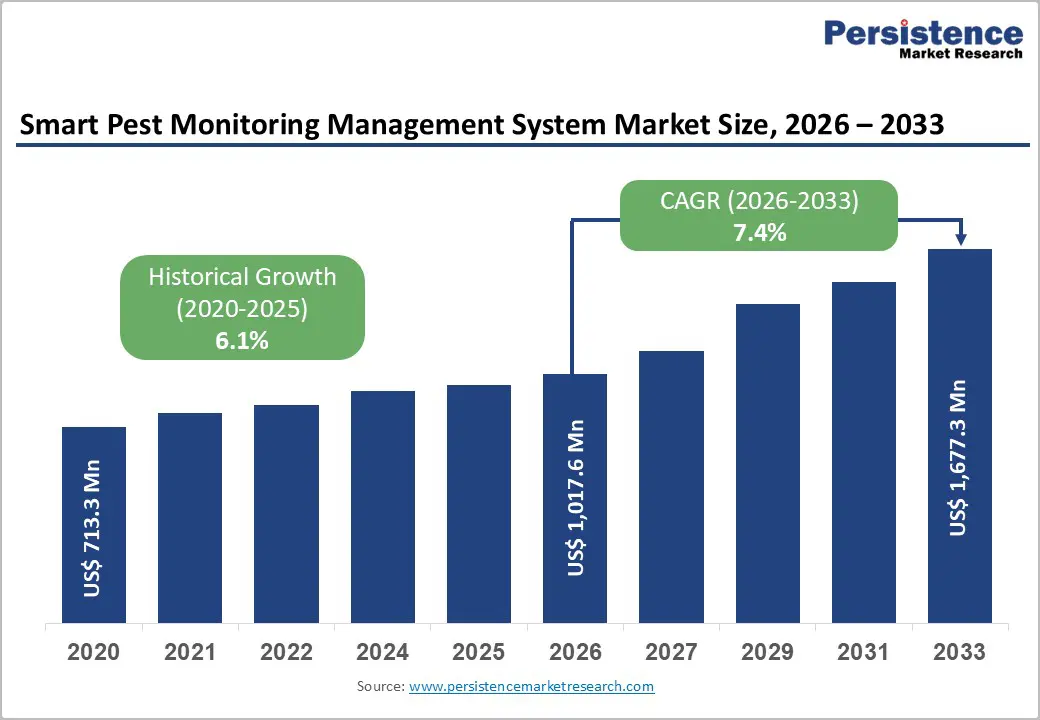

The global Smart Pest Monitoring Management System market is undergoing a significant transformation, driven by rapid advancements in IoT, artificial intelligence, and precision agriculture technologies. Valued at US$ 1,017.6 million in 2026, the market is projected to reach US$ 1,677.3 million by 2033, expanding at a CAGR of 7.4% during the forecast period. This growth reflects a broader shift toward data-driven agricultural practices and sustainable pest control strategies aimed at improving global food security while reducing environmental impact.

Rising crop losses due to pest infestations, combined with increasing regulatory pressure to reduce chemical pesticide usage, are accelerating adoption across agriculture, commercial facilities, industrial environments, and even residential applications. Smart pest monitoring systems are evolving from simple detection tools into integrated digital ecosystems that provide real-time analytics, predictive insights, and automated response capabilities.

Market Overview

Smart pest monitoring management systems combine IoT-enabled sensors, smart traps, imaging devices, wireless connectivity, and AI-based analytics platforms to detect, identify, and manage pest activity in real time. Unlike traditional pest control methods that rely on periodic inspections and reactive spraying, these systems enable continuous surveillance and early intervention.

The increasing integration of cloud computing, edge analytics, and machine learning is enabling predictive pest management models that significantly reduce response time and operational costs. As agriculture becomes more technology-intensive, pest management is emerging as a core component of precision farming ecosystems.

Between 2020 and 2025, the market grew steadily at around 6.1% CAGR, and this growth trajectory is expected to accelerate further due to regulatory reforms, climate variability, and the rising need for sustainable agricultural productivity.

Key Industry Highlights

- Market Size (2026): US$ 1,017.6 million

- Market Forecast (2033): US$ 1,677.3 million

- CAGR (2026–2033): 7.4%

- Leading Region: North America (~35% share in 2025)

- Fastest Growing Region: Asia Pacific (~25% share in 2025)

- Leading Application: Agriculture (~55% share in 2025)

- Dominant Component: Hardware (~45% share in 2025)

- Leading Pest Type: Insects (~52% share in 2025)

A key opportunity lies in the integration of pest monitoring systems with smart farming platforms, autonomous machinery, and digital agriculture ecosystems, enabling end-to-end farm intelligence.

Market Dynamics

Drivers

- IoT and AI-Driven Transformation

The integration of IoT sensors, smart traps, and AI-based analytics is revolutionizing pest management. Real-time monitoring enables farmers and facility operators to identify pest activity early, reducing crop damage and improving operational efficiency.

AI-powered image recognition and predictive modeling allow systems to detect pest behavior patterns and forecast outbreaks before they occur. Combined with 5G and LPWAN connectivity, these systems can operate across large agricultural landscapes with minimal latency.

- Rise of Precision Agriculture

Precision agriculture is a major growth catalyst for the market. Smart pest monitoring systems provide granular field-level insights that help optimize pesticide usage, reduce costs, and improve yield quality. This aligns with global sustainability goals and reduces the environmental footprint of farming.

- Regulatory Pressure on Pesticide Usage

Governments worldwide are enforcing stricter regulations on pesticide use due to environmental and health concerns. Integrated Pest Management (IPM) frameworks are being widely promoted, increasing demand for real-time monitoring solutions that reduce reliance on chemical spraying.

Restraints

- High Initial Investment

The adoption of smart pest monitoring systems is often hindered by high upfront costs associated with sensors, software platforms, and infrastructure deployment. Small and medium-scale farmers, especially in developing economies, face significant financial barriers.

- Infrastructure Limitations

In many rural and developing regions, limited internet connectivity and unstable power supply restrict system efficiency. Without reliable connectivity, real-time data transmission becomes inconsistent, reducing system effectiveness.

- Limited Technical Expertise

A lack of digital literacy among end users also restricts adoption. Many farmers struggle to interpret AI-driven insights or manage cloud-based dashboards, leading to underutilization of advanced features.

Opportunities

Integration with Precision Agriculture Platforms

The convergence of pest monitoring systems with broader agritech ecosystems presents a strong growth opportunity. Integration with soil sensors, weather forecasting systems, and crop health analytics enables holistic farm management.

This ecosystem approach allows automated decision-making, such as triggering targeted pesticide application or activating robotic sprayers based on real-time pest detection.

Expansion in Emerging Markets

Emerging economies in Asia, Latin America, and Africa present significant opportunities due to large agricultural bases and increasing government support for digital farming initiatives. Affordable, solar-powered, and low-maintenance systems are particularly suited for these regions.

Category-wise Analysis

Component Insights

Hardware dominates the market with approximately 45% share in 2025, driven by demand for durable sensors, traps, cameras, and field devices. These components form the backbone of pest monitoring systems, enabling real-time data collection in diverse environmental conditions.

Meanwhile, the software segment is the fastest-growing category. Cloud platforms, AI analytics tools, and mobile dashboards are becoming essential for converting raw data into actionable insights. This shift highlights the transition from hardware-centric solutions to integrated digital ecosystems.

Pest Type Insights

Insects remain the largest pest category, accounting for around 52% of market share in 2025. They significantly impact crop productivity and are difficult to control without early detection systems.

Rodents represent the fastest-growing segment due to increasing concerns in food storage facilities, warehouses, and urban infrastructure. Smart rodent detection systems with real-time alerts are gaining traction in commercial and industrial sectors.

Application Insights

Agriculture is the dominant application segment, holding approximately 55% market share in 2025. The high economic impact of pest damage in crops makes smart monitoring essential for modern farming practices.

The commercial sector is growing rapidly, driven by demand from restaurants, supermarkets, food processing units, and hospitality businesses. These environments require continuous monitoring to ensure hygiene compliance and prevent contamination risks.

Regional Analysis

North America

North America leads the global market with approximately 35% share in 2025. The United States plays a central role due to advanced agricultural technologies, strong regulatory frameworks, and widespread adoption of precision farming.

High investment in AI-based pest detection systems and strong collaboration between agritech companies and research institutions further support regional growth.

Europe

Europe is a highly regulated market, emphasizing sustainable agriculture and reduced pesticide usage. The region is expected to grow at a CAGR of around 7.8%, driven by organic farming initiatives and strict food safety standards.

Countries such as France, Germany, and Spain are key contributors, particularly in high-value crops like vineyards, fruits, and vegetables.

Asia Pacific

Asia Pacific is the fastest-growing region, accounting for approximately 25% share in 2025. Countries like India and China are rapidly adopting smart agriculture technologies to address food security challenges and reduce crop losses.

Government-backed digital agriculture initiatives and affordable IoT solutions are accelerating adoption across small and medium farms.

Competitive Landscape

The market is moderately consolidated, with a mix of global agritech leaders and specialized pest control companies. Competition is driven by innovation in AI analytics, sensor technology, and cloud integration.

Companies are increasingly adopting subscription-based models and hardware-as-a-service offerings, making solutions more affordable and scalable. Edge computing and offline-capable systems are also gaining importance in rural deployments.

Key Developments

- March 2025: Fovea launched an AI-powered insect trap integrated with drone scouting in Europe, reducing pest response times by 50%.

- July 2024: Trapview expanded its solar-powered monitoring network in India, targeting rice and cotton crops under government digital farming programs.

- November 2023: Semios introduced a predictive analytics platform integrating pest, weather, and crop data for orchards in North America.

Key Companies Covered

Bayer AG, Anticimex, Corteva Agriscience, BASF SE, Ecolab Inc., Syngenta AG, Bell Laboratories, Pelsis Group Ltd, Rentokil Initial plc, FMC Corporation, Rollins, Inc., SemiosBio Technologies, FaunaPhotonics, DunavNET, and Spensa Technologies.

Conclusion

The Smart Pest Monitoring Management System market is transitioning from a niche agricultural technology segment into a core pillar of global precision farming and sustainable pest control strategies. With increasing pressure to enhance food production efficiency while minimizing environmental harm, demand for intelligent, data-driven pest management solutions is expected to rise steadily.

Between 2026 and 2033, growth will be fueled by AI-driven analytics, IoT expansion, regulatory reforms, and increasing adoption in emerging economies. Despite challenges such as high costs and infrastructure gaps, the long-term outlook remains strong, positioning smart pest monitoring systems as a critical component of future agricultural and environmental management ecosystems.