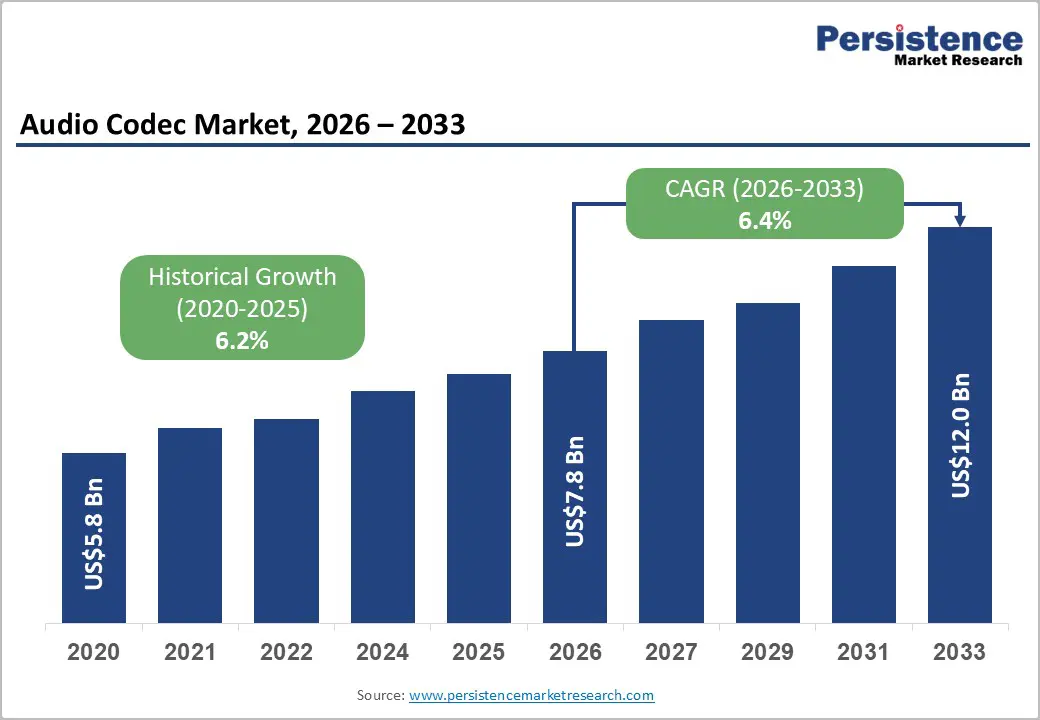

The global audio codec market is entering a phase of steady but structurally important transformation. Valued at US$7.8 billion in 2026, the market is projected to reach US$12.0 billion by 2033, expanding at a CAGR of 6.4% during the forecast period. This growth is being driven by the convergence of high-speed connectivity, rising demand for immersive audio experiences, and the rapid expansion of wireless and software-defined audio ecosystems.

Historically, audio codecs were primarily associated with smartphones and basic voice compression. Today, they have become foundational to a wide range of digital ecosystems, including streaming platforms, automotive infotainment systems, smart wearables, gaming environments, and next-generation telecommunications networks.

As the digital economy expands, audio codecs are evolving from hardware-bound components into highly flexible, software-integrated technologies that enable high-efficiency compression, ultra-low latency communication, and high-fidelity audio delivery across devices and networks.

Market Overview and Structural Evolution

The audio codec industry is undergoing a major structural shift. Traditionally, codec development focused on hardware-based compression embedded in mobile devices. However, the rise of cloud computing, software-defined networking, and AI-enhanced media processing has significantly broadened the scope of the market.

Modern audio codecs now operate across a hybrid architecture that includes:

- Hardware-embedded codecs in chipsets and SoCs

- Software codecs in streaming and communication platforms

- Cloud-based audio processing pipelines

- AI-enhanced adaptive audio systems

This transition is enabling a more scalable and flexible audio ecosystem where quality, latency, and bandwidth efficiency are dynamically optimized based on user conditions and device capabilities.

The increasing importance of real-time communication, especially in gaming, remote collaboration, and virtual environments, is further accelerating demand for next-generation codecs that can deliver consistent performance under variable network conditions.

Key Market Highlights

- Market Size (2026): US$7.8 Billion

- Forecast Value (2033): US$12.0 Billion

- CAGR (2026–2033): 6.4%

- Historical Growth (2020–2025): 6.2%

Regional Leadership

- North America: ~40.3% market share

- Asia Pacific: Fastest-growing region

Segment Leadership

- Product Type: Lossy codecs (41.9% share)

- Component: Hardware codecs (59.5% share)

Key Growth Drivers

Rising Connectivity Density and Streaming Consumption

The global expansion of high-speed internet and mobile connectivity is a foundational driver of the audio codec market. With billions of users consuming digital audio and video content daily, codecs play a critical role in compressing and transmitting audio efficiently.

Streaming platforms such as music services, OTT video providers, and podcast ecosystems rely heavily on optimized codecs to balance quality and bandwidth consumption. As consumer expectations for high-resolution audio increase, codec technologies are being pushed to deliver better clarity with lower latency and reduced data usage.

This demand is particularly strong in emerging markets, where mobile-first consumption patterns dominate digital behavior.

Expansion of Bluetooth LE Audio and Low-Power Wireless Ecosystems

One of the most transformative developments in the market is Bluetooth LE Audio. Powered by the LC3 codec, this technology enables:

- Higher audio quality at lower bitrates

- Reduced power consumption

- Multi-stream audio capabilities

- Improved accessibility for hearing devices

This innovation is particularly impactful for:

- Wireless earbuds

- Smartwatches

- Hearing aids

- IoT audio devices

As battery life and portability become critical design factors, low-power codecs are increasingly becoming a standard requirement rather than a premium feature.

Growth of Immersive Audio in Automotive and Telecom

The integration of immersive audio experiences is expanding across both telecommunications and automotive industries. Voice communication is shifting from traditional mono audio to spatial and high-definition formats, improving clarity and user engagement.

In the automotive sector, vehicles are evolving into connected entertainment hubs. Modern infotainment systems support:

- Streaming platforms

- Voice assistants

- Personalized sound zones

- Spatial surround audio

Automakers are partnering with audio technology providers to enhance in-cabin experiences, especially in electric and autonomous vehicles where digital engagement is central.

Market Restraints

Codec Fragmentation and Licensing Complexity

The presence of multiple competing codec standards creates significant challenges for manufacturers and developers. These include:

- Licensing and royalty costs

- Compatibility issues across platforms

- Integration complexity

- Regulatory compliance burdens

Proprietary codecs often require expensive licensing agreements, which can limit adoption in cost-sensitive markets.

Power, Latency, and Cost Trade-offs

Despite technological progress, codec implementation must balance three critical constraints:

- Power efficiency

- Processing latency

- Hardware cost

This balancing act becomes particularly difficult in compact devices such as wearables and entry-level smartphones, where processing resources are limited.

Real-time applications such as gaming and VoIP communication also require ultra-low latency performance, increasing engineering complexity.

Market Opportunities

Connected Vehicles and In-Cabin Audio Systems

The automotive sector represents one of the most promising growth avenues for audio codecs. Modern vehicles are increasingly software-defined environments that rely on digital audio systems for entertainment and communication.

Opportunities include:

- Spatial and immersive audio systems

- Multi-zone personalized audio

- Real-time voice communication systems

- Integrated streaming platforms

Electric and autonomous vehicles, in particular, are accelerating demand for advanced infotainment architectures. This creates strong opportunities for long-term partnerships between codec developers and automotive OEMs.

Accessibility and Assistive Audio Technologies

Accessibility-focused audio technologies are gaining importance across public infrastructure and consumer electronics. Advanced codecs now support:

- Broadcast audio for public spaces

- Real-time audio sharing

- Enhanced hearing aid integration

Applications include airports, hospitals, educational institutions, and transportation systems. Regulatory support for accessibility standards further strengthens this segment.

Emerging Markets and 5G Expansion

The rollout of 5G networks across Asia, Latin America, and parts of Africa is unlocking new opportunities for high-quality audio services. As smartphone penetration increases, users are consuming more:

- Streaming music

- Video content

- Real-time communication apps

This shift is driving large-scale adoption of efficient audio codecs optimized for mobile networks.

