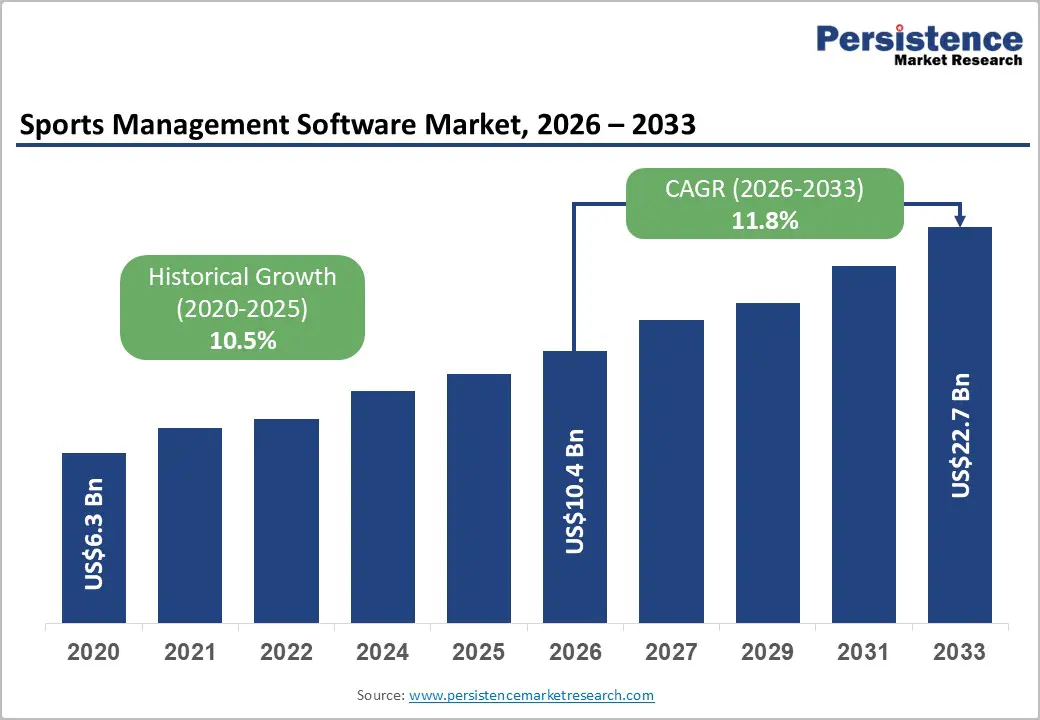

The global sports management software market is entering a phase of strong structural growth, driven by the rapid digital transformation of sports organizations across amateur, collegiate, and professional levels. Valued at approximately US$10.4 billion in 2026, the market is projected to reach US$22.7 billion by 2033, expanding at a CAGR of 11.8% during the forecast period. This expansion reflects a broader shift from manual, fragmented administrative processes toward integrated digital platforms that streamline operations such as registration, scheduling, payments, communication, analytics, and fan engagement.

As sports participation rises globally and organizations increasingly prioritize automation and data-driven decision-making, sports management software is becoming a foundational technology layer across the industry.

Market Overview

Sports management software refers to digital platforms designed to help sports organizations manage operational, administrative, and performance-related activities. These systems are widely used by clubs, leagues, schools, academies, and professional teams to coordinate players, coaches, administrators, and fans within a unified ecosystem.

The market’s expansion is strongly supported by the adoption of SaaS-based delivery models, which reduce upfront infrastructure costs and allow organizations of all sizes to access advanced tools. Additionally, increasing participation in organized sports—both team-based and individual—has intensified the need for scalable systems capable of handling complex scheduling, communication, and financial workflows.

Key Market Highlights

- Market Size (2026E): US$10.4 billion

- Market Forecast (2033F): US$22.7 billion

- CAGR (2026–2033): 11.8%

- Leading Region: North America (43.2% share)

- Fastest-Growing Region: Asia Pacific

- Leading Deployment: Cloud (54.8% share)

- Dominant Application: Player & Team Management (41.3% share)

North America continues to dominate due to early SaaS adoption and strong sports infrastructure, while Asia Pacific is emerging as the fastest-growing region, fueled by digitalization and rising grassroots sports participation.

Market Drivers

- Rising Participation in Organized Sports

One of the most significant drivers of the sports management software market is the increasing participation in organized sports activities. Youth leagues, school tournaments, amateur clubs, and recreational sports programs are expanding rapidly across both developed and emerging economies.

This growth creates substantial administrative complexity. Organizations must manage large volumes of registrations, player rosters, scheduling updates, payments, and communication across multiple stakeholders. Traditional manual systems are no longer sufficient, driving strong demand for automated digital platforms.

As participation continues to grow globally, particularly in Asia Pacific and Latin America, the demand for scalable software solutions is expected to rise in parallel.

- Expansion of Cloud and SaaS-Based Platforms

Cloud computing has become a cornerstone of the sports management software ecosystem. SaaS-based platforms are increasingly preferred due to their affordability, scalability, and ease of deployment.

Key advantages include:

- Real-time access to data from multiple devices

- Reduced IT infrastructure and maintenance costs

- Seamless updates and integrations

- Support for multi-location sports organizations

This transition has significantly expanded the addressable market, particularly among small and medium-sized sports organizations that previously lacked access to enterprise-grade systems.

- Integration of AI and Advanced Analytics

Artificial intelligence and analytics are transforming sports management software from basic administrative tools into intelligent decision-support systems.

AI-enabled features now include:

- Automated scheduling optimization

- Predictive performance analytics

- Resource allocation planning

- Injury risk and workload insights

These capabilities improve operational efficiency while enhancing competitive performance and strategic planning. Vendors offering advanced analytics are gaining a competitive advantage through higher user engagement and improved customer retention.

Market Restraints

- Data Privacy and Security Concerns

Sports organizations handle sensitive personal data, including athlete profiles, payment information, and in many cases, data related to minors. This creates strong regulatory obligations around data protection and cybersecurity.

Cloud-based platforms, while efficient, increase exposure to cyber risks if not properly secured. Compliance with frameworks such as GDPR and other regional regulations adds operational complexity and cost, particularly for smaller organizations.

- Cost Sensitivity and Market Fragmentation

The market is highly fragmented, ranging from small community clubs to large professional organizations. This creates significant variation in budget capacity and technology adoption readiness.

Smaller organizations often prioritize low-cost solutions and may delay adoption of comprehensive platforms unless clear ROI is demonstrated. As a result, vendors face pricing pressure and longer sales cycles, especially in highly competitive segments.

Market Opportunities

- Growth in Event and League Management Solutions

Event and league management is emerging as one of the fastest-growing segments in the market. The increasing complexity of tournaments, multi-venue competitions, and seasonal leagues has created demand for automation.

Key functionalities include:

- AI-based scheduling

- Bracket generation

- Venue allocation

- Real-time updates and notifications

These tools significantly reduce manual workload and improve operational accuracy, making them highly valuable for organizers.

- Expansion in Emerging Markets

Emerging economies across Asia Pacific, Latin America, and Africa represent major growth opportunities. These regions are experiencing:

- Rising sports participation

- Rapid mobile adoption

- Expanding digital payment ecosystems

- Government-backed digital infrastructure initiatives

Mobile-first platforms are particularly important in these markets, where smartphones are often the primary access point for digital services. Vendors that localize their solutions will be well-positioned to capture this growth.

- Fan Engagement and Monetization Integration

Sports organizations are increasingly using management platforms to enhance revenue generation. By integrating fan engagement tools, ticketing systems, and sponsorship management, software providers are enabling organizations to monetize digital interactions more effectively.

This convergence of operations and engagement is shifting the market from administrative software toward full-scale digital ecosystems.

Segment Analysis

Application: Player & Team Management Dominates

Player and team management is expected to hold approximately 41.3% of the market share. This segment includes core functionalities such as:

- Roster management

- Scheduling

- Attendance tracking

- Communication tools

- Payment processing

These features are essential for daily operations, making this segment the primary entry point for most organizations adopting sports management software.

Fastest-Growing Segment: Event & League Management

Event and league management is witnessing rapid growth due to the increasing scale and complexity of sports competitions. Automation tools for scheduling, logistics, and communication are becoming essential for efficient tournament operations.

Platforms that integrate analytics, ticketing, and live updates are further expanding revenue opportunities for organizers.

Deployment Analysis

Cloud Deployment Leads the Market

Cloud deployment dominates the market with a 54.8% share and continues to grow rapidly. Its advantages include:

- Lower cost of ownership

- Easy scalability

- Remote accessibility

- Seamless integration capabilities

Cloud-based systems are particularly effective for organizations managing multiple teams or locations, making them the preferred deployment model across all segments of the market.

Regional Insights

North America

North America leads the global market with a 43.2% share, driven by:

- High sports participation rates

- Mature SaaS ecosystem

- Strong youth and collegiate sports systems

- Early adoption of digital platforms

The U.S. remains the dominant contributor, supported by established companies like TeamSnap and SportsEngine. Continuous innovation in AI-driven scheduling and platform consolidation is further strengthening the region’s leadership.

Europe

Europe represents a mature and regulated market with strong emphasis on compliance, governance, and data protection. Countries such as the UK, Germany, France, and Spain are key contributors.

The region is increasingly focused on:

- Secure cloud adoption

- Fan engagement monetization

- Sports data analytics

Companies like Deltatre and Genius Sports are driving innovation in digital broadcasting and performance analytics.

Asia Pacific

Asia Pacific is the fastest-growing region, supported by:

- Expanding sports infrastructure

- Rapid digital transformation

- Mobile-first adoption

- Government support for digital ecosystems

Countries such as India, China, and Japan are driving growth. The rise of affordable mobile platforms and cloud services is enabling widespread adoption across grassroots and professional levels.

Competitive Landscape

The market is highly competitive and moderately fragmented, with a mix of global platforms and niche providers. However, consolidation is increasing as companies aim to offer integrated ecosystems rather than standalone solutions.

Key strategies include:

- AI-driven product innovation

- Subscription-based SaaS models

- Strategic partnerships and acquisitions

- Geographic expansion into emerging markets

Recent Developments

- TeamSnap ONE (2025): Integrated platform combining registration, scheduling, communication, and streaming.

- Fastbreak AI (2025): AI-powered scheduling engine enabling rapid tournament planning.

Key Players

Major companies operating in the market include:

TeamSnap, SportsEngine, Stack Sports, PlayMetrics, LeagueApps, Active Network, Jonas Software, Hudl, Catapult, Genius Sports, Deltatre, Teamworks, Omnify, EZFacility, Virtuagym, and PerfectMind.

Conclusion

The sports management software market is undergoing a strong transformation driven by digitalization, cloud adoption, and AI integration. As sports organizations increasingly shift toward centralized digital ecosystems, demand for scalable, intelligent, and user-friendly platforms will continue to rise.

With robust growth projected through 2033, the market presents significant opportunities for vendors that can combine operational efficiency with advanced analytics and fan engagement capabilities. North America will continue to lead, while Asia Pacific will emerge as the primary growth engine, shaping the next phase of global expansion.

Related Reports: