The telecommunications industry is undergoing a major transformation as operators modernize network infrastructure to support the growing demands of 5G, cloud computing, edge applications, and enterprise digitalization. At the center of this transformation is Virtualized Radio Access Network (vRAN), a technology that decouples traditional hardware-based network functions and shifts them into software-driven, cloud-native environments.

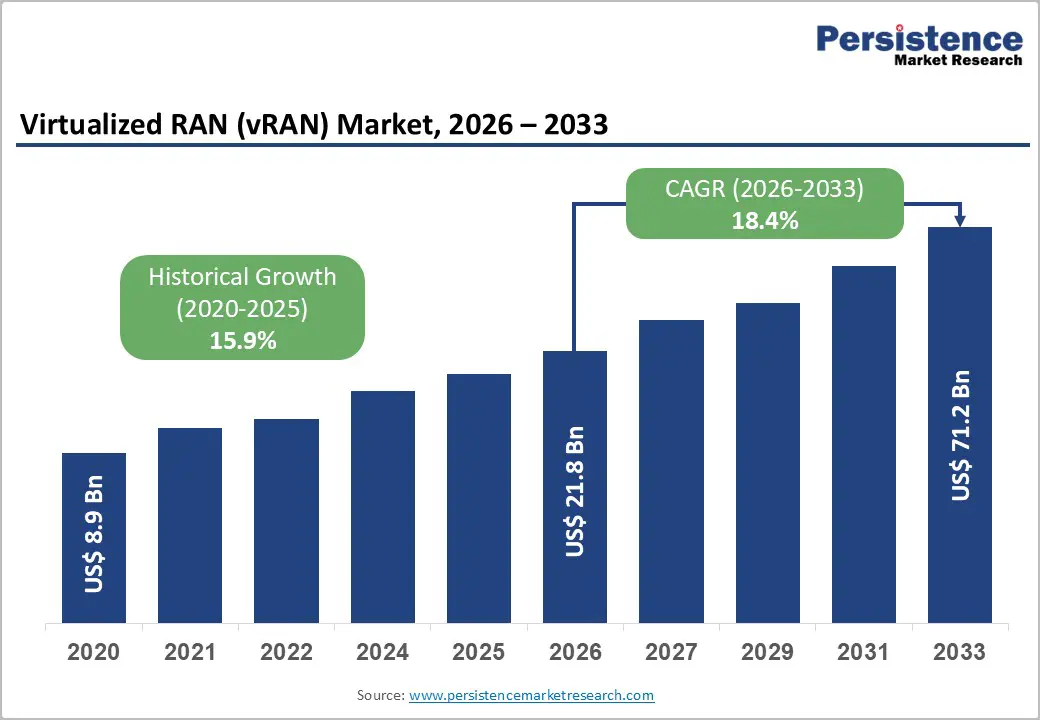

According to industry estimates, the global Virtualized RAN (vRAN) market is projected to grow from US$21.8 billion in 2026 to US$71.2 billion by 2033, registering a robust CAGR of 18.4% during the forecast period. The market’s rapid expansion is being fueled by accelerating 5G rollouts, increasing adoption of Open RAN architectures, rising mobile data traffic, and operators’ efforts to reduce network operating costs.

As telecom providers seek greater flexibility, scalability, and efficiency, vRAN is emerging as a foundational technology for next-generation wireless networks.

Understanding the Rise of Virtualized RAN

Traditional radio access networks rely on proprietary hardware and tightly integrated systems that often limit flexibility and increase deployment costs. Virtualized RAN changes this approach by separating software functions from dedicated hardware and running them on commercial-off-the-shelf (COTS) servers.

This virtualization allows operators to centralize network functions, dynamically allocate resources, and simplify network upgrades through software updates rather than expensive hardware replacements. The result is a more agile, cost-effective, and scalable network architecture capable of supporting diverse applications ranging from enhanced mobile broadband to industrial automation.

As telecom networks become increasingly software-defined, vRAN provides operators with the ability to deploy new services faster while optimizing infrastructure utilization.

5G Deployment Remains the Primary Growth Driver

The global rollout of standalone 5G networks is one of the strongest catalysts driving vRAN adoption. Telecom operators are investing heavily in infrastructure capable of supporting ultra-reliable low-latency communications, massive IoT connectivity, and advanced digital services.

Unlike previous generations of mobile technology, 5G networks require greater flexibility and processing capabilities. Virtualized architectures help operators meet these demands by enabling centralized management and efficient allocation of computing resources.

The growing adoption of applications such as autonomous vehicles, augmented reality, virtual reality, smart cities, and industrial IoT is further increasing the need for advanced radio access infrastructure. vRAN enables operators to respond quickly to changing network conditions while maintaining high levels of performance and reliability.

As global mobile data consumption continues to grow at unprecedented rates, virtualized network architectures are becoming essential for sustainable network expansion.

Open RAN Ecosystems Accelerate Market Expansion

Another significant factor contributing to the growth of the vRAN market is the increasing adoption of Open RAN (O-RAN) principles.

Historically, telecom operators depended heavily on single-vendor ecosystems, creating challenges related to cost, innovation, and interoperability. Open RAN addresses these concerns by promoting standardized interfaces that allow components from multiple vendors to work together seamlessly.

The emergence of O-RAN ecosystems provides operators with greater vendor flexibility, enhanced innovation opportunities, and reduced dependency on proprietary technologies. Governments and regulatory bodies across various regions are also supporting Open RAN initiatives as part of broader efforts to diversify telecommunications supply chains.

As a result, telecom companies are increasingly embracing virtualized and open network architectures to improve operational efficiency and foster competitive innovation.

Hardware Continues to Dominate Revenue Generation

Based on component analysis, hardware remains the largest segment in the virtualized RAN market, accounting for more than 46% of total market revenue in 2026 and exceeding US$10 billion in value.

Although vRAN focuses on software-driven functionality, the technology still requires powerful hardware platforms capable of handling real-time network processing. High-performance CPUs, GPUs, FPGAs, and specialized accelerators play a crucial role in ensuring low latency and high throughput.

The growing deployment of edge computing infrastructure is also increasing demand for advanced processing hardware. Telecom operators are investing in energy-efficient server platforms and acceleration technologies to maintain network performance while reducing operational costs.

At the same time, software is expected to be the fastest-growing component segment as operators increasingly adopt cloud-native architectures and software-defined networking solutions.

Public Deployments Lead While Private Networks Gain Momentum

Public deployments currently represent the largest deployment category within the vRAN market, accounting for over 55% of market share in 2026.

Telecom operators are leveraging public cloud and hyperscaler partnerships to accelerate network modernization while reducing capital expenditures. The scalability and flexibility offered by public deployment models make them particularly attractive for large-scale network expansion projects.

Major cloud providers are increasingly collaborating with telecom companies to provide infrastructure capable of supporting virtualized radio access functions. These partnerships are helping operators transition toward more flexible operational models while improving service delivery.

Meanwhile, private deployments are emerging as one of the fastest-growing segments in the market. Enterprises across manufacturing, logistics, healthcare, and defense sectors are implementing dedicated wireless networks to support mission-critical applications.

Private vRAN deployments offer enhanced security, lower latency, and greater customization, making them ideal for organizations seeking greater control over network operations.

LTE Networks Continue to Drive Adoption

Despite the rapid expansion of 5G, 4G/LTE remains the largest network type segment within the vRAN market, accounting for over 40% of total market revenue in 2026.

Many telecom operators are choosing to virtualize existing LTE networks as part of broader modernization initiatives. By deploying vRAN solutions in LTE environments, operators can improve network efficiency, reduce operating costs, and extend the lifespan of existing infrastructure.

In many developing economies, LTE continues to serve as the primary connectivity platform. Virtualization enables operators in these regions to improve network performance without undertaking costly hardware overhauls.

However, the 5G segment is expected to experience the fastest growth, expanding at a CAGR of 24.8% through 2033. The technology’s reliance on network slicing, edge computing, and ultra-low latency communications makes virtualized architectures particularly valuable for successful deployment.

Telecom Operators Remain the Largest End Users

Telecom operators account for more than 65% of total market revenue, making them the dominant end-user group in the vRAN ecosystem.

Growing consumer demand for high-speed connectivity, coupled with increasing network traffic volumes, is driving operators to modernize infrastructure and embrace cloud-native architectures. Virtualization provides a pathway toward lower operating costs, greater flexibility, and improved service quality.

Large-scale deployments by Tier-1 operators across North America, Europe, and Asia Pacific are creating significant growth opportunities for equipment manufacturers, software providers, and cloud infrastructure vendors.

At the same time, enterprises are becoming increasingly important customers. The rise of Industry 4.0, smart factories, and connected industrial ecosystems is encouraging businesses to deploy private 5G networks powered by virtualized infrastructure.

These enterprise deployments are expected to represent a major source of future market growth.

Edge Computing and AI Create New Opportunities

The convergence of vRAN, edge computing, and artificial intelligence is opening new avenues for innovation across the telecommunications sector.

Edge computing allows data processing to occur closer to users and devices, reducing latency and improving application performance. Because vRAN architectures already rely on distributed computing environments, they integrate naturally with edge infrastructure.

Industries such as manufacturing, transportation, healthcare, and energy are increasingly deploying edge-enabled networks to support real-time applications. This trend is creating significant demand for virtualized radio access solutions.

Artificial intelligence is also becoming a critical component of modern telecom networks. AI-powered vRAN platforms can automate network optimization, predict equipment failures, allocate resources dynamically, and improve overall operational efficiency.

As operators pursue autonomous network management capabilities, AI integration is expected to become a key competitive differentiator among vRAN vendors.

Regional Outlook: North America Leads, Asia Pacific Accelerates

North America currently dominates the global vRAN market, accounting for more than 38% of global revenue in 2026, equivalent to approximately US$8.3 billion.

The region benefits from extensive 5G investments, advanced cloud infrastructure, and strong support for Open RAN initiatives. Major telecom operators in the United States are actively implementing virtualized network architectures to improve flexibility and reduce long-term costs.

The presence of leading cloud providers, technology companies, and telecommunications innovators further strengthens North America's leadership position.

However, Asia Pacific is expected to be the fastest-growing regional market, registering a CAGR of approximately 23% during the forecast period.

China's large-scale 5G deployments, Japan's leadership in Open RAN implementation, and India's accelerating digital transformation initiatives are driving regional growth. Increasing mobile data consumption, favorable government policies, and expanding telecom infrastructure investments are creating strong opportunities across the region.

Europe also remains a significant market, supported by regulatory efforts promoting vendor diversification, digital transformation, and sustainable network development.

Competitive Landscape and Industry Developments

The virtualized RAN market remains moderately consolidated, with both established telecommunications vendors and innovative software-focused companies competing for market share.

Leading participants include:

- Huawei Technologies

- Ericsson

- Nokia Corporation

- ZTE Corporation

- Samsung Electronics

- NEC Corporation

- Fujitsu Limited

- Mavenir Systems

- Rakuten Symphony

- Parallel Wireless

Industry leaders are focusing on AI-enabled network optimization, cloud-native software platforms, Open RAN interoperability, and strategic partnerships to strengthen their competitive positions.

Recent collaborations involving Samsung, NVIDIA, Intel, Dell, and Orange demonstrate the industry's commitment to building scalable and energy-efficient virtualized network ecosystems capable of supporting future AI-driven telecommunications services.

Conclusion

Virtualized RAN is rapidly transitioning from an emerging technology to a fundamental component of next-generation telecommunications infrastructure. As operators seek to modernize networks, reduce operational costs, and support increasingly sophisticated digital services, virtualized architectures provide the flexibility and scalability required for long-term success.

Driven by 5G expansion, Open RAN adoption, edge computing growth, and enterprise demand for private wireless networks, the global vRAN market is expected to more than triple in value by 2033, reaching US$71.2 billion.

Organizations that invest early in cloud-native, AI-enabled, and open network architectures will be best positioned to capitalize on the next phase of telecommunications innovation, making vRAN one of the most transformative technologies shaping the future of global connectivity.