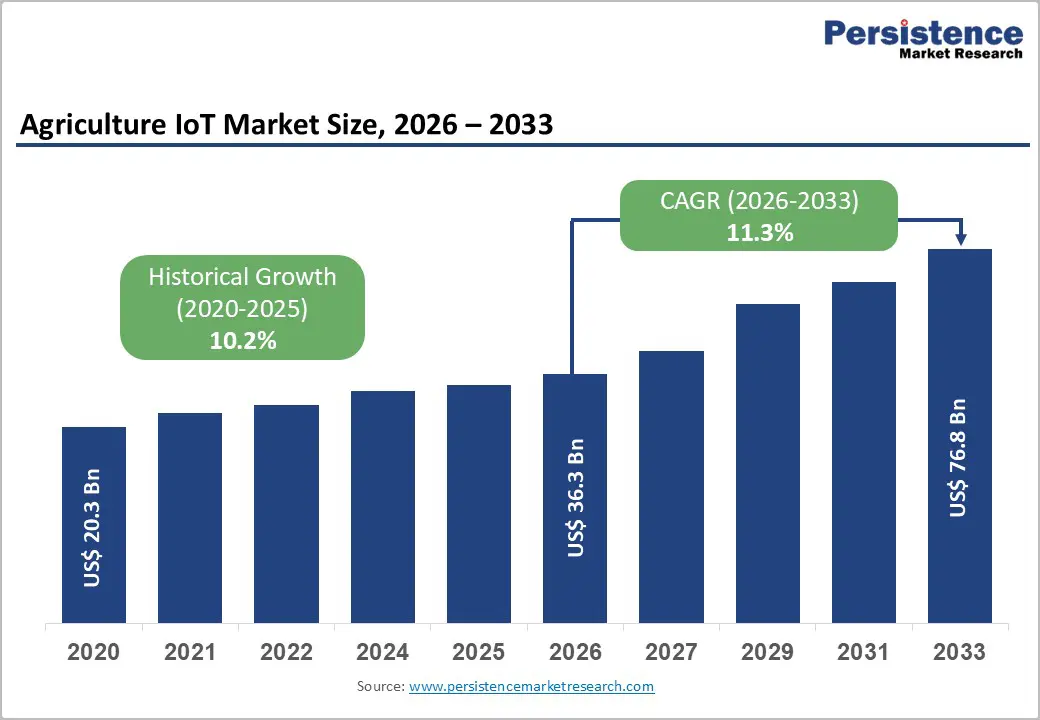

The global Agriculture IoT market is entering a strong expansion phase as farming systems worldwide transition toward data-driven, automated, and precision-based operations. Valued at approximately US$ 36.3 billion in 2026, the market is projected to reach US$ 76.8 billion by 2033, growing at a CAGR of 11.3% during the forecast period. This growth reflects the increasing urgency to improve crop productivity, reduce input wastage, and enhance resilience against climate variability and resource constraints.

Agriculture IoT, which integrates connected sensors, smart devices, cloud platforms, and analytics tools, is rapidly transforming traditional farming into a highly optimized and technology-enabled ecosystem. The combination of real-time monitoring and predictive insights is helping farmers make more informed decisions, improving both yield quality and operational efficiency.

Market Overview

The adoption of Agriculture IoT solutions is being driven by the global need to feed a growing population while minimizing environmental impact. Farmers are increasingly relying on IoT-enabled systems for soil monitoring, irrigation control, livestock tracking, greenhouse automation, and weather forecasting.

A major structural shift is underway, where farms are evolving from manually managed units to digitally connected ecosystems. This transformation is supported by advancements in connectivity technologies such as LPWAN, 5G, and satellite IoT, along with the growing affordability of sensors and cloud platforms.

Key Industry Highlights:

- Market Size (2026): US$ 36.3 Billion

- Forecast Value (2033): US$ 76.8 Billion

- CAGR (2026–2033): 11.3%

- Leading Region: North America (35% share in 2025)

- Fastest-Growing Region: Asia Pacific

- Leading Deployment: Cloud-based systems (52% share in 2025)

- Leading Connectivity: Cellular networks (38% share in 2025)

Market Dynamics

Drivers

Rising Adoption of Precision Farming

Precision farming is one of the most significant drivers of Agriculture IoT adoption. IoT-enabled sensors and GPS-based systems allow farmers to monitor soil moisture, nutrient levels, and crop health in real time. This enables targeted application of fertilizers, pesticides, and water, significantly improving yield efficiency.

Governments in regions such as Europe, North America, and Asia are actively promoting precision agriculture through subsidies and digital farming initiatives. These programs are accelerating adoption by demonstrating tangible improvements in productivity and resource optimization.

Government Support and Digital Agriculture Programs

Public sector investments in smart agriculture are playing a crucial role in market expansion. Subsidies, grants, and training programs are helping farmers overcome initial cost barriers associated with IoT adoption. In addition, international organizations are promoting digital agriculture to improve global food security and rural development.

Restraints

High Initial Investment and Infrastructure Gaps

Despite strong growth potential, the market faces challenges related to high upfront costs. IoT systems require investments in sensors, connectivity infrastructure, and analytics platforms, which can be difficult for small and mid-sized farmers.