Segment Analysis

Product Type Insights

Lossy Codecs (Market Leader – 41.9% share)

Lossy codecs dominate due to their efficiency in compressing audio data while maintaining acceptable quality. Formats such as MP3, AAC, and Opus are widely used in streaming platforms, VoIP services, and mobile applications.

Their ability to reduce bandwidth usage makes them essential for large-scale digital ecosystems.

Lossless Codecs (Fastest Growing Segment)

Lossless codecs such as FLAC and ALAC are gaining traction due to rising demand for high-resolution audio. This is especially evident in:

- Premium streaming services

- Professional audio production

- Gaming and immersive media

As network capacity improves, adoption of lossless formats is expected to accelerate.

Component Insights

Hardware Codecs (Dominant – 59.5% share)

Hardware codecs remain essential for real-time, low-power audio processing. They are widely integrated into smartphones, automotive systems, and IoT devices. Their efficiency and reliability ensure continued dominance in embedded applications.

Software Codecs (Fastest Growing Segment)

Software codecs are gaining momentum due to their flexibility and upgradability. They are widely used in:

- Streaming platforms

- Video conferencing tools

- Cloud-based communication systems

Hybrid models combining hardware acceleration and software adaptability are becoming increasingly common.

Regional Analysis

North America

North America leads the global market with approximately 40.3% share. The region benefits from:

- High 5G penetration

- Strong consumer spending

- Advanced semiconductor ecosystem

- Leadership in streaming innovation

Companies such as Qualcomm, Dolby Laboratories, and Apple are driving innovation in spatial audio and low-latency codecs.

The U.S. remains the primary innovation hub, particularly in immersive audio formats used in entertainment and gaming.

Europe

Europe’s market is shaped by strong regulatory frameworks and a focus on standardization. Countries such as Germany, France, and the U.K. lead adoption in automotive and broadcasting applications.

European innovation centers, including Fraunhofer IIS, continue to influence global codec standards such as MPEG-H and xHE-AAC.

The region also emphasizes accessibility and inclusive audio technologies, particularly in public broadcasting and transport systems.

Asia Pacific

Asia Pacific is the fastest-growing region due to:

- Massive smartphone user base

- Rapid 5G deployment

- Strong electronics manufacturing ecosystem

China, Japan, and India are key contributors. Companies like Huawei, Xiaomi, Sony, and MediaTek are driving large-scale adoption of efficient audio codec technologies.

The region’s expanding EV and OTT ecosystems are further accelerating demand.

Competitive Landscape

The audio codec market is moderately fragmented, with competition spanning semiconductor firms, software providers, and audio technology specialists.

Key competitive strategies include:

- Investment in R&D for low-power codecs

- Expansion into automotive audio systems

- Development of AI-enhanced audio processing

- Strategic licensing agreements

- Ecosystem partnerships with device manufacturers

Key Industry Developments

- January 2025: Samsung and Google introduced Eclipsa Audio, an open-standard immersive audio format designed for 3D audio experiences.

- June 2025: Apple launched its Spatial Audio Format (ASAF), enhancing immersive sound across devices and mixed reality environments.

Key Companies

Qualcomm, Cirrus Logic, MediaTek, Realtek Semiconductor, Texas Instruments, Analog Devices, STMicroelectronics, NXP Semiconductors, Renesas Electronics, ROHM Semiconductor, Sony Group Corporation, Dolby Laboratories, Synopsys, Fraunhofer IIS, Broadcom, Apple.

Conclusion

The audio codec market is evolving from a foundational compression technology into a core enabler of modern digital experiences. As connectivity expands and user expectations shift toward immersive, high-quality, and low-latency audio, codecs are becoming central to multiple industries including telecommunications, automotive, consumer electronics, and streaming media.

Between 2026 and 2033, the market’s steady expansion will be shaped by software-defined audio architectures, AI-driven enhancements, and the widespread adoption of wireless and immersive audio ecosystems. While challenges such as fragmentation and licensing complexity remain, innovation in low-power and high-efficiency codecs will continue to unlock new opportunities across both developed and emerging markets.

Related Reports: