The global SCADA (Supervisory Control and Data Acquisition) market is entering a new phase of expansion as industries worldwide accelerate automation, digitalization, and real-time operational monitoring. SCADA systems have become the backbone of industrial control environments, enabling organizations to monitor, collect, analyze, and control processes across geographically dispersed assets and critical infrastructure.

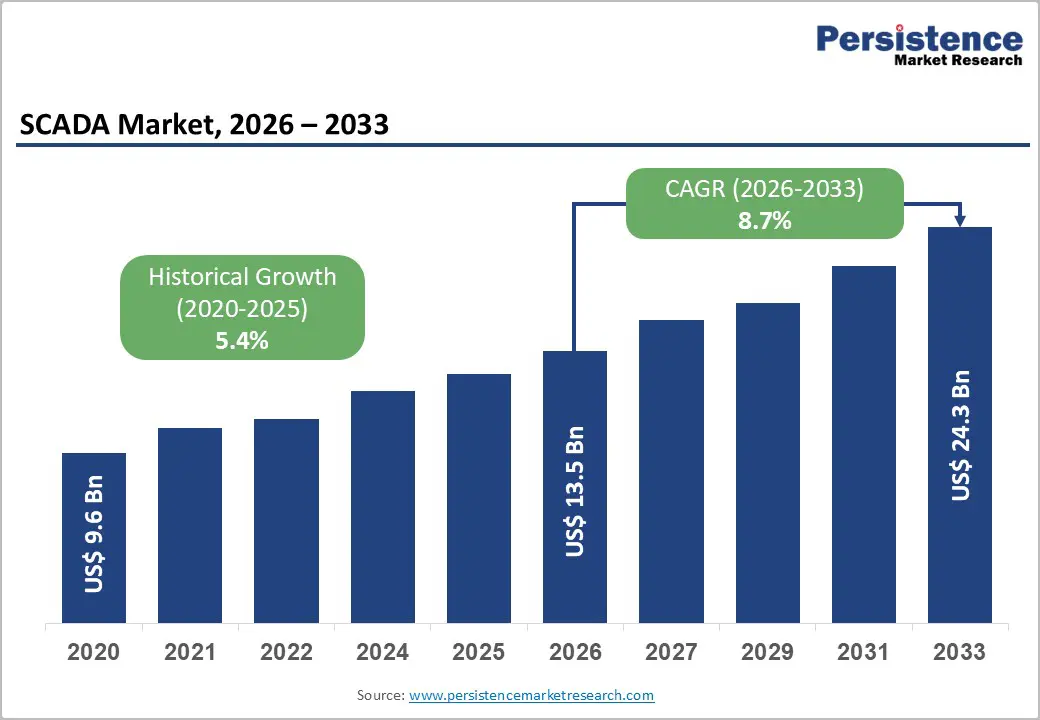

According to market estimates, the global SCADA market is projected to grow from US$13.5 billion in 2026 to US$24.3 billion by 2033, registering a CAGR of 8.7% during the forecast period. The market's growth is being fueled by increasing investments in smart grids, renewable energy integration, Industry 4.0 initiatives, and the rising need for operational efficiency across industrial sectors.

As businesses seek to improve productivity, reduce downtime, and enhance decision-making capabilities, SCADA systems are evolving beyond traditional monitoring platforms into intelligent operational ecosystems powered by artificial intelligence (AI), cloud computing, industrial IoT (IIoT), and advanced cybersecurity technologies.

Growing Importance of SCADA in Industrial Automation

Industrial automation remains one of the strongest growth drivers for the SCADA market. Manufacturers, utility operators, and infrastructure managers increasingly rely on automated systems to improve efficiency and maintain competitiveness.

SCADA platforms provide operators with real-time visibility into equipment performance, process conditions, and asset health. By integrating programmable logic controllers (PLCs), remote terminal units (RTUs), sensors, and communication networks, SCADA systems enable centralized monitoring and control of complex industrial operations.

Industries such as manufacturing, oil and gas, energy, transportation, and water treatment are increasingly deploying SCADA solutions to reduce operational costs and improve productivity. The growing adoption of predictive maintenance strategies is also encouraging organizations to invest in advanced SCADA platforms capable of generating actionable insights from operational data.

As digital transformation initiatives continue to gain momentum globally, SCADA systems are becoming critical components of connected industrial environments.