Rural connectivity limitations further restrict adoption, particularly in developing regions where broadband access remains inconsistent. This results in partial implementation or delayed adoption of IoT solutions.

Cybersecurity and Data Privacy Concerns

As agriculture becomes more connected, concerns around data security are increasing. Farms generate sensitive operational data that can be vulnerable to cyber threats. Compliance with data protection regulations also adds complexity and increases operational costs for solution providers.

Opportunities

Integration of Edge AI and Real-Time Analytics

One of the most promising opportunities lies in the integration of edge computing and artificial intelligence. Edge-based systems allow data to be processed directly on farms, reducing latency and enabling faster decision-making for irrigation, pest control, and harvesting operations.

AI-powered platforms combining satellite imagery, drone data, and sensor inputs are already delivering predictive insights that enhance crop planning and yield forecasting.

Expansion in Emerging Markets

Emerging economies present a major growth frontier for Agriculture IoT. Affordable, scalable, and mobile-based IoT solutions are gaining traction among smallholder farmers. Governments are also supporting digital agriculture adoption to improve productivity and food security.

Low-cost sensors, solar-powered devices, and pay-as-you-go models are making IoT solutions more accessible in price-sensitive markets.

Segment Analysis

By Component

Hardware remains the dominant segment, accounting for approximately 45% share in 2025. Sensors, gateways, and smart farming equipment form the backbone of IoT ecosystems, enabling data collection and transmission across agricultural fields.

However, software is the fastest-growing segment, driven by demand for analytics platforms and AI-based farm management systems. These solutions enable predictive insights, automated decision-making, and seamless integration with cloud infrastructure.

By Deployment

Cloud-based deployment leads the market with a 52% share in 2025 due to its scalability and cost-effectiveness. It enables centralized data storage and remote monitoring of large-scale agricultural operations.

On-premise solutions continue to grow in regions with strict data governance requirements or limited connectivity. Hybrid models combining cloud and edge systems are also emerging.

By Connectivity

Cellular connectivity dominates with a 38% share in 2025, supported by widespread mobile network coverage and low-power IoT standards such as NB-IoT and LTE-M.

LPWAN and satellite-based connectivity are the fastest-growing technologies, especially in remote agricultural regions where traditional networks are unavailable.

By Farm Type

Large-scale farms account for the majority share (55% in 2025), as they have the financial capacity to invest in advanced IoT systems.

However, small and mid-sized farms are expected to grow at a faster pace due to increasing availability of affordable technologies and government assistance programs.

By Application

Precision farming holds the largest share (42% in 2025), driven by its ability to optimize inputs and maximize yields.

Aquaculture, smart greenhouses, and livestock monitoring are emerging as high-growth applications, benefiting from controlled environment agriculture and automation technologies.

Regional Analysis

North America

North America leads the Agriculture IoT market with a 35% share in 2025. The region benefits from advanced agricultural infrastructure, high adoption of precision farming, and strong government support. The United States is the primary contributor, with widespread use of autonomous machinery, drones, and AI-based farming systems.

Europe

Europe is a mature, sustainability-focused market driven by regulatory support and climate-smart agriculture initiatives. Countries such as Germany, France, and the UK are investing in digital farming technologies to improve efficiency and reduce environmental impact.

Asia Pacific

Asia Pacific is the fastest-growing region, accounting for around 28% of the market in 2025. Growth is fueled by large agricultural populations, increasing food demand, and government-led digital transformation programs in countries like India and China. Affordable IoT solutions are driving widespread adoption among smallholder farmers.

Competitive Landscape

The Agriculture IoT market is moderately consolidated, with global technology leaders and specialized regional players competing across hardware, software, and connectivity segments. Key companies are focusing on AI integration, cloud platforms, and edge computing to strengthen their market positions.

Strategic collaborations, mergers, and acquisitions are common as companies aim to expand their technological capabilities and geographic reach. Subscription-based and data-as-a-service models are also gaining popularity, making IoT solutions more accessible to farmers of all scales.

Key Developments

- Deere & Company introduced its AI-powered See & Spray system for precision herbicide application.

- Trimble Inc. partnered with Bayer to develop cloud-based crop monitoring platforms in Europe.

- Raven Industries launched autonomous IoT-enabled sprayer systems in Brazil for large-scale farms.

Key Companies Covered

Deere & Company, Trimble Inc., AGCO Corporation, Raven Industries, Topcon Corporation, DeLaval, Kubota Corporation, The Climate Corporation, Farmers Edge Inc., Ag Leader Technology, Libelium Comunicaciones Distribuidas S.L., AKVA Group, Innovasea Systems Inc., GEA Group Aktiengesellschaft, and others.

Conclusion

The Agriculture IoT market is poised for transformative growth over the forecast period as farming increasingly integrates digital intelligence, automation, and connectivity. With rising global food demand, climate pressures, and the need for resource optimization, IoT-enabled agriculture is becoming essential rather than optional.

While challenges such as high costs and connectivity gaps remain, ongoing technological advancements and strong government support are expected to accelerate adoption worldwide. The integration of AI, edge computing, and affordable IoT solutions will define the next phase of smart farming, making agriculture more efficient, sustainable, and resilient.