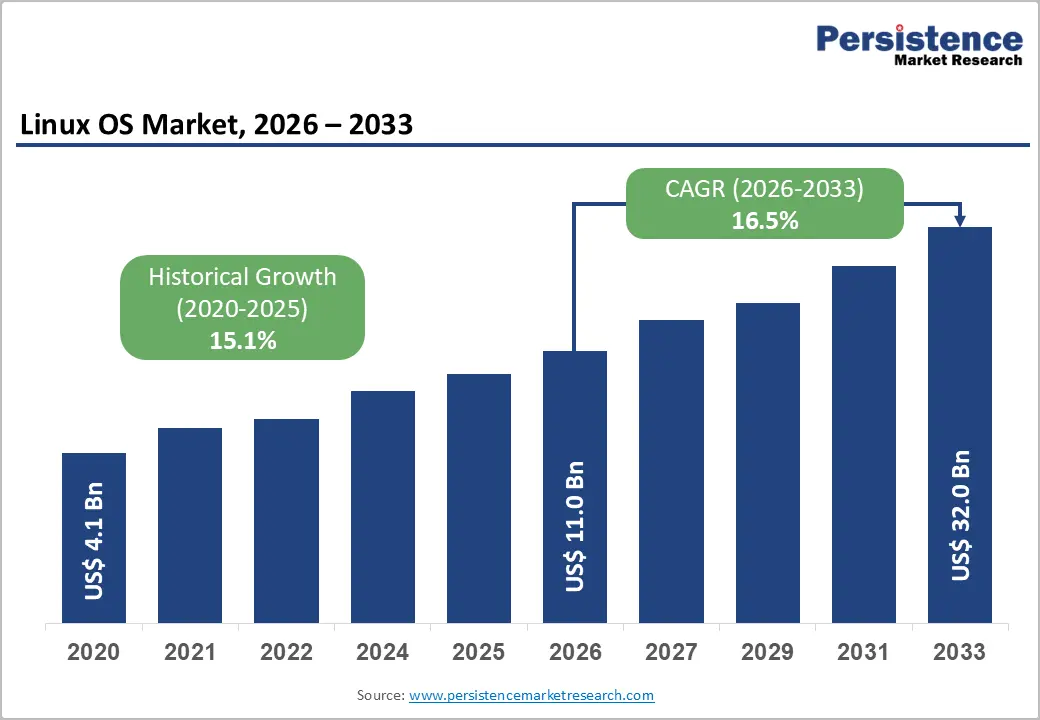

The global Linux operating system (OS) market is entering a phase of accelerated structural expansion, driven by deep transformations in enterprise IT architecture, cloud computing, edge infrastructure, and AI-enabled systems. Valued at approximately US$ 11.0 billion in 2026, the market is projected to reach US$ 32.0 billion by 2033, registering a strong CAGR of 16.5% during the forecast period.

This growth reflects a broader shift toward open-source infrastructure as organizations prioritize scalability, transparency, security, and cost efficiency in increasingly complex digital ecosystems. Linux, once considered a niche server OS, has now become a foundational layer for cloud-native computing, embedded systems, and high-performance workloads.

Key Market Drivers

- Accelerated Cloud Migration and Cloud-Native Transformation

One of the most powerful forces shaping Linux adoption is the rapid migration of enterprise workloads to cloud environments. Hyperscale cloud providers such as AWS, Microsoft Azure, and Google Cloud Platform have standardized much of their infrastructure on Linux-based systems, reinforcing its dominance in cloud computing.

Organizations are modernizing legacy IT systems and adopting:

- Containerized environments (Docker, Kubernetes)

- Microservices-based architectures

- Hybrid and multi-cloud deployments

Linux provides the flexibility, scalability, and cost efficiency required for these architectures. As cloud-native transformation deepens, Linux is becoming the default operating layer for enterprise application deployment.

Government institutions are also contributing to demand growth, particularly in regions prioritizing digital sovereignty and open-source policy frameworks.

- Expansion of Edge Computing, IoT, and Embedded Systems

The proliferation of edge computing and IoT devices is significantly expanding Linux deployment opportunities. Edge environments require lightweight, stable, and customizable operating systems—characteristics that align strongly with Linux.

Key application areas include:

- Industrial automation systems

- Smart manufacturing and robotics

- Connected vehicles and infotainment systems

- Telecommunications infrastructure

- Medical and diagnostic devices

Specialized distributions such as real-time Linux (PREEMPT_RT) and Yocto-based builds are enabling highly customized deployments tailored to hardware-specific needs.

As billions of connected devices are deployed globally, Linux continues to gain share as the preferred OS for embedded systems due to its reliability and long lifecycle support.

- Rising Cybersecurity and Transparency Requirements

Cybersecurity concerns are pushing enterprises toward open-source ecosystems. Linux offers transparent codebases that allow security teams to audit, modify, and harden systems as needed.

Unlike proprietary operating systems, Linux:

- Enables rapid vulnerability patching

- Supports community-driven security enhancements

- Provides customizable security modules (SELinux, AppArmor)

Organizations in regulated industries—such as finance, healthcare, and defense—are increasingly adopting Linux to meet compliance and governance requirements.

- AI, Machine Learning, and High-Performance Computing Expansion

The rapid rise of AI workloads is another major driver of Linux adoption. Modern AI infrastructure depends heavily on GPU-intensive computing environments, which are most efficiently supported by Linux-based systems.

