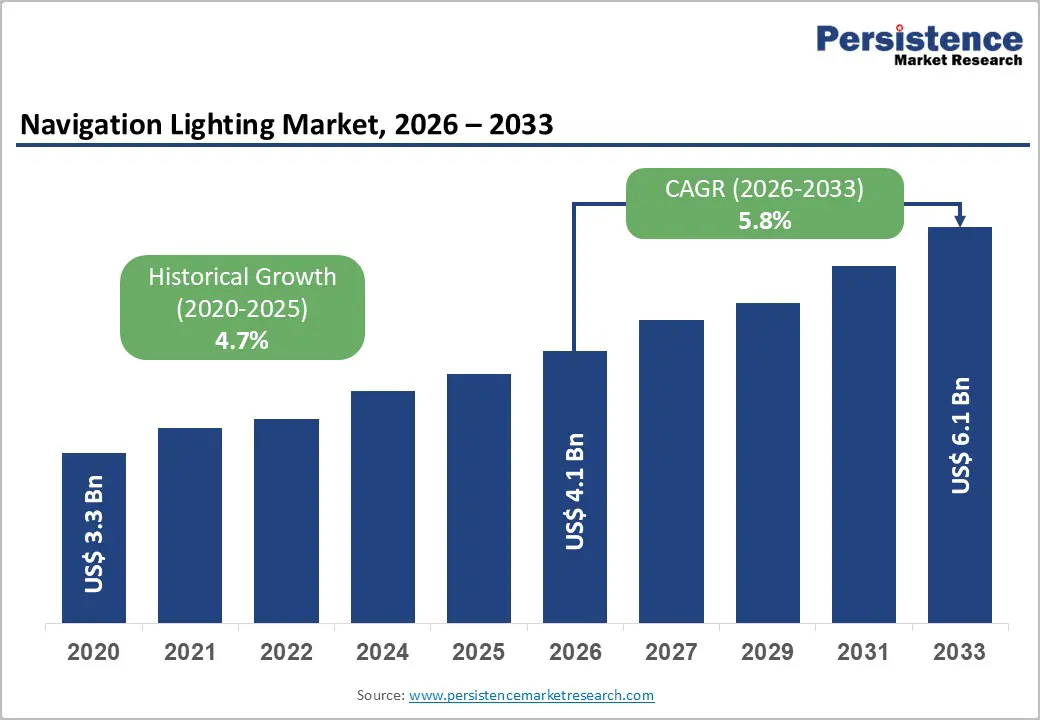

The global navigation lighting market is emerging as a critical safety and compliance-driven segment across marine, aviation, and infrastructure ecosystems. Valued at approximately US$4.1 billion in 2026, the market is projected to reach US$6.1 billion by 2033, expanding at a CAGR of 5.8% during the forecast period. This steady growth reflects a combination of regulatory enforcement, modernization of global transport infrastructure, and rapid adoption of energy-efficient LED-based lighting systems.

Navigation lighting systems are not optional components; they are mandated safety requirements under international maritime and aviation regulations. As global trade intensifies and air traffic expands, the need for reliable, durable, and compliant lighting systems continues to rise, supporting long-term market stability.

Market Overview and Structural Dynamics

The navigation lighting market operates at the intersection of safety compliance, transportation infrastructure, and energy efficiency innovation. Over 80% of global trade by volume is transported through maritime routes, making marine shipping the dominant application segment.

At the same time, aviation infrastructure upgrades and smart city development projects are expanding the scope of navigation lighting beyond traditional marine applications. Airports, offshore platforms, wind farms, and industrial zones increasingly rely on advanced lighting systems for visibility, hazard prevention, and operational continuity.

The market is undergoing a structural transformation driven by three key forces:

- Transition from incandescent and halogen systems to LED technology

- Increasing regulatory scrutiny and global safety standards

- Integration of smart monitoring and predictive maintenance systems

Key Market Highlights

- Market Size (2026): US$4.1 Billion

- Forecast Value (2033): US$6.1 Billion

- CAGR (2026–2033): 5.8%

- Historical CAGR (2020–2025): 4.7%

Regional Leadership

Asia Pacific dominates with approximately 36.7% market share, driven by shipbuilding hubs, port modernization, and aviation expansion.

Dominant Product Segment

- Sidelights hold around 30.5% share, due to regulatory mandates across all vessel categories.

Leading Installation Type

- Portable systems lead with 40.4% share, supported by flexibility and emergency deployment applications.

Key Growth Drivers

- Regulatory Compliance as a Structural Demand Base

Navigation lighting is fundamentally governed by strict international safety regulations across maritime and aviation sectors. Organizations such as the International Maritime Organization (IMO) define detailed lighting requirements for vessels of different sizes and categories.

Similarly, aviation authorities mandate precise lighting standards for aircraft and ground infrastructure to ensure visibility and collision avoidance.

This creates:

- Non-discretionary demand

- Continuous replacement cycles

- Mandatory upgrade requirements

Even during economic downturns, compliance obligations ensure stable market demand.

- Transition Toward LED-Based Lighting Systems

The shift to LED technology is one of the most transformative trends in the market. LEDs offer:

- Lower energy consumption

- Longer operational lifespan

- Reduced maintenance requirements

- Better performance in harsh environments

For marine and aviation operators, where maintenance access is difficult and costly, LED systems significantly reduce lifecycle costs.

Additionally, regulatory push toward energy efficiency is accelerating adoption. This transition is also increasing average selling prices, contributing to overall market value expansion.

- Expansion of Global Maritime Trade and Fleet Size

Global maritime trade continues to grow steadily, increasing the installed base of navigation lighting systems. Rising vessel production, longer shipping routes, and increased port activity all contribute to higher demand.

Key impacts include:

- Expansion of commercial shipping fleets

- Growth in offshore energy operations

- Increased replacement demand for aging vessels

Harsh marine environments also necessitate corrosion-resistant and high-durability lighting systems, further driving upgrades.

Restraints Impacting Market Growth

High Certification and Compliance Complexity

Navigation lighting systems must undergo rigorous testing and certification before deployment. This increases:

- Product development timelines

- Engineering costs

- Time-to-market for manufacturers

Smaller operators often face difficulties in adopting advanced systems due to compliance complexity and integration challenges.

Price Sensitivity in Emerging Markets

Despite long-term cost savings, LED-based navigation lighting systems have higher upfront costs compared to conventional alternatives. This creates resistance among:

- Small vessel operators

- Inland water transport services

- Cost-sensitive aviation infrastructure projects

Supply Chain Disruptions

Global supply chain volatility affects:

- Electronic component availability

- Manufacturing lead times

- Logistics and distribution costs

These challenges particularly impact smaller manufacturers dependent on outsourced components.

Key Opportunities

Retrofit Market Expansion

One of the most significant opportunities lies in retrofitting existing fleets. A large portion of the global vessel base still operates on legacy incandescent or halogen systems.

Retrofit benefits include:

- Immediate compliance upgrades

- Energy savings

- Reduced maintenance costs

Plug-and-play LED retrofit kits are gaining strong traction in commercial shipping, recreational boating, and inland waterways.

Solar and Portable Lighting Solutions

Portable and solar-powered navigation lighting systems are expanding rapidly, particularly in:

- Remote ports

- Offshore energy projects

- Temporary construction zones

- Emergency response operations

Advancements in battery storage and photovoltaic efficiency are improving reliability, making these systems increasingly viable for harsh environments.

Smart and Connected Lighting Systems

The integration of IoT-enabled monitoring is reshaping the industry. Smart navigation lighting systems now offer:

- Real-time performance tracking

- Automated fault detection

- Predictive maintenance alerts

This reduces downtime and enhances operational efficiency, especially in large fleets and aviation infrastructure.

Segment Analysis

Light Type: Sidelights and Masthead Lights

Sidelights dominate the market due to regulatory mandates across all vessel categories. They are essential for collision avoidance and visibility in all operating conditions.

Masthead lights are the fastest-growing segment, driven by:

- Fleet modernization

- Adoption of LED systems

- Enhanced visibility requirements in congested waters

Modern vessels increasingly use integrated LED lighting systems that combine multiple functions into compact units.

Installation Type: Portable vs Fixed Systems

Portable systems lead the market due to:

- Ease of deployment

- Suitability for temporary operations

- Use in emergency and defense applications

Fixed installations are the fastest-growing segment, supported by:

- Large commercial vessels

- Offshore platforms

- Airports and infrastructure projects

Fixed systems are increasingly integrated with smart monitoring platforms for improved lifecycle management.

Regional Insights

Asia Pacific: Market Leader and Fastest Growing Region

Asia Pacific dominates global demand due to:

- Strong shipbuilding industry in China, Japan, South Korea, and India

- Expanding aviation infrastructure

- Rapid port modernization projects

Government investments in infrastructure and maritime trade expansion further strengthen regional dominance.

North America: Compliance-Driven Modernization

North America shows strong demand driven by:

- Regulatory enforcement

- Naval modernization programs

- Recreational boating market

LED retrofit adoption is particularly strong in marine and aviation infrastructure.

Europe: Technology and Sustainability Focus

Europe remains a mature but innovation-driven market. Key characteristics include:

- Strict energy efficiency regulations

- Strong offshore wind sector

- Advanced naval and aerospace industries

European manufacturers focus heavily on high-performance, compact, and smart lighting systems.

Competitive Landscape

The navigation lighting market is moderately fragmented, with competition based on:

- Product reliability

- Certification compliance

- LED innovation

- Durability in extreme environments

Key companies include:

Glamox AS, Koito Manufacturing Co., Ltd., Dialight plc, Perko Inc., and Hella Marine among others.

These companies are increasingly investing in:

- Smart lighting systems

- LED retrofit solutions

- Integrated monitoring platforms

- Energy-efficient product portfolios

Recent Industry Developments

In March 2026, manufacturers introduced advanced wireless lighting control systems and high-efficiency LED luminaires, signaling a shift toward connected and automated lighting ecosystems. This reflects a broader industry trend toward digitalization, where navigation lighting is becoming part of intelligent transport infrastructure systems.

Conclusion

The navigation lighting market is set for steady and resilient growth through 2033, supported by regulatory mandates, global trade expansion, and rapid LED adoption. While cost pressures and certification complexity remain challenges, strong retrofit demand and smart lighting integration present significant long-term opportunities.

As maritime, aviation, and infrastructure sectors continue modernizing, navigation lighting is evolving from a basic safety requirement into a technologically advanced, energy-efficient, and connected system essential for global transport safety.

Related Reports: