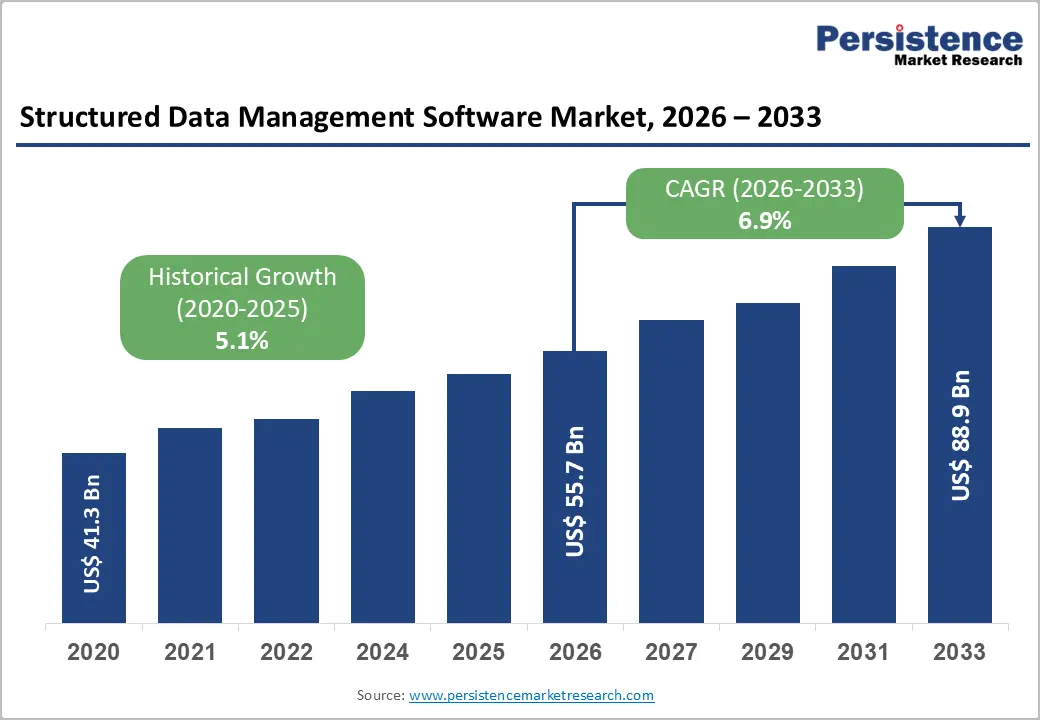

The global structured data management software market is entering a strong growth phase, driven by the accelerating digitization of enterprises, explosive growth in structured and semi-structured data volumes, and the increasing need for scalable, secure, and compliant data governance systems. Valued at US$55.7 billion in 2026, the market is projected to reach US$88.9 billion by 2033, expanding at a CAGR of 6.9% during the forecast period.

Organizations across industries are rapidly shifting from fragmented legacy databases to unified, cloud-native data platforms that support real-time analytics, artificial intelligence (AI) workloads, and regulatory compliance. This transformation is reshaping how enterprises store, process, and derive insights from structured data, positioning data management software as a foundational layer of digital business infrastructure.

Market Overview

Structured data management software refers to platforms and tools designed to store, organize, integrate, govern, and analyze structured datasets—typically organized in relational formats such as tables, rows, and columns. These systems include relational database management systems (RDBMS), cloud data warehouses, master data management tools, and data integration platforms.

The market’s expansion is strongly linked to enterprise digital transformation strategies. Businesses today operate in data-intensive environments where structured data flows continuously from applications such as ERP systems, CRM platforms, financial systems, IoT dashboards, and transactional applications. Managing this data efficiently is critical for operational intelligence, regulatory compliance, and strategic decision-making.

The increasing adoption of hybrid and multi-cloud environments has further accelerated demand for scalable structured data platforms that can operate seamlessly across distributed infrastructures.

Key Market Highlights

- Market Size (2026): US$55.7 Billion

- Forecast Value (2033): US$88.9 Billion

- CAGR (2026–2033): 6.9%

- Historical Growth (2020–2025): 5.1%

- Leading Region: North America (38% share)

- Fastest Growing Region: Asia Pacific (CAGR 8.7%)

- Leading Deployment Model: Cloud-based (52% share)

- Dominant End-use Industry: BFSI

Market Drivers

- Rapid Cloud Adoption and Data Modernization

One of the most powerful growth drivers is the global shift toward cloud computing. Enterprises are actively modernizing legacy data systems to cloud-native architectures to improve scalability, performance, and cost efficiency.

According to industry studies, nearly 90% of enterprises now follow multi-cloud strategies, reinforcing the need for unified structured data management platforms that can operate across AWS, Azure, and Google Cloud ecosystems.

Cloud-based structured data platforms such as Amazon Redshift, Google BigQuery, and Microsoft Azure Synapse Analytics are becoming central to enterprise data strategies, enabling real-time analytics and reducing infrastructure overhead.

- Rising Data Governance and Regulatory Compliance Requirements

Global regulatory frameworks are becoming increasingly strict, pushing enterprises to adopt structured data governance solutions. Regulations such as GDPR, CCPA, Basel IV, IFRS 9, and DORA require organizations to maintain full data traceability, auditability, and transparency.

With more than 160 data protection laws active globally, enterprises are investing heavily in platforms that provide:

- Data lineage tracking

- Automated compliance reporting

- Real-time monitoring

- Secure access control

Structured data management software has therefore become essential for risk mitigation and legal compliance.

- Explosion of Enterprise Data Volumes

Modern enterprises generate massive structured datasets from digital transactions, customer interactions, financial operations, and IoT systems. This exponential data growth is overwhelming traditional database systems.

Structured data management platforms help organizations:

- Organize large-scale datasets efficiently

- Enable faster query processing

- Improve decision-making accuracy

- Support high-speed analytics applications

Market Restraints

- High Implementation Complexity and Cost Barriers

Despite strong demand, implementation complexity remains a key challenge. Large-scale deployments often require significant investment in:

- Software licensing

- System integration

- Cloud migration

- Workforce training

For many small and medium enterprises (SMEs), the cost and complexity of adoption remain prohibitive, slowing market penetration in this segment.

- Data Security and Cloud Risk Concerns

Security remains a major concern, especially for industries handling sensitive data such as BFSI, healthcare, and government sectors.

According to global cybersecurity studies, the average cost of a data breach exceeds US$4 million, making organizations cautious about cloud adoption. Risks such as:

- Misconfigured cloud environments

- Credential theft

- Data sovereignty issues

continue to slow full-scale adoption of cloud-based structured data platforms.

Market Opportunities

- AI and Machine Learning Integration

The integration of AI and ML into structured data management platforms is transforming the market landscape. AI-enabled features include:

- Automated data cleansing

- Intelligent schema mapping

- Predictive governance

- Natural language querying

The World Economic Forum estimates AI could contribute US$15.7 trillion to the global economy by 2030, and structured data platforms are central to this transformation.

Vendors embedding generative AI capabilities are expected to gain a strong competitive advantage through improved automation and user experience.

- Rising Demand from BFSI Sector

The BFSI sector is emerging as both the largest and fastest-growing end-user segment. Financial institutions require high-performance data systems for:

- Fraud detection

- Risk modeling

- Algorithmic trading

- Regulatory reporting

With global digital payments projected to surpass US$14 trillion by 2027, structured data management systems are critical for handling high-frequency financial transactions and compliance requirements.

Segment Analysis

Deployment Model

Cloud-based deployment dominates the market with approximately 52% share, driven by scalability, cost efficiency, and flexibility. Organizations increasingly prefer cloud-first strategies, enabling seamless integration with analytics tools and AI applications.

On-premise deployments continue to exist in highly regulated industries, but their share is gradually declining.

Component

The software segment accounts for around 68% of total revenue, including:

- Relational database systems

- Data integration tools

- Data warehousing platforms

- Master data management systems

Services such as consulting and managed support are also growing, particularly in large enterprise deployments.

Organization Size

Large enterprises dominate the market with 61% revenue share, due to their:

- Complex IT environments

- High data volumes

- Strong regulatory obligations

- Greater investment capacity

SMEs are increasingly adopting cloud-based solutions but still represent a smaller share of total revenue.

Application

Financial analytics leads the application segment with 22% share, driven by demand for:

- Real-time risk analysis

- Fraud detection systems

- Financial reporting

- Portfolio optimization

End-use Industry

The BFSI sector holds the largest share at 24%, reflecting its heavy reliance on structured data for operations, compliance, and customer analytics.

Regional Analysis

North America

North America leads the global market with 38% share, supported by:

- Strong presence of technology giants (IBM, Microsoft, Oracle, Snowflake)

- Advanced cloud infrastructure

- High enterprise IT spending

- Strong regulatory frameworks

The United States remains the dominant contributor, with widespread adoption of advanced data management technologies.

Europe

Europe is the second-largest market, driven by strict data governance regulations such as GDPR. Countries like Germany and the UK are leading adoption, particularly in industrial and financial sectors.

The region emphasizes:

- Data transparency

- Compliance-driven analytics

- Secure cloud adoption

Asia Pacific

Asia Pacific is the fastest-growing region with a CAGR of 8.7%, driven by:

- Rapid digital transformation in China and India

- Government-led digital economy initiatives

- Expanding cloud ecosystems

- Increasing enterprise data generation

This region is expected to become a major growth engine for the global market.

Competitive Landscape

The structured data management software market is moderately consolidated, with major global players dominating enterprise deployments. Key companies focus on innovation, cloud integration, and AI-driven capabilities.

Leading players include:

IBM Corporation, Oracle Corporation, Microsoft, SAP SE, AWS, Google Cloud, Snowflake, Informatica, Teradata, Cloudera, Databricks, SAS Institute, and others.

Key Industry Trends:

- Shift toward cloud-native platforms

- Expansion of AI-driven data management tools

- Growth in subscription-based pricing models

- Strategic acquisitions and partnerships

Recent innovations, such as Snowflake’s AI integrations and Microsoft Fabric enhancements, highlight the strong convergence of data management and artificial intelligence.

Recent Developments

- February 2025: Snowflake integrated its Arctic AI model into its structured data platform for native AI workloads.

- October 2024: IBM launched an upgraded Db2 platform with AI-assisted query optimization.

- March 2024: Microsoft expanded Microsoft Fabric with Copilot-enabled structured data tools.

Conclusion

The structured data management software market is undergoing a fundamental transformation driven by cloud adoption, AI integration, and rising regulatory pressures. As enterprises continue to modernize their data infrastructure, structured data platforms are becoming essential for operational efficiency, compliance, and advanced analytics.

With strong growth expected through 2033, the market is positioned as a critical pillar of the global digital economy. Vendors that successfully combine cloud scalability, AI intelligence, and robust governance capabilities are likely to lead the next wave of industry innovation.