific Dominates Global Market Growth

Asia Pacific is expected to remain both the largest and fastest-growing regional market for general purpose analog ICs. The region is projected to account for approximately 41% of global market value in 2026 and is forecast to grow at a CAGR of 6.3% through 2033.

China continues to lead regional demand due to its massive consumer electronics production base, expanding EV industry, and extensive telecommunications infrastructure investments. The country's strong manufacturing ecosystem makes it a key consumer of analog semiconductor technologies.

Japan contributes through advanced automotive manufacturing, industrial automation, and robotics sectors, while South Korea and Taiwan remain critical semiconductor production hubs.

India is emerging as a significant growth market due to government-backed semiconductor initiatives, electronics manufacturing incentives, and increasing domestic demand for connected devices and EVs.

The expansion of regional fabrication facilities, assembly operations, and semiconductor design centers further strengthens Asia Pacific's position as the global growth engine for analog ICs.

Market Challenges and Competitive Pressures

Despite favorable growth prospects, the general purpose analog IC market faces several challenges. Supply chain disruptions, mature-node manufacturing constraints, and geopolitical uncertainties continue to affect semiconductor production capacity.

Many analog devices are manufactured using older process technologies that prioritize stability and reliability rather than miniaturization. Limited capacity at mature fabrication nodes can create supply shortages during periods of elevated demand.

Additionally, pricing pressure remains a significant concern, particularly in standardized product categories where competition is intense. Buyers frequently adopt multi-sourcing strategies, increasing pressure on suppliers to balance cost competitiveness with profitability.

Rising material costs, fabrication expenses, and inflationary pressures have prompted several semiconductor companies to implement selective price increases, highlighting ongoing cost management challenges across the industry.

Competitive Landscape and Future Outlook

The global general purpose analog IC market remains moderately consolidated, led by major semiconductor companies such as Texas Instruments, Analog Devices, STMicroelectronics, Infineon Technologies, and NXP Semiconductors.

These industry leaders continue investing in research and development, capacity expansion, automotive-grade technologies, and mixed-signal innovations to strengthen their competitive positions. Strategic acquisitions, partnerships, and advanced manufacturing investments are expected to shape future market dynamics.

Looking ahead, the convergence of electric mobility, industrial automation, 5G connectivity, healthcare digitization, and smart consumer technologies will continue driving demand for analog semiconductor solutions. As electronic systems become more intelligent, connected, and energy efficient, analog ICs will remain fundamental building blocks enabling next-generation innovation.

With strong growth opportunities across multiple industries and expanding global semiconductor investments, the general purpose analog IC market is positioned for resilient and sustained expansion through 2033.