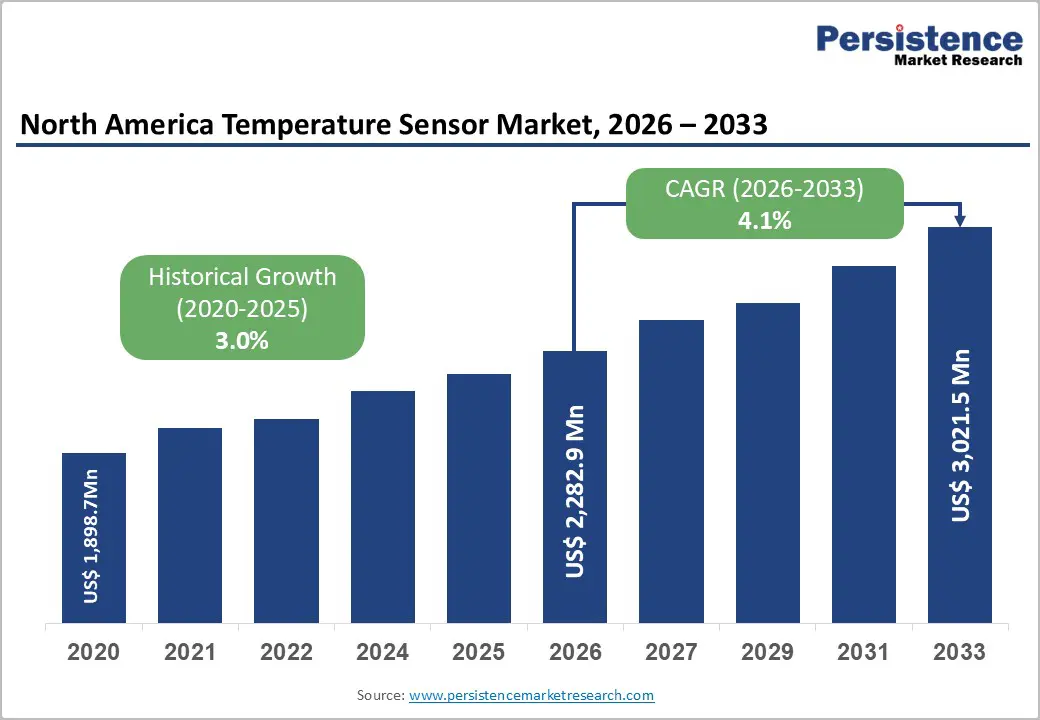

The North America temperature sensor market is entering a steady but strategically important growth phase, driven by the increasing need for precision monitoring, automation, and energy-efficient system control across industries. The market size is projected to rise from US$ 2,282.9 million in 2026 to US$ 3,021.5 million by 2033, reflecting a CAGR of 4.1% during the forecast period.

Although the growth rate may appear moderate compared to high-tech semiconductor markets, temperature sensors play a foundational role in modern industrial ecosystems. They are embedded across automotive systems, industrial machinery, healthcare devices, data centers, and consumer electronics—making them an essential enabling technology for digital transformation in North America.

Market Overview

Temperature sensing technologies are evolving from simple measurement tools into integrated intelligence components within connected systems. Modern industries increasingly rely on real-time thermal data to ensure safety, improve efficiency, and reduce operational downtime.

In North America, the market benefits from a highly developed industrial base, rapid electrification of transportation, and strong adoption of Industry 4.0 technologies. The region’s focus on predictive maintenance, automation, and energy optimization is accelerating demand for advanced sensor solutions with higher accuracy, lower power consumption, and seamless connectivity.

At the same time, the shift toward smart infrastructure—including AI-driven data centers, smart healthcare systems, and EV thermal management platforms—is expanding the scope of temperature sensors beyond traditional applications.

Key Market Highlights

- Market Size (2026E): US$ 2,282.9 Mn

- Market Forecast (2033F): US$ 3,021.5 Mn

- CAGR (2026–2033): 4.1%

- Historical CAGR (2020–2025): 3.0%

Leading Segments (2026)

- Product Type: Thermocouples (30%+ share, US$ 684.9 Mn)

- Connectivity: Wired systems (72%+ share, US$ 1,643.7 Mn)

- Industry: Automotive (28%+ share, US$ 639.2 Mn)

- Country: United States (75%+ share)

Market Dynamics

Drivers

- Rising Adoption of Predictive Maintenance and Industrial IoT

One of the strongest growth drivers for the North America temperature sensor market is the widespread adoption of predictive maintenance strategies. Enterprises are increasingly replacing reactive maintenance models with data-driven monitoring systems that use real-time sensor inputs to detect early signs of equipment failure.

Temperature sensors play a critical role in Industrial IoT (IIoT) ecosystems by continuously monitoring machine health, detecting overheating, and enabling early fault detection. According to the National Institute of Standards and Technology (NIST), IIoT-enabled systems significantly improve operational efficiency in manufacturing and utilities.

Manufacturers are increasingly embedding temperature sensors with wireless communication and analytics capabilities, allowing integration into cloud-based monitoring platforms. This shift is helping industries reduce downtime, optimize asset utilization, and extend equipment lifespan.

- Electrification of Vehicles and Expanding Thermal Management Needs

The rapid transition toward electric vehicles (EVs) is another major growth catalyst. EV systems require precise thermal management to ensure battery safety, performance efficiency, and long-term durability.

Modern battery management systems (BMS) use multiple temperature sensors to monitor individual cells and prevent thermal runaway. In fact, sensor density in vehicles has increased significantly—from just a few sensors in traditional vehicles to more than 15–20 in modern EVs.

North American automakers are heavily investing in EV development, and thermal monitoring has become a core design requirement in battery packs, power electronics, and motor control systems. This structural shift ensures sustained demand for high-performance temperature sensing solutions.

Restraints

- Raw Material Price Volatility and Supply Chain Disruptions

Temperature sensor manufacturing depends on critical materials such as platinum (used in RTDs), rare-earth elements, and semiconductor substrates. These materials are subject to price volatility driven by geopolitical tensions, supply chain constraints, and fluctuating global demand.

For manufacturers, especially smaller players, these cost fluctuations compress margins and create pricing instability. The lack of vertical integration further increases vulnerability to raw material disruptions.

- High Implementation Costs and Calibration Complexity

Advanced temperature sensing systems used in aerospace, industrial automation, and precision manufacturing often require significant upfront investment. Costs include not only hardware but also installation, calibration, and integration with legacy systems.

Precision sensors such as RTDs and fiber optic systems require specialized maintenance to ensure accuracy over time. This increases operational costs, particularly for small and medium enterprises, limiting adoption in price-sensitive sectors.

Opportunities

- Expansion of Smart Healthcare and Wearable Devices

Healthcare is emerging as a high-growth application area for temperature sensors. Wearable devices such as smart thermometers, patient monitoring patches, and remote diagnostic tools are increasingly used in hospitals and home care settings.

The post-pandemic rise in remote patient monitoring has accelerated adoption, with temperature sensors playing a central role in early illness detection and continuous health tracking. Compact IC-based sensors and thermistors are widely used due to their accuracy and small form factor.

The integration of AI-based health analytics and wireless connectivity is further enhancing real-time diagnostics and enabling personalized healthcare solutions.

- Growth of Data Centers and High-Performance Computing

The expansion of cloud computing, AI workloads, and high-performance computing is significantly increasing demand for advanced thermal monitoring systems.

Data centers generate substantial heat, and inefficient cooling can lead to performance degradation or system failure. Temperature sensors are used extensively in server racks, cooling systems, and liquid cooling infrastructures.

Major cloud providers such as AWS, Microsoft Azure, and Google Cloud are investing heavily in advanced cooling technologies, including immersion and liquid cooling systems. This trend is creating strong opportunities for infrared and fiber optic temperature sensing solutions.

Segment Analysis

By Product Type

Thermocouples

Thermocouples dominate the North America temperature sensor market with over 30% share in 2026. Their popularity stems from durability, wide temperature range, and cost-effectiveness. They are widely used in extreme industrial environments such as oil & gas, power generation, and heavy manufacturing.

Their ability to withstand harsh operating conditions makes them ideal for continuous process monitoring, especially where reliability is critical.

IC-Based Sensors

IC-based temperature sensors are expected to grow rapidly due to their compact size, low power consumption, and high accuracy. These sensors are widely used in consumer electronics, IoT devices, and smart systems where miniaturization is essential.

By Connectivity

Wired Sensors

Wired connectivity dominates the market with over 72% share in 2026. Industries continue to rely on wired systems due to their stability, low latency, and resistance to interference.

Critical applications such as industrial automation and process control require uninterrupted and highly reliable data transmission, supporting continued dominance of wired systems.

Wireless Sensors

Wireless temperature sensors are gaining strong momentum due to increasing demand for flexible and scalable monitoring systems. They eliminate complex wiring requirements and are ideal for remote or difficult-to-access environments.

The expansion of IoT ecosystems and cloud-based monitoring platforms is expected to significantly boost wireless adoption.

By Industry

Automotive

The automotive sector is the largest end-user, accounting for over 28% share in 2026. Temperature sensors are widely used in engine control units, EV battery systems, and emission control technologies.

The rise of electric vehicles has significantly increased thermal monitoring requirements, making temperature sensing a critical component of automotive safety and performance systems.

Consumer Electronics

Consumer electronics is one of the fastest-growing segments, expected to grow at a CAGR of 8.2%. Temperature sensors are widely used in smartphones, laptops, wearables, and smart home devices to prevent overheating and improve performance efficiency.

Country Analysis

United States

The United States dominates the North America temperature sensor market with over 75% share. Growth is driven by strong semiconductor manufacturing, expansion of AI-driven data centers, and regulatory requirements for industrial safety and energy efficiency.

The CHIPS and Science Act is also accelerating domestic semiconductor production, increasing demand for high-precision thermal monitoring systems in fabrication facilities.

Canada

Canada’s market is growing steadily, supported by strong demand for HVAC systems, EV adoption in cold climates, and cold-chain logistics infrastructure. Temperature sensors are widely used in building automation systems, healthcare storage, and industrial monitoring applications.

Competitive Landscape

The North America temperature sensor market is moderately fragmented, with leading companies accounting for around 20–30% of total share. Key players focus on innovation in MEMS-based sensors, wireless integration, and IoT-enabled solutions.

Major competitive strategies include acquisitions, R&D investments, and partnerships with automotive and industrial automation firms.

Key Developments

- In April 2025, Wilcoxon launched a digital triaxial accelerometer integrated with a temperature sensor for predictive maintenance applications.

- In January 2025, Thermo Electric – Cotemp Sensing developed a 300mm thermocouple wafer with 65 measurement points for semiconductor thermal mapping.

Key Companies

Honeywell International Inc., Texas Instruments Incorporated, Analog Devices Inc., Emerson Electric Co., Amphenol Corporation, Microchip Technology Inc., Watlow Electric Manufacturing Company, Omega Engineering Inc., Teledyne Technologies Incorporated, Fluke Corporation, Thermo Sensors Corporation, TE Connectivity Ltd., AMETEK Inc., and others.

Conclusion

The North America temperature sensor market is positioned for stable and technology-driven growth through 2033. While traditional industrial applications continue to anchor demand, the next wave of expansion is being shaped by EV adoption, AI-driven data centers, healthcare digitization, and industrial IoT integration.

As industries prioritize efficiency, safety, and predictive intelligence, temperature sensors will remain a foundational component of connected systems across North America’s evolving technological landscape.