Linux is widely used in:

- AI training clusters

- Deep learning pipelines

- High-performance computing (HPC) environments

- Cloud-based AI services

Its compatibility with frameworks such as TensorFlow, PyTorch, and CUDA makes it the preferred OS for AI infrastructure providers.

Market Restraints and Challenges

- Fragmentation Across Distributions

One of the most persistent challenges in the Linux ecosystem is distribution fragmentation. Enterprises often struggle with:

- Compatibility differences between distributions (RHEL, Ubuntu, Debian)

- Kernel version inconsistencies

- Package management variations

- Application portability issues

This fragmentation increases operational complexity and raises total cost of ownership (TCO), particularly for organizations managing large-scale deployments.

- Talent Shortage and Skill Gaps

A shortage of Linux-skilled professionals remains a major constraint on market expansion. Many enterprises face difficulties in hiring experts in:

- Linux system administration

- Cloud integration

- DevOps and container orchestration

- Security hardening

This skills gap is particularly pronounced in emerging economies, slowing down migration from legacy systems.

- Migration and Integration Complexity

Transitioning from proprietary operating systems to Linux-based environments can be complex. Enterprises often face:

- Legacy system compatibility issues

- Application rewriting requirements

- Infrastructure redesign challenges

These factors can delay adoption timelines and increase short-term implementation costs.

Market Opportunities

- Emerging Markets Digital Transformation

Emerging economies in Asia Pacific, Latin America, and Africa represent a significant growth frontier. Governments are increasingly adopting Linux to:

- Reduce software licensing costs

- Build sovereign digital infrastructure

- Expand public digital services

Linux is also being used in education systems to provide low-cost computing platforms.

- Expansion of Sovereign Cloud and Government IT Modernization

Governments worldwide are prioritizing sovereign cloud initiatives and secure digital infrastructure. Linux plays a central role in:

- Public administration systems

- Defense and cybersecurity platforms

- National data centers

Open-source adoption aligns with policies promoting independence from foreign software ecosystems.

- Growth in Software-Defined Vehicles and Automotive Systems

The automotive industry is rapidly shifting toward software-defined vehicles (SDVs). Linux is increasingly used in:

- Infotainment systems

- Advanced driver assistance systems (ADAS)

- Vehicle connectivity platforms

Its flexibility and real-time capabilities make it ideal for automotive innovation.

Segment Analysis

By Application

Servers (Dominant Segment)

Servers are expected to account for approximately 45% of market revenue in 2026. Linux dominates enterprise and cloud server environments due to:

- High scalability

- Strong virtualization support (KVM, Xen)

- Stability under heavy workloads

Embedded Systems (Fastest-Growing Segment)

Embedded Linux is expanding rapidly across industrial and consumer applications. Growth is driven by IoT proliferation and automotive digital transformation.

By End User

Enterprises (Leading Segment)

Enterprises account for roughly 58% of total market share. Linux is widely used for:

- Cloud-native applications

- Enterprise IT infrastructure

- DevOps pipelines

Government (Fastest-Growing Segment)

Government adoption is accelerating due to:

- Digital sovereignty initiatives

- Open-source policy frameworks

- Cost optimization mandates

Regional Analysis

North America

North America holds approximately 40% market share in 2026, driven by:

- Advanced cloud infrastructure

- Strong enterprise IT maturity

- Presence of hyperscalers (AWS, Azure, Google Cloud)

The United States leads regional adoption across finance, defense, and technology sectors.

Europe

Europe is driven by strict data protection regulations such as GDPR. Governments and enterprises are increasingly adopting Linux to ensure:

- Data sovereignty

- Regulatory compliance

- Reduced dependency on proprietary systems

Countries like Germany, France, and the UK are leading adoption.

Asia Pacific (Fastest-Growing Region)

Asia Pacific is expected to be the fastest-growing region due to:

- Rapid digital transformation in India and China

- Government-backed open-source initiatives

- Expansion of cloud infrastructure

Southeast Asia is also emerging as a strong growth hub for Linux-based innovation.

Competitive Landscape

The Linux OS market is moderately fragmented, with a mix of enterprise vendors and community-driven distributions.

Key Players Include:

- IBM (Red Hat)

- Canonical Ltd.

- SUSE LLC

- Oracle Corporation

- Amazon Web Services

- Google LLC

- Microsoft Corporation

These companies focus on enterprise support, cloud integration, and managed Linux distributions.

Recent Industry Developments

- NVIDIA released the 595 Linux graphics driver series, improving Vulkan support for high-performance computing workloads.

- Oracle introduced updates to its Unbreakable Enterprise Kernel with enhancements in security and memory management.

- Intel discontinued its Clear Linux OS, signaling consolidation in the enterprise distribution landscape.

- Kali Linux 2026.1 introduced new tools and usability improvements for cybersecurity professionals.

Future Outlook

The Linux OS market is expected to evolve along three major trajectories:

- Cloud dominance – Linux will remain the core OS for cloud-native ecosystems.

- Edge expansion – Embedded Linux will power billions of IoT devices globally.

- AI infrastructure integration – Linux will become the default OS for AI and HPC workloads.

As enterprises continue to modernize IT infrastructure, Linux is transitioning from an alternative operating system to a foundational digital infrastructure layer.

Conclusion

The global Linux OS market is undergoing a structural transformation driven by cloud computing, AI adoption, edge expansion, and open-source governance models. While challenges such as fragmentation and skill shortages persist, strong enterprise demand and government support are expected to sustain long-term growth.

With the market projected to reach US$ 32.0 billion by 2033, Linux is positioned not just as an operating system, but as a critical enabler of next-generation digital ecosystems across industries worldwide.

Related Reports: