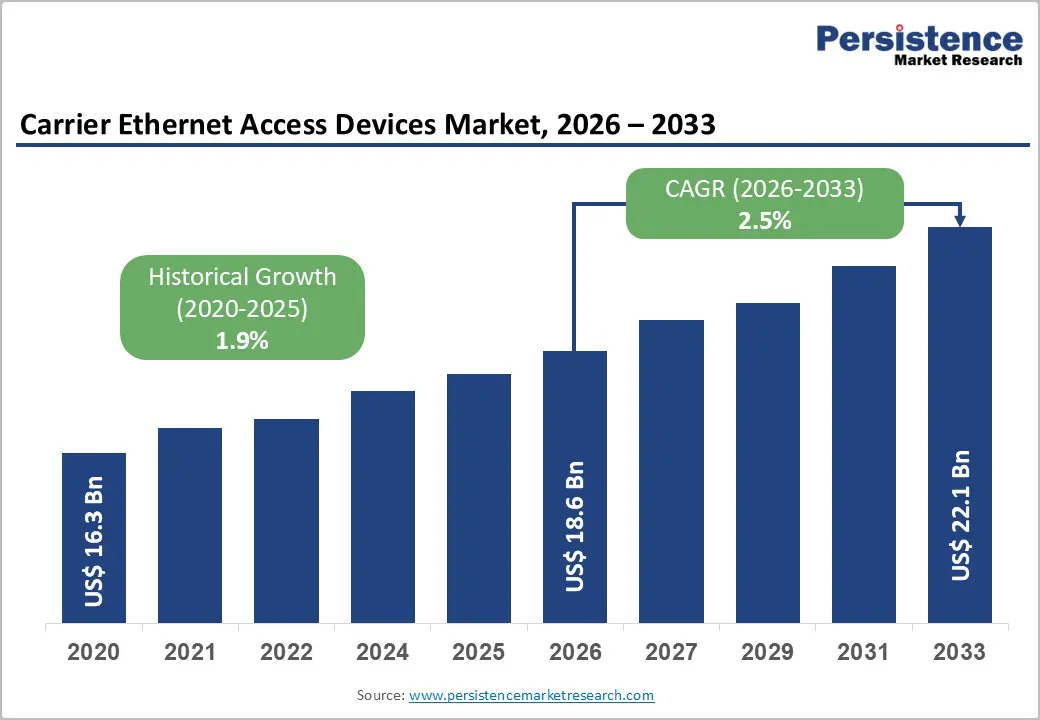

The global Carrier Ethernet Access Devices (CEADs) market is entering a phase of sustained expansion as telecom operators, enterprises, and public sector organizations increasingly prioritize high-performance network infrastructure. The market is estimated to be valued at US$ 18.6 billion in 2026 and is projected to reach US$ 22.1 billion by 2033, registering a CAGR of 2.5% during the forecast period from 2026 to 2033.

Carrier Ethernet access devices have become fundamental components of modern communication networks, providing the interface between service provider infrastructure and end-user environments. As organizations continue to embrace cloud computing, digital transformation, edge computing, and 5G technologies, demand for scalable, secure, and low-latency Ethernet connectivity solutions is growing steadily.

The transition away from legacy Time Division Multiplexing (TDM) networks toward Ethernet-based architectures is creating significant opportunities for vendors. These solutions offer enhanced flexibility, lower operational costs, simplified network management, and improved bandwidth scalability, making them increasingly attractive across a wide range of industries.

Rising 5G Deployments Fuel Demand for Carrier Ethernet Infrastructure

One of the primary drivers of the carrier Ethernet access devices market is the rapid deployment of 5G networks worldwide. Telecom operators are expanding network capacity to support growing mobile data consumption, connected devices, and emerging digital services.

The rollout of dense small-cell architectures requires robust fronthaul and backhaul connectivity. Carrier Ethernet access devices play a critical role in connecting cell sites to core networks while maintaining low latency and high reliability. As operators invest heavily in fiber-based transport infrastructure, demand for carrier-grade Ethernet equipment continues to rise.

The increasing adoption of Open Radio Access Network (Open RAN) frameworks is also contributing to market growth. Open architectures reduce vendor dependency and encourage interoperability among network components, creating opportunities for Ethernet device manufacturers to provide flexible and scalable solutions.

Furthermore, applications such as autonomous transportation, industrial automation, augmented reality, and telemedicine require real-time communication capabilities. Ethernet access infrastructure enables operators to meet these stringent performance requirements while ensuring network scalability for future traffic growth.

Enterprise Digital Transformation Accelerates Market Expansion

Digital transformation initiatives across industries are significantly increasing demand for carrier Ethernet access devices. Organizations are modernizing IT environments and migrating critical workloads to hybrid and multi-cloud infrastructures, creating the need for highly reliable network connectivity.

Modern enterprises require deterministic networking performance to support applications such as unified communications, cloud collaboration, financial transactions, data analytics, and industrial automation. Carrier Ethernet solutions provide the low-latency, high-availability connectivity necessary for these mission-critical workloads.

As businesses expand geographically and adopt distributed operating models, Ethernet access devices are helping establish seamless connectivity between branch offices, data centers, cloud environments, and remote users. Enhanced service-level agreements (SLAs) and centralized network management capabilities further strengthen their appeal among enterprise customers.

Industry standards such as MEF 3.0 are improving interoperability and service consistency, enabling organizations to deploy carrier Ethernet services more efficiently across complex network environments. These developments are expected to support long-term market growth as enterprises continue to prioritize digital resilience and operational efficiency.

Industrial IoT and Smart Infrastructure Create New Opportunities

The convergence of Operational Technology (OT) and Information Technology (IT) networks is opening new avenues for carrier Ethernet access device adoption. Industrial sectors increasingly require resilient communication infrastructure capable of supporting real-time automation and machine-to-machine communications.

Manufacturing facilities, energy utilities, transportation networks, and smart city projects are deploying Ethernet-based networking solutions to facilitate data exchange between connected devices and centralized management systems. Carrier Ethernet access devices equipped with Time-Sensitive Networking (TSN) capabilities provide the deterministic performance required for these environments.

In smart factories, CEADs support Industry 4.0 initiatives by enabling synchronized communication between sensors, controllers, robotics systems, and analytics platforms. Similarly, utility providers use Ethernet networks to manage smart grids and monitor infrastructure assets in real time.

Transportation authorities are also leveraging Ethernet connectivity for intelligent traffic management systems, surveillance networks, and public transit operations. As investments in smart infrastructure continue to grow globally, demand for ruggedized and industrial-grade Ethernet access devices is expected to increase substantially.

SD-WAN Adoption Presents Competitive Challenges

While market growth remains positive, carrier Ethernet access device vendors face increasing competition from Software-Defined Wide Area Networking (SD-WAN) platforms.

SD-WAN solutions offer organizations centralized management, policy-based traffic routing, and greater flexibility across multiple connectivity options. Many enterprises are adopting software-centric networking strategies to simplify operations and reduce hardware dependency.

Cloud-first organizations particularly favor SD-WAN because of its ability to optimize traffic routing across SaaS applications and hybrid cloud environments. Integrated security capabilities further enhance the value proposition of these platforms.

As a result, some enterprises are reducing investments in traditional networking hardware. However, carrier Ethernet access devices continue to maintain a strong position in applications where guaranteed performance, low latency, and carrier-grade reliability are essential.

In response, leading vendors are integrating SD-WAN functionality into Ethernet platforms and developing hybrid networking solutions that combine the strengths of both technologies. This convergence is helping manufacturers remain competitive while addressing evolving customer requirements.

Technological Complexity Remains a Key Barrier

The growing sophistication of communication networks presents several challenges for the carrier Ethernet access devices market. Organizations often struggle with integrating modern Ethernet solutions into existing legacy infrastructures.

Many telecom operators continue to maintain TDM-based systems alongside newer Ethernet networks, creating interoperability concerns and increasing deployment complexity. Ensuring compatibility across diverse hardware environments requires extensive testing, customization, and technical expertise.

Rapid changes in networking standards and technologies further complicate implementation efforts. Service providers must continuously upgrade equipment, software, and workforce skills to remain competitive.

To address these challenges, manufacturers are investing in automation, simplified management interfaces, and advanced interoperability features. Solutions that support smooth migration from legacy environments are gaining significant traction among organizations seeking to modernize their networks without disrupting operations.

Switches Continue to Dominate Device Segment

By device type, switches are expected to maintain their leadership position in the carrier Ethernet access devices market, accounting for approximately 58% of total revenue in 2026.

Ethernet switches play a critical role in directing data traffic efficiently across networks while minimizing latency and congestion. Their ability to support high-bandwidth applications makes them indispensable in data centers, telecom networks, and industrial environments.

Growing data traffic generated by cloud computing, video streaming, IoT deployments, and enterprise applications is driving continued investment in advanced switching technologies. Organizations value switches for their scalability, reliability, and ability to support evolving network architectures.

Meanwhile, routers are projected to emerge as the fastest-growing device category during the forecast period. As network environments become increasingly complex, demand for intelligent routing solutions capable of managing dynamic traffic patterns and enforcing security policies continues to rise.

Advanced Ethernet routers support critical functions such as network segmentation, traffic prioritization, NAT, DHCP, and cloud connectivity, making them essential components of modern enterprise and telecom infrastructures.

Telecommunications Sector Remains the Largest End User

The telecommunications sector is expected to account for approximately 45% of market revenue in 2026, making it the largest end-user segment for carrier Ethernet access devices.

Telecom operators continue to invest heavily in network modernization initiatives to accommodate growing demand for broadband, mobile services, and digital applications. Ethernet access devices support these efforts by enabling reliable transmission of voice, video, and data traffic across increasingly complex network environments.

The ongoing expansion of fiber networks, 5G deployments, and edge computing infrastructure is further strengthening demand within the telecom sector. Service providers rely on CEADs to improve network performance, reduce operational costs, and maintain service quality.

At the same time, the enterprise segment is anticipated to record the fastest growth through 2033. Organizations across industries are adopting carrier Ethernet solutions to support cloud computing, digital collaboration, cybersecurity initiatives, and remote work environments.

As enterprises increasingly depend on real-time applications and distributed operations, demand for scalable and secure Ethernet connectivity is expected to accelerate.

North America Leads Global Market Share

North America is projected to hold approximately 35% of the global carrier Ethernet access devices market in 2026, supported by its advanced telecommunications infrastructure and strong concentration of technology vendors.

The region benefits from widespread fiber deployment, early adoption of 5G technologies, and significant investments in edge computing and cloud infrastructure. Telecommunications providers and enterprises continue to upgrade networks to support increasing data traffic and evolving digital services.

Government-backed broadband expansion programs are also improving connectivity in underserved regions, creating additional opportunities for Ethernet infrastructure deployment.

Furthermore, North American organizations remain at the forefront of digital transformation initiatives, driving demand for advanced networking solutions that support cloud migration, smart city projects, and industrial automation.

Asia Pacific Emerges as the Fastest-Growing Region

Asia Pacific is expected to be the fastest-growing regional market between 2026 and 2033. Rapid digital transformation across major economies such as China and India is creating strong demand for carrier Ethernet access devices.

Governments throughout the region are investing heavily in broadband infrastructure, fiber networks, and smart city development projects. Expanding internet penetration and increasing smartphone adoption are also contributing to rising network traffic volumes.

Telecommunications operators are accelerating 5G rollouts, while enterprises are investing in cloud computing, industrial IoT, and digital modernization initiatives. These factors are driving substantial demand for Ethernet access infrastructure across both urban and rural markets.

Local manufacturing capabilities and supportive government policies are further strengthening the region’s position as a major growth engine for the global market.

Competitive Landscape

The global carrier Ethernet access devices market is moderately consolidated, with major industry participants accounting for an estimated 35% to 40% of total market share. Leading vendors compete through technological innovation, product diversification, strategic partnerships, and geographic expansion initiatives.

Key companies operating in the market include:

- Cisco Systems

- Juniper Networks

- ADTRAN Holdings

- Calix

- Huawei Technologies

- ZTE Corporation

- Nokia Corporation

- Ericsson

- NETGEAR

- RAD Data Communications

- CIENA Corporation

- Lumentum Operations

- FiberHome Telecommunication Technologies

- Ribbon Communications

Future Outlook

The carrier Ethernet access devices market is poised for steady growth through 2033 as enterprises, telecom operators, and public infrastructure providers continue investing in next-generation connectivity solutions. While competition from SD-WAN and software-centric architectures presents challenges, Ethernet technology remains essential for delivering carrier-grade performance, low latency, and network reliability.

The expansion of 5G networks, industrial IoT ecosystems, cloud-native applications, smart infrastructure projects, and edge computing environments will continue to create long-term opportunities for vendors. Organizations seeking scalable, secure, and future-ready networking solutions are expected to maintain strong demand for carrier Ethernet access devices, ensuring the market's relevance in the evolving digital economy.