Grid Modernization Creating Significant Growth Opportunities

One of the most influential drivers of SCADA adoption is the ongoing modernization of electricity grids worldwide. Utilities are investing heavily in transmission and distribution automation, renewable energy integration, and smart grid infrastructure to improve reliability and efficiency.

The rapid expansion of renewable energy sources such as solar and wind power has increased the complexity of power management systems. Unlike conventional power generation, renewable energy assets are often geographically distributed and subject to fluctuating output levels.

SCADA systems play a crucial role in monitoring renewable energy installations, substations, energy storage systems, and transmission networks. They provide real-time telemetry, remote switching capabilities, outage management functions, and predictive maintenance support.

Government initiatives supporting clean energy adoption are further accelerating demand. Programs aimed at achieving carbon neutrality and energy transition goals require advanced supervisory systems capable of managing increasingly dynamic power networks.

As utilities continue modernizing aging infrastructure and deploying smart grid technologies, SCADA providers are expected to benefit from sustained long-term demand.

Industry 4.0 and Industrial IoT Driving Adoption

The emergence of Industry 4.0 has transformed how organizations manage industrial operations. Modern manufacturing facilities increasingly integrate machines, sensors, software platforms, and enterprise systems to create intelligent production environments.

SCADA systems serve as a critical bridge between operational technology (OT) and information technology (IT). They enable seamless communication between production equipment, Manufacturing Execution Systems (MES), Enterprise Resource Planning (ERP) platforms, and analytics tools.

Industrial IoT sensors generate vast amounts of operational data that SCADA systems collect and analyze in real time. This capability allows organizations to identify inefficiencies, predict equipment failures, optimize maintenance schedules, and improve asset utilization.

Advanced SCADA platforms are increasingly incorporating AI and machine learning algorithms that can identify patterns, detect anomalies, and provide predictive insights. These capabilities help operators make faster and more informed decisions, reducing downtime and improving overall operational efficiency.

As Industry 4.0 adoption expands globally, demand for intelligent SCADA solutions is expected to increase substantially.

Cybersecurity Challenges Remain a Key Concern

Despite strong growth prospects, cybersecurity remains one of the most significant challenges facing the SCADA market.

Historically, many SCADA systems operated within isolated environments. However, growing connectivity through cloud platforms, IoT devices, and remote access technologies has increased exposure to cyber threats.

Critical infrastructure sectors such as energy, water, transportation, and manufacturing are becoming attractive targets for cybercriminals and state-sponsored attacks. A successful breach can disrupt essential services, cause financial losses, and compromise public safety.

As a result, organizations are investing heavily in cybersecurity solutions designed specifically for industrial control systems. These include industrial firewalls, intrusion detection systems, network segmentation technologies, and zero-trust security frameworks.

Regulatory agencies worldwide are also introducing stricter cybersecurity requirements for critical infrastructure operators. Compliance with these regulations often requires substantial investments in security upgrades and system modernization.

While cybersecurity concerns may slow adoption in some regions, they are simultaneously creating opportunities for vendors offering secure and resilient SCADA platforms.

Hardware Segment Continues to Dominate

Based on component type, hardware remains the largest segment of the SCADA market.

In 2026, hardware is expected to account for more than 53% of total market revenue, exceeding US$7.2 billion. Demand remains strong for critical field devices such as RTUs, PLCs, sensors, communication gateways, and industrial networking equipment.

Many industrial facilities continue to modernize aging infrastructure, creating sustained demand for new hardware installations. Grid modernization projects, oil and gas facility upgrades, manufacturing automation initiatives, and infrastructure expansion in emerging economies further support hardware growth.

Reliable hardware remains essential for ensuring operational continuity, safety, and redundancy in mission-critical applications.

At the same time, software is emerging as the fastest-growing component segment. Organizations increasingly seek advanced visualization, analytics, cybersecurity, and interoperability capabilities that modern software platforms provide.

Cloud-Based SCADA Gains Momentum

Traditionally, on-premises deployments have dominated the SCADA landscape due to security, reliability, and compliance considerations.

The on-premises segment is expected to account for over 49% of market revenue in 2026, valued at more than US$6.6 billion. Industries operating critical infrastructure often prefer maintaining complete control over data and operational systems.

However, cloud-based SCADA solutions are experiencing rapid growth as organizations seek greater scalability, flexibility, and cost efficiency.

Cloud deployment offers several advantages, including reduced capital expenditures, centralized monitoring, remote accessibility, and simplified software updates. Organizations managing multiple facilities can benefit from unified operational visibility across geographically dispersed assets.

