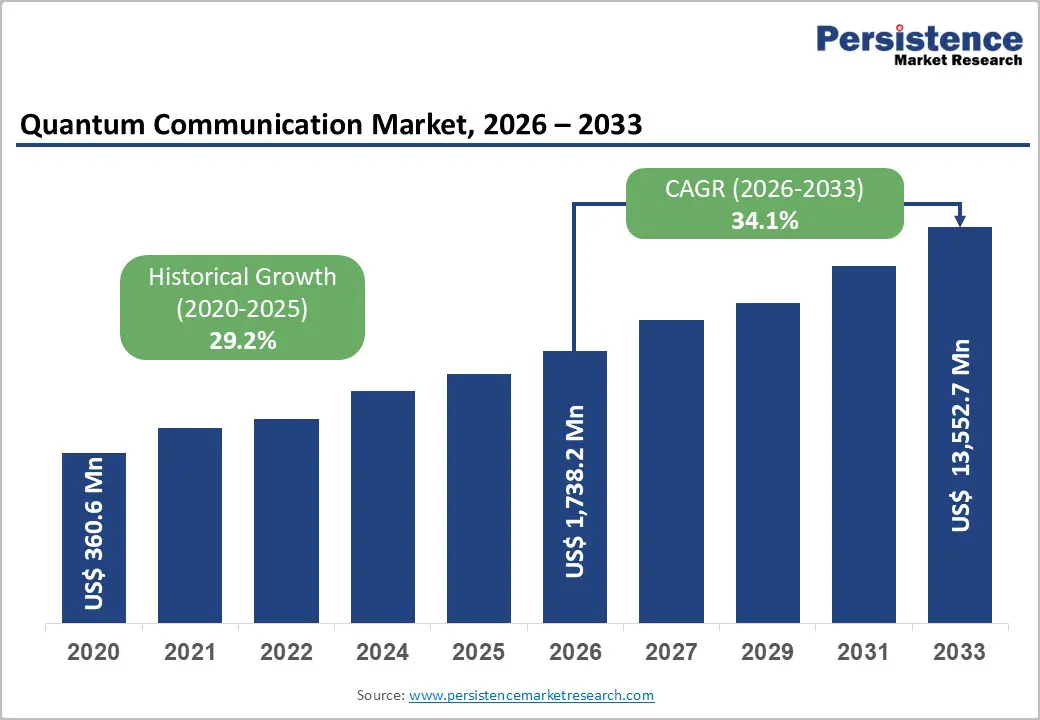

The global Quantum Communication Market is entering a transformative growth phase as governments, defense agencies, and enterprises prepare for a post-quantum cybersecurity landscape. Valued at US$ 1,738.2 million in 2026, the market is projected to surge dramatically to US$ 13,552.7 million by 2033, expanding at a remarkable CAGR of 34.1% during the forecast period. This exponential growth reflects rising urgency around next-generation cyber threats, particularly the “Harvest Now, Decrypt Later (HNDL)” risk, where adversaries store encrypted data today with the intent of decrypting it in the future using fault-tolerant quantum computers.

As quantum computing advances toward practical scalability, traditional encryption methods face long-term vulnerability. This has triggered a global shift toward quantum-secure communication systems, especially Quantum Key Distribution (QKD) and satellite-based quantum networks. The result is a rapidly expanding ecosystem supported by heavy public funding, defense procurement programs, and private-sector innovation.

Market Overview and Structural Evolution

Quantum communication represents a paradigm shift in secure data transmission, leveraging the principles of quantum mechanics—particularly quantum entanglement and photon behavior—to enable theoretically unbreakable encryption. Unlike classical encryption methods, which rely on computational complexity, quantum communication ensures security rooted in physical laws.

The market’s evolution is being shaped by three major structural forces: accelerating cyber risk, long cryptographic migration timelines, and increasing geopolitical competition in quantum technologies. Enterprises are no longer viewing quantum security as optional; instead, it is becoming a strategic necessity embedded into national security and digital infrastructure planning.

Government mandates such as the U.S. National Quantum Initiative Act and NIST’s post-quantum cryptography standards finalized in 2024 have further institutionalized this transition. Similar frameworks in Canada, the European Union, and Asia are reinforcing global alignment toward quantum-safe communication systems.

Key Industry Highlights

Several segments are emerging as dominant contributors to market growth:

Leading Offering – Hardware Dominance (56%+ share in 2026):

The hardware segment is expected to surpass US$ 973.4 million in 2026, driven by demand for ultra-precise photon sources, quantum detectors, and noise-resistant transmission systems. These components are essential for maintaining signal integrity in quantum communication networks.

Leading Technology – Quantum Key Distribution (60%+ share):

QKD is projected to generate over US$ 1,042.9 million in 2026, making it the most widely adopted quantum communication technology. Its ability to detect interception attempts and ensure near-unbreakable encryption positions it as the backbone of secure communication frameworks.

Leading End-user – Government & Defense (25%+ share):

Valued at US$ 434.6 million in 2026, government and defense agencies remain the largest adopters due to the critical need for secure military communications, intelligence sharing, and protection of national infrastructure.

Leading Region – North America (37%+ share):

North America is projected to hold US$ 643.1 million in 2026, supported by advanced R&D ecosystems, strong federal funding, and early adoption by defense and financial institutions.

Market Dynamics

Drivers

- Rise of Satellite-Based Quantum Communication Networks

A major growth driver is the development of satellite-enabled quantum communication systems, which overcome the distance limitations of fiber-based networks. Traditional fiber optics suffer from photon loss over long distances, restricting secure communication to metropolitan-scale networks. Satellite systems eliminate this barrier, enabling secure global communication.

China’s Micius satellite and Europe’s Quantum Internet Alliance demonstrate early breakthroughs in this domain. With global investments exceeding US$ 2 billion, satellite-based quantum networks are becoming a cornerstone of future secure communication infrastructure for governments and defense organizations.

- Regulatory Push from Post-Quantum Cryptography Standards

The finalization of NIST’s post-quantum cryptography standards—including ML-KEM, ML-DSA, and SLH-DSA—has accelerated enterprise adoption. Governments now require cryptographic inventory assessments and migration planning, with strict deadlines extending into the 2030s.

These regulations are transforming quantum communication from a research-driven field into a procurement-driven industry. Enterprises in banking, defense, and critical infrastructure are being compelled to upgrade systems, creating sustained demand for QKD hardware and services.

Restraints

High Hardware Costs and Infrastructure Limitations

Quantum communication systems remain expensive due to specialized manufacturing requirements for single-photon sources, detectors, and precision optical components. Additionally, fiber-based QKD networks are constrained by distance limitations, typically under 200 km without repeaters.

Although technological milestones—such as Toshiba’s extended-range QKD demonstrations—are pushing boundaries, scalable nationwide deployments still require significant infrastructure investment.

Talent Shortage and Integration Complexity

The market also faces a shortage of quantum physicists, photonics engineers, and network integration specialists. Deploying quantum systems requires seamless integration with existing IT infrastructure such as SIEM, zero-trust architectures, and enterprise encryption frameworks.

The complexity of migrating legacy cryptographic systems across large enterprises adds further cost and time barriers, slowing down widespread adoption.

Opportunities

Quantum-as-a-Service (QaaS) Models

One of the most promising opportunities is the emergence of cloud-based Quantum-as-a-Service platforms. These models allow enterprises to access quantum-secured communication without investing in expensive infrastructure.

QaaS significantly lowers adoption barriers, especially for healthcare, BFSI, and research institutions. It also enables recurring revenue models for vendors and fosters broader commercialization of quantum technologies.

Telecom-Led Quantum Network Expansion

Telecom operators are increasingly integrating QKD into existing fiber networks to offer secure communication services. Partnerships between telecom providers and quantum technology firms are enabling pilot projects and early commercial deployments.

These collaborations are expected to accelerate mainstream adoption while creating a multi-layered ecosystem involving hardware vendors, software providers, and managed service operators.

Category-wise Analysis

Offering Insights

Hardware continues to dominate due to its foundational role in quantum communication infrastructure. Quantum detectors alone account for approximately 24% of hardware demand, highlighting their importance in maintaining signal integrity.

Services, however, are expected to grow rapidly as organizations seek consulting, integration, and managed quantum security solutions. This shift reflects increasing reliance on external expertise for deployment and maintenance.

Technology Insights

Quantum Key Distribution (QKD):

QKD remains the dominant technology due to its ability to detect eavesdropping and ensure secure key exchange. Financial institutions and government agencies prioritize QKD for compliance and cybersecurity resilience.

Quantum Teleportation:

Although still in early-stage research, quantum teleportation is gaining attention for its potential to enable instant, high-fidelity quantum communication across distant nodes. Long-term applications include distributed quantum computing and ultra-secure global networks.

End-user Insights

Government and defense sectors dominate adoption, driven by national security requirements and increasing cyber warfare risks. Meanwhile, the BFSI sector is expected to grow at a rapid 38.4% CAGR, fueled by the need for secure digital banking, fraud prevention, and regulatory compliance.

Other emerging adopters include healthcare organizations, cloud service providers, and research institutions, all of which require high-security communication frameworks.

Regional Analysis

North America

North America leads the global market due to strong federal investment, advanced quantum research institutions, and active private-sector participation. The U.S. is particularly focused on integrating quantum communication into defense and financial systems.

Asia Pacific

Asia Pacific is the fastest-growing region with a projected CAGR of 39.8%. China leads in satellite-based quantum communication infrastructure, while Japan and India are making significant investments in national quantum programs.

Europe

Europe holds over 24% market share, driven by the EU Quantum Flagship Program. Countries such as Germany, France, and the U.K. are advancing photonics research and cross-border quantum networks with strong regulatory alignment.

Competitive Landscape

The market remains moderately consolidated, with key players focusing heavily on R&D and global expansion. Strategic initiatives include the development of QKD systems, quantum satellites, and integrated encryption platforms.

Emerging trends include quantum-as-a-service models and hybrid encryption systems combining classical and quantum security protocols.

Recent Key Developments

In 2026, India’s National Quantum Mission successfully demonstrated a 1,000 km quantum-secure communication network, marking a significant milestone in indigenous quantum capability development.

Additionally, Quantum Computing Inc. and Ciena demonstrated a hybrid system combining QKD, post-quantum cryptography, and optical encryption capable of achieving high-speed secure transmission up to 1.6 Tb/s.

Key Companies

Major players shaping the quantum communication landscape include:

ID Quantique, QuantumCTek, Toshiba Corporation, QNu Labs, QuintessenceLabs, MagiQ Technologies, KETS Quantum Security, Qubitekk, SpeQtral, Quantropi, IonQ, and Quantum Computing Inc., among others.

Conclusion

The quantum communication market is transitioning from experimental research to large-scale industrial deployment. Driven by escalating cybersecurity threats, regulatory mandates, and technological breakthroughs, the industry is poised for exponential expansion through 2033.

While challenges such as high costs and infrastructure limitations persist, innovations in satellite networks, QKD systems, and Quantum-as-a-Service models are steadily overcoming these barriers. As a result, quantum communication is expected to become a foundational layer of global cybersecurity architecture in the coming decade.