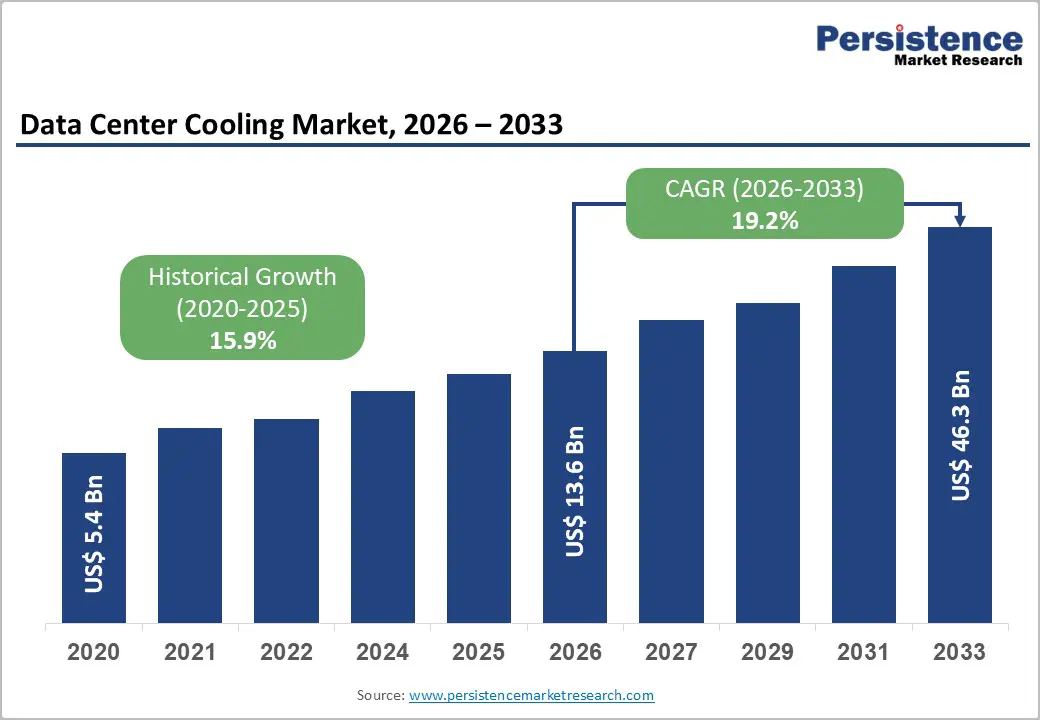

The global data center cooling market is undergoing a fundamental transformation as digital infrastructure shifts toward high-density computing, AI workloads, and sustainability-driven operations. Valued at US$13.6 billion in 2026, the market is projected to surge to US$46.3 billion by 2033, reflecting a strong CAGR of 19.2% during the forecast period. This rapid expansion is being shaped by structural changes in data center architecture, increasing thermal loads from advanced computing systems, and mounting regulatory pressure to reduce energy consumption and carbon emissions.

Traditional air-based cooling systems, once sufficient for conventional workloads, are now reaching their operational limits. Modern AI and high-performance computing (HPC) environments routinely exceed rack densities of 20–30 kW, with next-generation GPU clusters pushing far beyond 50–100 kW per rack. This shift is accelerating the adoption of liquid cooling technologies, hybrid cooling architectures, and AI-driven thermal optimization systems that can maintain performance stability while improving Power Usage Effectiveness (PUE).

Structural Shift Toward High-Density Computing

One of the most significant forces driving the data center cooling market is the rapid expansion of AI, machine learning, and HPC workloads. These applications require dense server configurations with significantly higher power consumption and heat output than traditional enterprise IT systems. A single AI accelerator can generate over 1,200 watts under peak load, and large-scale deployments of such processors create intense thermal environments that conventional air conditioning systems struggle to manage efficiently.

As a result, operators are increasingly redesigning cooling infrastructure to accommodate liquid-based solutions such as direct-to-chip cooling, rear-door heat exchangers, and full immersion cooling systems. These technologies offer superior heat transfer efficiency compared to air, enabling data centers to operate at higher densities without compromising uptime or reliability. This structural shift is redefining the foundation of thermal management strategies across hyperscale and enterprise facilities.

Market Drivers

Rise of AI and HPC Workloads

The accelerating deployment of generative AI platforms, large language models, and advanced analytics is fundamentally reshaping cooling requirements. These workloads significantly increase power density, forcing operators to adopt advanced cooling solutions capable of handling extreme thermal loads. Hyperscale cloud providers and AI-focused data centers are leading this transition, investing heavily in liquid cooling systems to ensure operational stability and energy efficiency.

Sustainability Regulations and Net-Zero Targets

Environmental regulations and corporate sustainability commitments are also playing a crucial role in market expansion. Governments across North America, Europe, and Asia Pacific are enforcing stricter energy efficiency standards for data centers. The European Union’s Energy Efficiency Directive and Green Deal policies are pushing operators to continuously reduce PUE levels, while the U.S. Department of Energy has introduced initiatives aimed at lowering federal data center energy consumption.

Liquid cooling systems are increasingly favored because they can achieve PUE levels below 1.2, compared to 1.4–1.6 for traditional air-cooled systems. This translates into 30–40% energy savings in cooling operations. Additionally, Nordic countries are promoting waste heat recovery systems, where excess thermal energy from data centers is reused in district heating networks, further strengthening demand for advanced cooling infrastructure.

Market Restraints

Despite strong growth potential, the market faces notable challenges. High capital expenditure remains a major barrier, particularly for retrofitting legacy data centers. Transitioning from air-based systems to liquid cooling requires significant infrastructure upgrades, including piping systems, coolant distribution units, and specialized containment structures. These upgrades can increase upfront costs by 20–40%, although long-term operational savings often justify the investment within a 2–4 year period.

Operational complexity is another restraint. The introduction of liquid cooling raises concerns around coolant leakage, maintenance requirements, and system reliability. Many operators remain cautious, especially in multi-tenant colocation environments where hardware ownership and liability are shared. The need for skilled technicians and specialized training further slows adoption in some regions.

Emerging Opportunities

The evolution of AI-driven thermal management systems presents a major growth opportunity. Modern coolant distribution units (CDUs) are now being equipped with predictive analytics capabilities that optimize cooling based on real-time workload patterns. These systems can reduce pump energy consumption by up to 20%, significantly improving overall efficiency.

Immersion cooling is also emerging as a commercially viable solution beyond pilot deployments. Modular immersion cooling pods are being developed to support rack densities of up to 140 kW, making them particularly suitable for AI clusters and edge data centers. Companies collaborating with GPU manufacturers such as NVIDIA and AMD are gaining a competitive advantage by co-engineering optimized thermal solutions for next-generation chipsets.

Another promising opportunity lies in heat recovery and circular energy models. Data centers are increasingly being integrated into urban energy ecosystems where waste heat is repurposed for residential heating, agricultural applications, or industrial processes. In some cases, up to 70–80% of rejected heat energy can be recovered and reused, transforming cooling systems from cost centers into revenue-generating assets.

Segment Analysis

By Component

Solutions dominate the market, accounting for over 74% share in 2026. This includes CRAC and CRAH units, liquid cooling loops, containment systems, and chillers that collectively form the backbone of data center thermal infrastructure. The growing demand for integrated and scalable systems is reinforcing this dominance, particularly in hyperscale environments.

Services represent the fastest-growing segment as operators increasingly rely on predictive maintenance, system optimization, and lifecycle management. As cooling environments become more complex, specialized expertise is required to ensure efficiency, minimize downtime, and support retrofitting initiatives.

By Technology

Air cooling continues to hold a leading share of over 53% due to its cost-effectiveness and widespread adoption in existing infrastructure. It remains the preferred option for moderate-density workloads and legacy facilities.

However, liquid cooling is the fastest-growing technology segment, projected to expand at a CAGR of 26.4% through 2033. Its ability to manage high-density workloads efficiently makes it essential for AI and HPC applications. The shift toward chip-level cooling is accelerating adoption across hyperscale data centers globally.

By Data Center Size

Large data centers account for more than 58% of the market, driven by their massive IT loads and scalability requirements. These facilities prioritize redundancy, energy optimization, and advanced cooling architectures.

Small and medium-sized data centers are experiencing rapid growth due to the rise of edge computing. These facilities require compact, modular cooling systems that are easy to deploy and maintain while offering high energy efficiency.

By End User

Hyperscale data centers lead the market with over 35% share, driven by exponential growth in cloud computing and AI workloads. Their large-scale infrastructure demands highly efficient cooling systems to manage extreme heat loads.

Cloud providers are emerging as the fastest-growing end-user segment, fueled by rising enterprise migration to cloud platforms, SaaS adoption, and digital transformation initiatives. Their expansion is directly increasing demand for scalable and sustainable cooling solutions.

Regional Insights

North America leads the global market with over 36% share, supported by strong hyperscale infrastructure and early adoption of AI technologies. The United States alone accounts for a significant portion of global data center electricity consumption, with major hubs such as Northern Virginia driving large-scale deployments. Regulatory initiatives focused on energy efficiency are further accelerating adoption of advanced cooling systems.

Asia Pacific is the fastest-growing region, with a CAGR of 24.6%. Rapid digitalization, rising cloud adoption, and increasing AI workloads are driving demand across China, India, Singapore, and South Korea. Energy constraints and high rack densities are pushing operators toward liquid and hybrid cooling solutions.

Europe remains a key market, holding over 26% share, driven by strict environmental regulations and sustainability mandates. Countries such as Germany, the UK, and the Nordics are leading the adoption of free cooling, liquid cooling, and heat recovery systems, supported by favorable climate conditions and renewable energy availability.

Competitive Landscape

The market is moderately consolidated, with leading players accounting for 30–40% of global revenue. Key companies are focusing on mergers and acquisitions, R&D investments, and partnerships with semiconductor manufacturers to develop advanced cooling technologies. Competitive differentiation is increasingly based on integrated solution portfolios, AI-driven thermal management software, and sustainability performance.

New business models such as Cooling-as-a-Service (CaaS), modular prefabricated cooling pods, and predictive maintenance platforms are gaining traction. These models allow operators to reduce upfront costs while improving operational flexibility.

Recent innovations include high-capacity coolant distribution units designed for AI data centers and compact immersion cooling systems for edge environments, reflecting the industry’s shift toward scalability and efficiency.

Conclusion

The data center cooling market is entering a period of rapid evolution driven by AI expansion, sustainability mandates, and architectural shifts in computing infrastructure. As workloads become denser and energy demands intensify, traditional air-based systems are giving way to advanced liquid cooling and hybrid technologies. With strong growth projected through 2033, the market is positioned at the center of the global digital infrastructure transformation, where efficiency, scalability, and sustainability will define competitive advantage.

Related Reports:

- 4G (LTE) Devices Market

- Mobile Apps and Web Analytics Market

- Bluetooth Beacon and iBeacon Market

- Interactive and Self-Service Kiosk Market