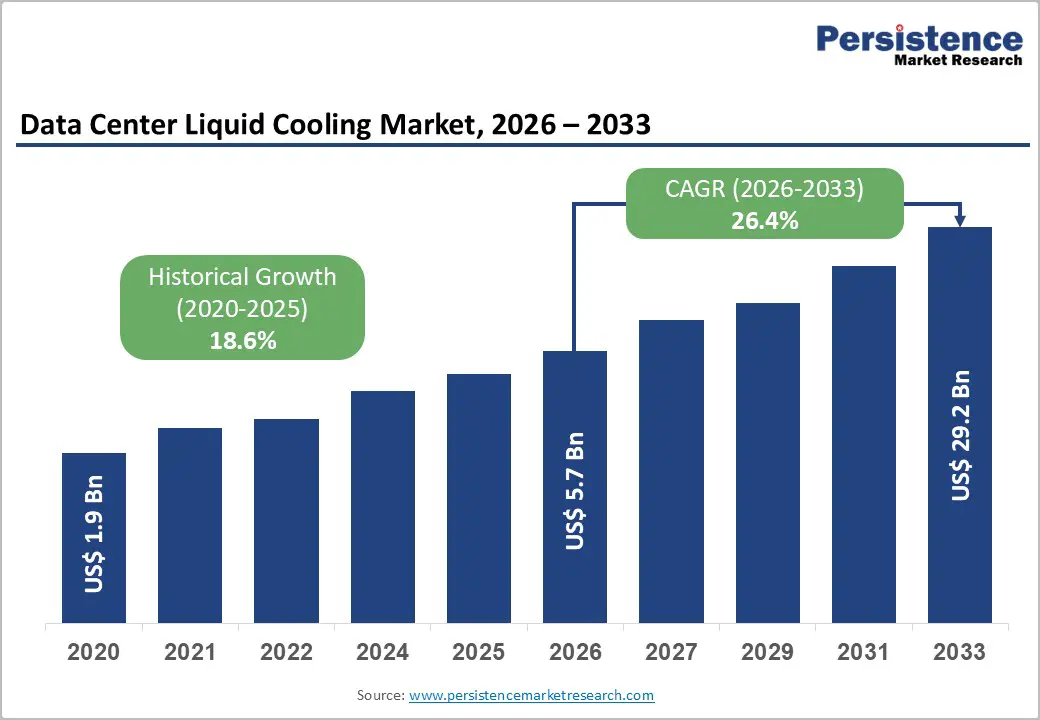

The global data center liquid cooling market is entering a transformative growth phase as the rapid expansion of artificial intelligence (AI), high-performance computing (HPC), cloud services, and hyperscale data centers drives unprecedented demand for advanced thermal management solutions. According to industry projections, the market is expected to grow from US$5.7 billion in 2026 to US$29.2 billion by 2033, registering an impressive CAGR of 26.4% during the forecast period.

As organizations increasingly deploy power-hungry GPUs and advanced processors to support AI model training, machine learning, and data analytics, traditional air-cooling systems are reaching their performance limits. Liquid cooling technologies, including cold plate and immersion cooling, are emerging as the preferred solutions due to their superior heat dissipation capabilities, energy efficiency, and ability to support high-density computing environments.

AI and High-Performance Computing Fuel Market Expansion

One of the most significant drivers of the data center liquid cooling market is the growing adoption of AI and HPC workloads. Modern AI applications require enormous computational power, leading to server rack densities that often exceed 30–50 kW per rack, compared to the conventional 5–10 kW levels found in traditional data centers.

These elevated power densities generate substantial heat, making conventional air cooling insufficient and costly. Liquid cooling technologies offer heat transfer capabilities that are up to 1,000 times more efficient than air, enabling operators to maintain optimal operating temperatures while reducing energy consumption.

The increasing deployment of AI infrastructure across industries such as healthcare, finance, manufacturing, scientific research, and defense is accelerating investments in advanced cooling systems. As global data center electricity consumption is projected to surpass 945 TWh by 2030, efficient thermal management solutions will become critical to ensuring operational sustainability and performance.

Sustainability Goals Accelerate Adoption of Liquid Cooling Technologies

Environmental concerns and stricter energy-efficiency regulations are compelling data center operators to adopt sustainable cooling solutions. Liquid cooling systems significantly improve Power Usage Effectiveness (PUE), often achieving values below 1.2 compared to 1.4–1.6 for conventional air-cooled facilities.

The ability of liquid cooling systems to dissipate heat more effectively helps operators reduce electricity consumption and carbon emissions while supporting environmental, social, and governance (ESG) objectives. Many technology companies are actively investing in innovative cooling methods to align with net-zero emission targets.

For example, next-generation cooling architectures have been designed to minimize water usage while maximizing energy efficiency. Such developments are becoming increasingly important as governments and regulatory bodies worldwide implement stricter sustainability mandates for digital infrastructure.

Solutions Segment Continues to Dominate Market Revenue

Based on component type, the solutions segment is expected to maintain its leadership position, accounting for more than 73% of the global market share in 2026, with a market value exceeding US$4.2 billion.

Data center operators increasingly prefer integrated liquid cooling solutions that address critical challenges such as heat density management, energy efficiency, and space optimization. These systems offer immediate benefits by improving thermal performance, reducing operational costs, and enabling higher computing capacity within existing infrastructure.

Meanwhile, the services segment is anticipated to witness the fastest growth, registering a CAGR of 27.8% through 2033. As liquid cooling deployments become more complex, organizations are seeking specialized expertise for system installation, maintenance, optimization, and performance monitoring. Service providers play an essential role in ensuring efficient operation and minimizing downtime.

Cold Plate Cooling Leads While Immersion Cooling Gains Momentum

Among cooling technologies, cold plate liquid cooling is expected to account for more than 55% of the market share in 2026, generating revenues exceeding US$3.1 billion.

Cold plate cooling directly transfers heat away from CPUs, GPUs, and other high-performance components through liquid-cooled plates. Its modular architecture and compatibility with existing server infrastructure make it an attractive option for data center operators seeking gradual adoption of liquid cooling technologies.

However, immersion cooling is emerging as the fastest-growing segment. In immersion cooling systems, servers are submerged in specially designed dielectric fluids that efficiently absorb and dissipate heat.

The technology offers substantial advantages, including up to 80% higher energy efficiency and exceptionally low PUE values ranging from 1.02 to 1.03. Additionally, immersion cooling enables compact deployments, allowing operators to maximize computing density while minimizing physical space requirements.

As AI workloads continue to increase, immersion cooling is expected to gain broader acceptance among hyperscale operators and HPC facilities.

Large Data Centers Remain Primary Consumers

Large-scale data centers occupying more than 10,000 square feet are projected to account for over 64% of the market share in 2026, representing a market value exceeding US$3.6 billion.

These facilities typically host extensive cloud infrastructure, enterprise applications, and AI processing systems that generate significant thermal loads. Liquid cooling technologies help large operators maintain uptime, improve energy efficiency, and achieve sustainability goals while supporting increasingly dense computing environments.

At the same time, small and medium-sized data centers are expected to experience rapid growth, with a projected CAGR of approximately 28%. The proliferation of edge computing, Internet of Things (IoT) applications, and localized data processing is creating demand for compact and energy-efficient cooling solutions suitable for space-constrained environments.

Cloud Providers Drive Fastest End-User Growth

Enterprises remain the largest end-user segment, accounting for more than 30% of market share in 2026. Organizations across industries are investing in liquid cooling to support advanced analytics, AI applications, virtualization, and mission-critical workloads while reducing energy costs.

However, cloud service providers are expected to record the highest growth rate, with a projected CAGR of 29.5% during the forecast period.

Leading hyperscale companies such as Amazon Web Services, Microsoft Azure, and Google Cloud are significantly expanding their infrastructure to support generative AI applications, machine learning platforms, and large-scale data processing.

These providers are increasingly incorporating liquid cooling systems into their facilities to meet sustainability objectives while supporting the computational requirements of next-generation AI services.

Challenges Associated with Deployment and Retrofitting

Despite strong growth prospects, the market faces several challenges that may slow adoption.

One major barrier is the high upfront investment associated with liquid cooling infrastructure. Installation costs can be 20% to 30% higher than conventional air-cooling systems, particularly for immersion cooling deployments that require specialized tanks, pumps, piping, and safety systems.

Retrofitting existing facilities presents additional difficulties. Legacy data centers often require significant redesigns to accommodate liquid cooling technologies, including modifications to racks, electrical systems, and facility layouts.

Furthermore, the industry faces a shortage of professionals with expertise in liquid cooling design, deployment, and maintenance. This skills gap can increase implementation timelines and operating costs.

Water consumption also remains a concern. Some liquid cooling approaches can require substantial water resources, raising questions about sustainability in regions facing water scarcity. Industry reports suggest that AI-focused data centers may dramatically increase water usage in the coming years, highlighting the need for innovative closed-loop cooling systems.

Innovation Creates New Growth Opportunities

Technological innovation continues to create significant opportunities for market participants.

The development of advanced dielectric fluids with improved thermal conductivity and environmental performance is enhancing the efficiency and safety of immersion cooling systems. These next-generation coolants support higher computing densities while reducing environmental impact.

Heat recovery technologies represent another promising opportunity. Instead of treating waste heat as a byproduct, operators are increasingly exploring ways to redirect thermal energy to district heating networks, commercial buildings, and industrial processes. This approach not only improves sustainability but also creates potential revenue streams.

Artificial intelligence is also being integrated into cooling management systems. AI-driven thermal optimization platforms can dynamically adjust cooling performance, predict maintenance requirements, and improve overall energy efficiency through real-time analytics.

Hybrid cooling systems that combine air cooling, liquid cooling, and intelligent controls are emerging as flexible solutions capable of supporting diverse workload requirements.

Government Policies Encourage Green Data Centers

Government initiatives worldwide are accelerating adoption of energy-efficient data center technologies.

Regulations in North America, Europe, and Asia increasingly emphasize reduced energy consumption, lower carbon emissions, and improved infrastructure sustainability. Policies promoting renewable energy integration, stricter PUE targets, and waste heat utilization are encouraging operators to invest in liquid cooling systems.

The growth of edge computing and 5G networks further strengthens market opportunities. Edge facilities often operate in space-constrained environments where traditional cooling methods are less effective, making liquid cooling an attractive alternative.

As governments continue supporting digital infrastructure modernization through incentives and sustainability mandates, demand for advanced cooling technologies is expected to rise significantly.

North America Maintains Market Leadership

North America is projected to account for more than 36% of global market share in 2026, with market revenues exceeding US$2.1 billion and expected to surpass US$8.7 billion by 2033.

The region benefits from strong investments in AI infrastructure, defense modernization, autonomous systems, and hyperscale data centers. Rising electricity consumption from data centers has increased the urgency for more efficient cooling technologies, driving widespread adoption across the United States and Canada.

Asia Pacific Emerges as Fastest-Growing Region

Asia Pacific is forecast to register the highest regional growth rate, achieving a CAGR of 35.6% through 2033.

Countries such as China, India, and Japan are witnessing rapid growth in cloud computing, AI development, 5G deployment, and digital transformation initiatives. Rising demand for energy-efficient infrastructure and supportive government policies are accelerating liquid cooling adoption across the region.

Competitive Landscape

The global data center liquid cooling market is moderately fragmented, with established technology companies and specialized cooling providers competing through innovation and strategic partnerships.

Major industry participants include Schneider Electric, LiquidStack, Rittal GmbH & Co. KG, Green Revolution Cooling, IBM, Asetek, Alfa Laval, Vertiv, and Fujitsu.

As AI computing continues to reshape the global digital landscape, liquid cooling is rapidly transitioning from a niche technology to a critical component of next-generation data center infrastructure. With increasing regulatory support, sustainability requirements, and demand for high-density computing, the market is poised for substantial growth through 2033.