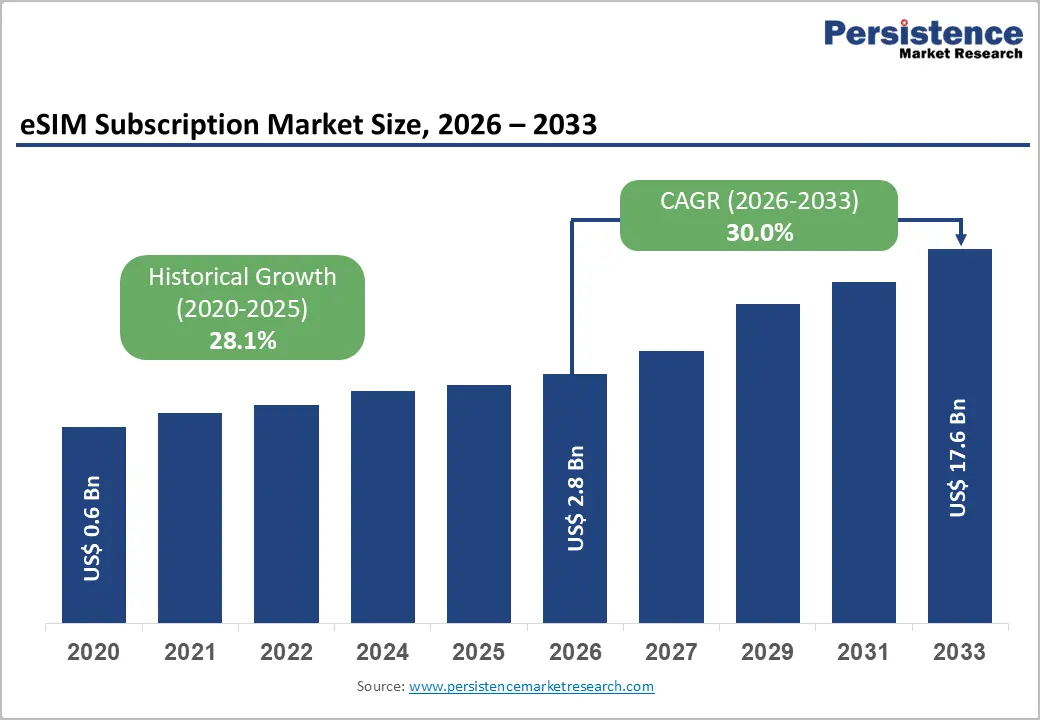

The global eSIM subscription market is entering a period of rapid structural transformation, driven by the shift away from physical SIM cards toward fully digital, remotely provisioned connectivity. Valued at US$ 2.8 billion in 2026, the market is projected to surge to US$ 17.6 billion by 2033, expanding at a strong CAGR of 30.0% during 2026–2033. This growth reflects accelerating adoption across smartphones, IoT ecosystems, and connected vehicles, alongside telecom operators’ increasing focus on flexible, software-defined connectivity services.

As digital infrastructure evolves, eSIM subscriptions are becoming a core enabler of next-generation communication models. The ability to activate, switch, and manage mobile networks without physical SIM cards is reshaping both consumer expectations and enterprise connectivity strategies.

Market Overview

eSIM (embedded SIM) technology eliminates the need for physical SIM cards by embedding a programmable SIM directly into devices. This enables remote provisioning of mobile network profiles, allowing users and enterprises to switch carriers, manage multiple numbers, and activate services instantly.

The subscription model built around eSIMs is expanding rapidly because it aligns with broader trends in digitalization, automation, and cloud-based connectivity management. Telecom operators are transitioning from traditional SIM distribution toward subscription-based digital services, improving operational efficiency and increasing customer lifetime value.

Between 2020 and 2025, the market recorded a strong historical CAGR of 28.1%, setting the foundation for even faster growth during the forecast period.

Key Market Highlights

- Market Size (2026): US$ 2.8 Billion

- Forecast Size (2033): US$ 17.6 Billion

- CAGR (2026–2033): 30.0%

- Leading Region: North America (38% share in 2025)

- Fastest Growing Region: Asia Pacific

- Leading Subscription Type: Voice + Data (45% share in 2025)

- Leading Application: Smartphones & Consumer Devices (55% share in 2025)

- Leading End-user: Consumer Segment (~50% share in 2025)

Market Dynamics

Drivers

- Expansion of IoT and 5G Connectivity

One of the strongest growth drivers is the rapid expansion of IoT and 5G-enabled devices. Global cellular IoT connections have already surpassed 4 billion units, and this number continues to grow as industries adopt smart sensors, connected machines, and real-time monitoring systems.

Industries such as logistics, manufacturing, energy, and utilities increasingly depend on scalable connectivity solutions. eSIM technology enables remote provisioning of SIM profiles, reducing the need for physical intervention and enabling global deployments of IoT devices at scale.

With LTE Cat 1 bis and 5G modules becoming mainstream, eSIM subscriptions are becoming a default connectivity solution for enterprise IoT ecosystems.

- Rising Adoption in Smartphones and Consumer Devices

The integration of eSIM in smartphones is significantly accelerating adoption. Leading OEMs are embedding eSIM functionality in flagship and mid-range devices, making digital connectivity accessible to a wider consumer base.

Consumers benefit from:

- Instant carrier activation

- Seamless international roaming

- Dual SIM functionality

- Easy switching between plans

As users become more mobile and digitally connected, demand for flexible subscription-based telecom services is increasing steadily.

Restraints

- Device Fragmentation and Limited Awareness

Despite strong growth, adoption is uneven across markets. While premium smartphones widely support eSIM, many mid-range and budget devices still rely on physical SIM cards. This creates a fragmented ecosystem that slows mass adoption, especially in price-sensitive regions.

Consumer awareness also remains a challenge. Many users are unfamiliar with activation processes, profile management, and carrier switching, leading to hesitation and increased support requirements for operators.

- Regulatory and Security Challenges

Telecom regulations vary significantly across countries, particularly around SIM registration, data localization, and cross-border connectivity. These differences complicate global rollout strategies for eSIM subscription providers.

Security concerns such as SIM swap fraud, unauthorized provisioning, and data breaches further require advanced encryption and compliance systems, increasing operational costs and limiting entry for smaller providers.

Opportunities

- Growth of Industrial IoT and M2M Connectivity

Industrial IoT represents one of the most promising opportunities for eSIM subscriptions. Sectors like manufacturing, logistics, agriculture, and smart utilities require always-on, scalable connectivity for thousands of devices.

eSIM enables:

- Factory-embedded connectivity

- Remote SIM management

- Multi-network switching

- Reduced maintenance costs

This makes it highly attractive for long-term enterprise subscription models based on recurring revenue.

- Connected Vehicles and Enterprise Mobility

The automotive sector is rapidly integrating eSIM technology for telematics, infotainment, and over-the-air software updates. Connected vehicles rely on continuous connectivity, making eSIM a natural fit for subscription-based models.

Similarly, enterprises are adopting eSIM-enabled devices for global workforce mobility, enabling employees to stay connected across regions without physical SIM swaps or roaming limitations.

Segment Analysis

Subscription Type

Voice + Data plans dominate the market, accounting for around 45% share in 2025. This dominance is driven by smartphone usage patterns, where consumers prefer bundled communication services.

However, IoT/M2M subscriptions are the fastest-growing segment, supported by rising demand for machine-to-machine connectivity in industrial applications.

Application

Smartphones and consumer devices hold the largest share (55%), reflecting strong OEM adoption and increasing availability of eSIM-enabled devices.

Meanwhile, industrial IoT applications are expanding rapidly, especially in sectors requiring real-time data collection and remote monitoring. These applications depend heavily on reliable and flexible connectivity, making eSIM a preferred solution.

End-user

The consumer segment accounts for nearly 50% of the market, driven by convenience, flexibility, and digital-first connectivity preferences.

The enterprise segment, however, is growing faster, supported by increasing adoption of IoT ecosystems, fleet management systems, and global workforce connectivity solutions.

Regional Analysis

North America

North America leads the global eSIM subscription market with 38% share in 2025, supported by advanced telecom infrastructure and early adoption of digital SIM technologies. The region benefits from strong 5G deployment and widespread availability of eSIM-enabled devices.

Enterprise adoption is also rising, particularly in logistics, healthcare, and smart infrastructure sectors.

Europe

Europe is a major growth region driven by strong regulatory frameworks and cross-border mobility needs. Countries such as Germany, France, and the U.K. are leading adoption.

The region is expected to grow at a CAGR of 28.3%, fueled by IoT expansion in smart cities, utilities, and transportation systems.

Asia Pacific

Asia Pacific is the fastest-growing region, holding around 27.3% share in 2025. Rapid smartphone adoption, strong manufacturing capabilities, and large-scale 5G deployment are key growth drivers.

China, India, and Japan are leading markets, supported by government-led digital transformation initiatives and smart city developments.

Competitive Landscape

The eSIM subscription market is moderately consolidated, with major telecom operators dominating global subscription revenues. Companies such as AT&T, Vodafone, Deutsche Telekom, Orange, and Telefónica leverage their infrastructure and subscriber bases to maintain strong market positions.

At the same time, digital-first players such as Airalo, Holafly, GigSky, and Nomad eSIM are reshaping the market by offering flexible, app-based eSIM solutions for travelers and remote users.

IoT connectivity providers like KORE Wireless are also gaining traction by targeting enterprise and industrial deployments.

Competition is increasingly defined by:

- Multi-network coverage

- API-driven connectivity platforms

- Cloud-based SIM management

- Flexible subscription pricing models

Recent Developments

- Apple (2025): Expanded eSIM-only activation for U.S. iPhones in partnership with Verizon, accelerating mainstream adoption.

- GSMA (2024): Updated eSIM IoT standards (SGP.32), improving remote provisioning and interoperability.

- Thales & IDEMIA (2025): Introduced quantum-resistant eSIM security modules for automotive and critical infrastructure use cases.

These developments highlight the growing maturity and security focus of the ecosystem.

Key Companies in the Market

Airalo, GigSky, Ubigi, Holafly, Nomad eSIM, Yesim, Truphone, Deutsche Telekom, Telefónica, Vodafone Group, AT&T, Orange S.A., KORE Wireless, BNESIM, Maya Mobile.

Conclusion

The global eSIM subscription market is undergoing a major structural shift, moving from traditional SIM-based connectivity to fully digital, software-driven subscription ecosystems. With a projected value of US$ 17.6 billion by 2033, the market is set to become a foundational layer of global mobile connectivity.

Strong growth in IoT, 5G networks, connected vehicles, and enterprise mobility will continue to drive demand, while innovation in remote provisioning, security, and multi-network access will shape the next phase of competition.

As telecom ecosystems evolve toward fully digital infrastructure, eSIM subscriptions are positioned not just as an upgrade, but as the future standard of global connectivity.

Related Reports: