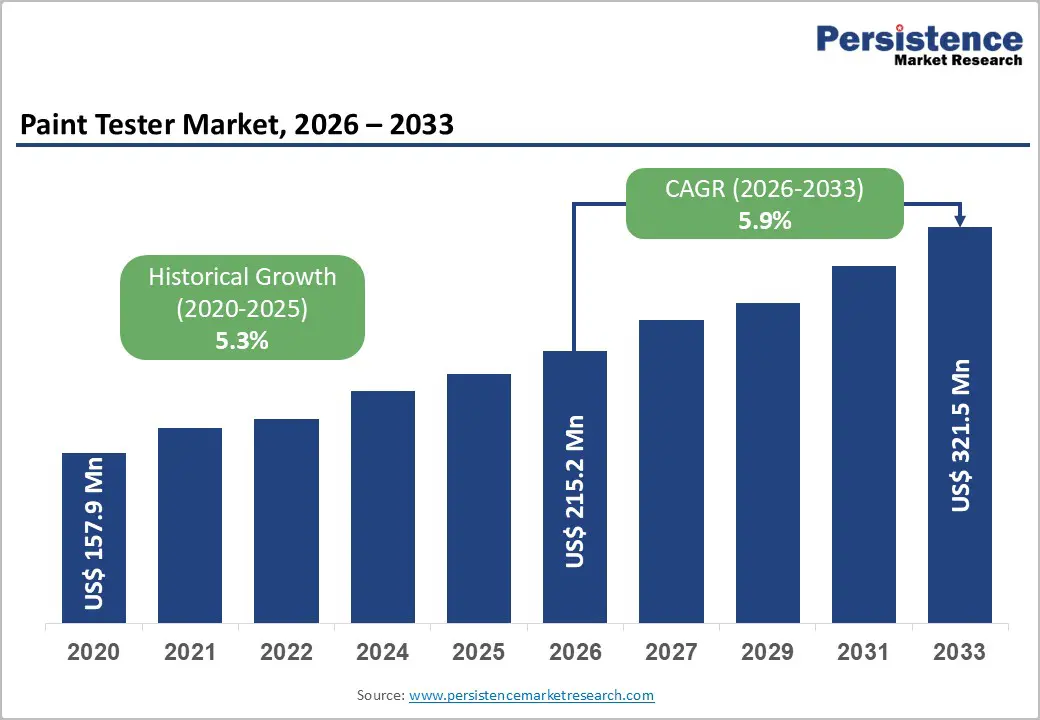

The global Paint Tester Market is poised for steady growth over the forecast period, supported by expanding industrial manufacturing activities, increasingly stringent quality control regulations, and rapid advancements in digital testing technologies. The market is expected to be valued at US$ 215.2 million in 2026 and is projected to reach US$ 321.5 million by 2033, registering a CAGR of 5.9% between 2026 and 2033.

Paint testing instruments have become essential tools across industries where coating performance directly impacts product quality, durability, corrosion resistance, safety, and aesthetics. Automotive manufacturers, aerospace companies, marine operators, infrastructure developers, and industrial coating producers increasingly rely on sophisticated testing solutions to ensure compliance with global quality standards.

The transition from traditional manual testing systems toward digital, connected, and data-driven quality inspection platforms is creating new opportunities for manufacturers of paint testing equipment worldwide.

Growing Automotive Production Fuels Demand for Paint Testing Equipment

The automotive industry remains the largest consumer of paint testing instruments globally. Modern vehicle production requires multiple coating layers, including primers, base coats, and clear coats, all of which must meet strict quality specifications.

Global vehicle production exceeds 85 million units annually, creating substantial demand for coating thickness gauges, adhesion testers, gloss meters, hardness testers, and corrosion testing systems. Automotive manufacturers must ensure consistent coating quality throughout the production process to maintain product durability, appearance, and warranty compliance.

Paint thickness measurement has become particularly important as automakers seek to optimize material consumption while maintaining corrosion protection standards. Even minor deviations in coating thickness can impact product performance, increase costs, or lead to quality failures.

The growing adoption of electric vehicles (EVs) further strengthens demand for advanced testing technologies. Unlike conventional vehicles, EVs utilize lightweight aluminum structures and composite materials that require specialized coating measurement techniques such as eddy current and ultrasonic testing. As EV production expands globally, manufacturers are investing heavily in next-generation paint inspection systems capable of accurately measuring coatings on multiple substrate types.

Regulatory Standards Strengthen Market Foundations

One of the most significant drivers supporting long-term market growth is the increasing global harmonization of paint and coating testing standards.

Organizations such as ASTM International, ISO, IEC, and various regional regulatory agencies have established comprehensive testing frameworks governing coating performance, durability, adhesion, corrosion resistance, gloss retention, and color consistency.

Standards such as ASTM D3359 for adhesion testing, ASTM B117 for salt spray corrosion testing, ASTM D3363 for hardness evaluation, and ISO 2409 for cross-cut adhesion testing are widely adopted across industries. Compliance with these standards often requires certified testing instruments and documented measurement procedures.

Regulatory requirements extend beyond manufacturing into sectors such as:

- Aerospace and defense

- Marine and shipbuilding

- Oil and gas infrastructure

- Industrial equipment manufacturing

- Construction and protective coatings

As environmental regulations and product quality requirements continue to evolve, organizations increasingly invest in certified testing systems to maintain compliance and minimize operational risks.

Digital Transformation Reshaping the Industry

Digitalization represents one of the most important trends transforming the Paint Tester market.

Traditional analog instruments are gradually being replaced by smart testing devices equipped with Bluetooth connectivity, cloud integration, mobile applications, automated reporting systems, and advanced analytics capabilities.

Modern testing solutions now allow quality inspectors to:

- Collect measurement data in real time

- Transfer inspection results wirelessly

- Generate automated compliance reports

- Store testing records in cloud platforms

- Integrate data into enterprise quality management systems

Industry 4.0 initiatives are accelerating this transformation. Manufacturers increasingly require seamless connectivity between inspection instruments and production management systems to support predictive quality control and statistical process monitoring.

The automotive sector, in particular, has become a major adopter of digital paint testing solutions due to quality management requirements under IATF 16949 standards. These standards emphasize measurement system analysis, process capability monitoring, and traceable quality documentation.

As a result, digital paint testing systems are expected to remain the fastest-growing technology segment throughout the forecast period.

High Equipment Costs Remain a Key Challenge

Despite strong growth prospects, the market faces certain limitations.

Premium paint testing laboratories require a wide range of specialized instruments, including corrosion chambers, spectrophotometers, automated adhesion testers, environmental aging systems, and advanced coating thickness gauges. These systems can involve investments ranging from several thousand dollars to well over US$100,000.

For small and medium-sized enterprises (SMEs), particularly in emerging economies, these costs can present significant barriers to adoption.

Additional expenses related to calibration, certification, software licensing, maintenance contracts, and operator training further increase total ownership costs.

Consequently, many smaller manufacturers continue to rely on basic testing equipment, delaying the transition toward comprehensive digital quality control systems.

Calibration and Technical Expertise Requirements

Another challenge affecting market expansion is the need for regular calibration and specialized technical expertise.

Many paint testing instruments used in regulated industries require traceable calibration procedures compliant with ISO/IEC 17025 standards. Maintaining measurement accuracy demands periodic verification using certified reference materials and calibration standards.

Organizations without dedicated quality laboratories often face difficulties managing calibration schedules and documentation requirements. In many developing regions, limited availability of accredited calibration laboratories further complicates instrument maintenance.

As testing technologies become increasingly sophisticated, manufacturers must also invest in employee training programs to ensure proper instrument operation and data interpretation.

Aerospace and Defense Offer Significant Growth Opportunities

The aerospace and defense sector represents one of the most attractive opportunities for paint testing equipment suppliers.

Aircraft coatings perform critical functions beyond aesthetics, including corrosion protection, UV resistance, chemical resistance, and aerodynamic performance enhancement. As a result, coating inspection requirements within aerospace applications are among the most demanding in any industry.

Global aviation growth is expected to drive substantial long-term demand. Commercial airlines continue expanding their fleets, while aircraft manufacturers maintain strong production pipelines to meet rising passenger traffic.

Every aircraft undergoes extensive coating inspection during manufacturing, maintenance, repair, and overhaul (MRO) operations. These activities require specialized paint testing technologies capable of evaluating coatings on aluminum alloys, composite structures, and advanced aerospace materials.

Military applications further support market growth through strict compliance requirements for defense coatings and protective systems used in aircraft, naval vessels, military vehicles, and infrastructure.

Product Segment Analysis

Coating Thickness Testers Lead the Market

Coating Thickness Testers represent the largest product category, accounting for approximately 31% of total market revenue.

Their dominance reflects the universal importance of thickness measurement across virtually all coating applications. Whether in automotive production, industrial manufacturing, marine construction, or aerospace assembly, coating thickness remains one of the primary indicators of coating performance.

Modern thickness testers utilize multiple technologies including:

- Magnetic induction

- Eddy current measurement

- Ultrasonic testing

- Multi-layer analysis systems

Recent innovations allow inspectors to measure multiple coating layers simultaneously without damaging the coating system, improving efficiency and accuracy.

Gloss Meters Maintain Strong Demand

Gloss meters constitute the second-largest product segment.

These instruments play a critical role in evaluating surface appearance and finish quality. Automotive manufacturers, furniture producers, appliance manufacturers, and industrial coating suppliers rely heavily on gloss measurements to maintain product consistency and customer satisfaction.

Growing consumer expectations for premium finishes continue to support demand for advanced gloss measurement technologies.

Technology Segment Analysis

Non-Destructive Testing Dominates

Non-Destructive Testing (NDT) technologies account for approximately 43% of market revenue, making them the dominant technology segment.

NDT methods enable inspectors to evaluate coating characteristics without damaging the painted surface or underlying substrate. This capability is essential in industries where products cannot be sacrificed for testing purposes.

Applications include:

- Automotive assembly lines

- Aircraft maintenance facilities

- Shipbuilding operations

- Industrial infrastructure inspections

The ability to conduct rapid, accurate, and repeatable inspections without interrupting operations makes NDT technologies indispensable across modern manufacturing environments.

Smart Testing Systems Gain Momentum

Digital and smart testing systems represent the fastest-growing technology category.

Features such as wireless connectivity, automated reporting, cloud integration, and AI-assisted data analysis are increasingly becoming standard requirements among industrial customers.

Manufacturers that successfully combine precision measurement with digital workflow integration are expected to gain significant competitive advantages over the coming decade.

Application Analysis

Automotive Manufacturing Leads End-Use Demand

Automotive manufacturing remains the largest application segment, representing approximately 38% of market revenue.

Vehicle manufacturers require comprehensive paint testing throughout production to ensure compliance with performance, durability, and appearance standards.

The automotive industry utilizes nearly every category of paint testing instrument, including:

- Thickness gauges

- Adhesion testers

- Gloss meters

- Color measurement systems

- Corrosion testing equipment

- Hardness testers

The industry's continuous focus on quality improvement and process optimization supports sustained demand for advanced testing solutions.

Aerospace and Defense Follow Closely

Aerospace and defense represent the second-largest application segment.

Higher technical requirements, stringent certification standards, and premium equipment specifications contribute to above-average revenue generation within this sector.

As aircraft production and maintenance activities increase globally, aerospace applications are expected to become an increasingly important source of market growth.

Regional Market Outlook

North America Maintains Leadership

North America remains the largest regional market for paint testing equipment.

The region benefits from a highly developed manufacturing sector, strong regulatory frameworks, advanced aerospace industries, and significant automotive production activities.

The presence of major testing instrument manufacturers, extensive ASTM standard adoption, and substantial defense-related procurement further strengthen regional market leadership.

Continuous innovation in coating inspection technologies is expected to support North America's dominant position throughout the forecast period.

Europe Drives Innovation

Europe serves as a global center for paint testing technology innovation.

The region hosts numerous leading manufacturers specializing in coating inspection equipment, color measurement systems, and advanced testing technologies.

Strong automotive production, industrial manufacturing expertise, and regulatory harmonization across European markets continue to drive equipment demand.

Germany, the United Kingdom, and the Netherlands remain particularly important markets due to their concentration of automotive and industrial coating activities.

Asia Pacific Emerges as the Fastest-Growing Market

Asia Pacific is expected to record the highest growth rate during the forecast period.

Rapid industrialization, expanding automotive production, rising infrastructure investments, and increasing adoption of international quality standards are creating significant opportunities across the region.

China remains the world's largest automotive manufacturing hub, while India continues to expand its vehicle production capabilities. Japan maintains leadership in precision manufacturing and advanced quality control systems.

Growing industrial activities across Southeast Asia further contribute to regional demand for paint testing equipment.

Competitive Landscape

The Paint Tester market remains moderately fragmented, with a mix of global leaders and regional specialists competing across multiple product categories.

Leading companies continue investing in digitalization, connectivity, automation, and software integration to differentiate their offerings.

Key competitive strategies include:

- Development of smart testing platforms

- Expansion of cloud-based quality management solutions

- Enhanced calibration services

- Global distribution network expansion

- Industry-specific product customization

The next phase of competition is expected to center on AI-enabled inspection systems, predictive quality analytics, and integrated digital ecosystems capable of delivering comprehensive coating quality management solutions.

Conclusion

The global Paint Tester market is entering a new phase of growth driven by industrial digitalization, expanding manufacturing activities, and increasingly rigorous quality standards. With the market projected to grow from US$ 215.2 million in 2026 to US$ 321.5 million by 2033, opportunities remain strong across automotive, aerospace, industrial manufacturing, marine, and infrastructure sectors.

As organizations prioritize quality assurance, regulatory compliance, and operational efficiency, demand for advanced, connected, and non-destructive paint testing technologies will continue to rise. Companies that successfully integrate precision measurement with digital data management and Industry 4.0 capabilities are expected to shape the future of the global Paint Tester market through 2033.