The increasing maturity of cloud security technologies and compliance frameworks is helping address historical concerns regarding data protection and operational risks.

As industrial organizations continue embracing digital transformation strategies, cloud-based SCADA adoption is expected to accelerate significantly throughout the forecast period.

Energy and Utilities Lead Market Demand

The energy and utilities sector remains the largest end-user of SCADA technology, accounting for more than 35% of global market revenue in 2026.

Electric utilities rely heavily on SCADA systems to monitor generation facilities, substations, transmission lines, and distribution networks. Real-time visibility enables operators to maintain grid stability, manage outages, and optimize asset performance.

The integration of renewable energy resources, distributed energy systems, and energy storage technologies is increasing operational complexity across power networks. SCADA platforms provide the control and monitoring capabilities necessary to manage these evolving environments effectively.

Government investments in energy infrastructure, grid resilience, and decarbonization initiatives continue to support adoption within this sector.

As electricity demand grows and renewable energy penetration increases, utilities are expected to remain among the most significant investors in SCADA technologies.

Water and Wastewater Segment Emerging as a High-Growth Opportunity

Among all industry verticals, water and wastewater management is expected to register one of the highest growth rates, with a CAGR of approximately 12.5% through 2033.

Population growth, urbanization, and aging infrastructure are placing increasing pressure on water systems worldwide. Utilities are turning to automation technologies to improve resource management, reduce losses, and ensure regulatory compliance.

SCADA systems enable real-time monitoring of pumps, pipelines, reservoirs, treatment facilities, and distribution networks. They help operators detect leaks, optimize energy consumption, monitor water quality, and respond quickly to operational issues.

Cloud-based SCADA solutions are particularly attractive for smaller utilities with limited IT resources. Subscription-based deployment models offer affordable access to advanced monitoring and control capabilities without large upfront investments.

As governments prioritize water sustainability and infrastructure modernization, demand from this segment is expected to grow rapidly.

Regional Analysis

North America

North America remains the largest regional market, accounting for more than 36% of global revenue in 2026.

Strong regulatory frameworks, extensive critical infrastructure networks, and substantial government investments support regional growth. Programs such as the Infrastructure Investment and Jobs Act (IIJA) continue driving modernization across energy, water, and transportation sectors.

The region also benefits from the presence of leading automation and industrial technology providers, fostering continuous innovation.

Asia Pacific

Asia Pacific is projected to be the fastest-growing regional market, expanding at a CAGR of 13.2%.

Rapid industrialization, urban development, smart city initiatives, and large-scale infrastructure projects are driving adoption throughout the region. China and India are investing heavily in smart grids, manufacturing automation, and water management systems.

Government-backed digital transformation programs and growing cybersecurity awareness are further accelerating SCADA deployment.

Europe

Europe continues to represent a major market for SCADA technologies, supported by strong industrial automation adoption and regulatory compliance requirements.

The expansion of renewable energy infrastructure, cross-border energy projects, and Industry 4.0 initiatives is creating new opportunities for vendors. Increased focus on cybersecurity and critical infrastructure resilience is also driving modernization efforts across the region.

Competitive Landscape

The SCADA market remains moderately consolidated, with major players focusing on innovation, cybersecurity, cloud integration, and AI-enabled analytics to strengthen their market positions.

Leading companies are pursuing mergers, acquisitions, strategic partnerships, and research and development investments to expand their capabilities and address evolving customer requirements.

Subscription-based software models, SaaS offerings, edge computing integration, and predictive analytics capabilities are becoming important competitive differentiators.

Key market participants include Siemens AG, Schneider Electric SE, Rockwell Automation, ABB Ltd., Emerson Electric Co., Honeywell International Inc., Mitsubishi Electric Corporation, Yokogawa Electric Corporation, Inductive Automation, GE Digital, Hitachi Ltd., and AVEVA Group.

Conclusion

The global SCADA market is poised for sustained growth through 2033 as industrial automation, smart infrastructure, renewable energy integration, and digital transformation initiatives continue reshaping operational environments worldwide.

The convergence of OT and IT systems, coupled with advances in AI, cloud computing, and industrial IoT technologies, is transforming SCADA from a traditional monitoring tool into a strategic platform for intelligent operations management.

Although cybersecurity concerns and legacy system integration challenges remain significant obstacles, ongoing innovation and infrastructure investments are expected to create substantial opportunities for vendors. As industries increasingly prioritize operational efficiency, resilience, and real-time decision-making, SCADA systems will remain at the center of the global industrial digitalization journey.