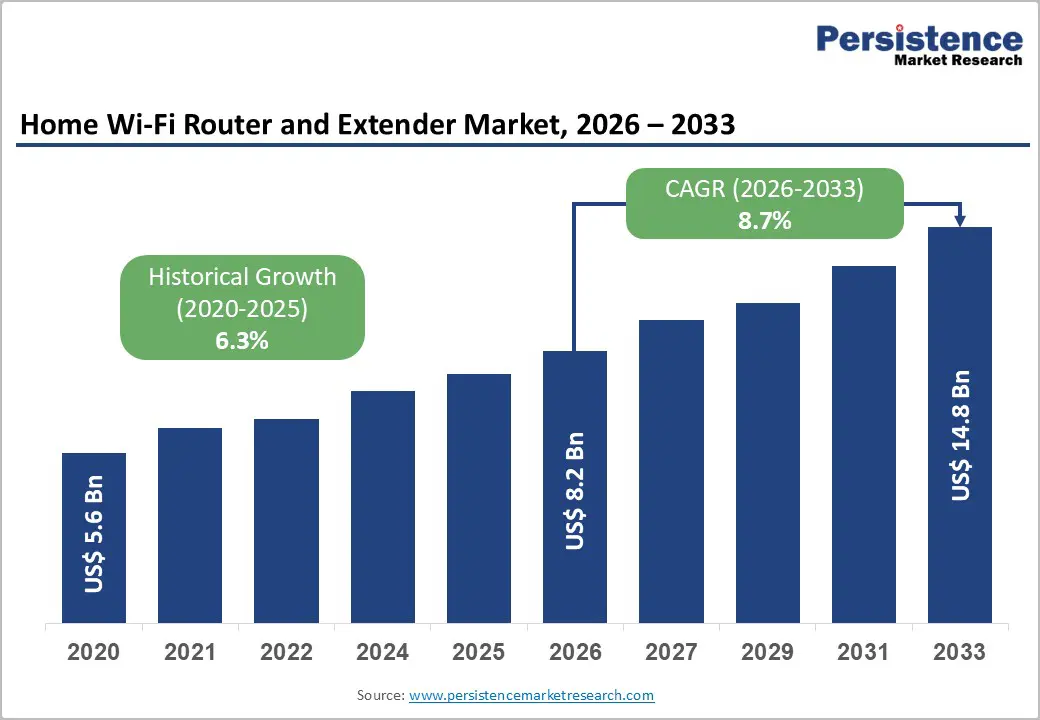

The global home Wi-Fi router and extender market is entering a strong growth phase, supported by rapid broadband expansion, increasing smart home adoption, and the transition toward high-performance wireless standards. Valued at US$8.2 billion in 2026, the market is projected to reach US$14.8 billion by 2033, expanding at a CAGR of 8.7% during the forecast period.

This growth reflects a structural shift in how households consume internet services. Connectivity is no longer limited to basic browsing or video streaming; it now supports cloud gaming, remote work, IoT ecosystems, 4K/8K media consumption, and multi-device digital lifestyles. As a result, home networking hardware is evolving from a utility product into a critical digital infrastructure component.

Market Overview

Home Wi-Fi routers and extenders form the backbone of residential connectivity, enabling seamless wireless communication between broadband networks and connected devices. The surge in global internet users—estimated at 6 billion people in 2025 (ITU)—has significantly expanded the addressable market.

At the same time, households now operate an average of 5 to 10 connected devices, including smartphones, laptops, smart TVs, gaming consoles, and IoT-enabled appliances. This multi-device environment is pushing consumers away from single-router setups toward advanced mesh networks and high-capacity routers capable of managing high bandwidth loads efficiently.

The market is also benefiting from widespread deployment of fiber broadband, with ISPs increasingly bundling routers and extenders with service plans, accelerating product penetration across both developed and emerging economies.

Key Market Highlights

- Market Size (2026): US$8.2 Billion

- Forecast Value (2033): US$14.8 Billion

- CAGR (2026–2033): 8.7%

- Leading Device Type: Routers (57% share, US$4.7 Billion in 2026)

- Leading Technology: Wi-Fi 5 (40% share, US$3.3 Billion in 2026)

- Leading Distribution Channel: Retail (42% share, US$3.4 Billion in 2026)

- Leading Region: Asia Pacific (37% share, US$3.0 Billion in 2026)

Market Dynamics

Driver: Rising Household Data Consumption and Connected Devices

One of the strongest growth drivers is the exponential rise in household data consumption. In developed markets, monthly household usage now exceeds 300 GB, driven by:

- 4K/8K video streaming

- Online gaming and cloud gaming

- Remote work and video conferencing

- Smart home automation systems

- Cloud-based storage and applications

As device density increases per household, legacy routers struggle to deliver stable coverage and low latency. This is accelerating demand for high-performance routers, Wi-Fi extenders, and mesh systems that ensure seamless connectivity across multiple rooms and devices.

The expansion of the smart home ecosystem is also reinforcing this trend. Devices such as smart speakers, security cameras, and connected appliances require continuous connectivity, making advanced routers essential household infrastructure.

Driver: Broadband Expansion and Government Digital Initiatives

Global governments are heavily investing in broadband infrastructure expansion. Programs such as:

- India’s BharatNet initiative

- U.S. BEAD Program

- EU Gigabit Society targets

are accelerating fiber-to-the-home (FTTH) and high-speed internet adoption.

According to Ericsson, global fixed broadband connections are expected to rise from 1.6 billion to 2 billion by 2030, with significant growth in fiber, FWA, and satellite connectivity.

This expansion directly fuels demand for next-generation routers capable of handling gigabit and multi-gigabit speeds, particularly in emerging markets transitioning from DSL and basic broadband to fiber networks.

Restraint: High Upgrade Costs

Despite strong demand, affordability remains a major constraint. Premium Wi-Fi 6E and Wi-Fi 7 mesh systems can cost between US$400 and US$700, making them inaccessible to many consumers in price-sensitive regions.

This leads to:

- Longer replacement cycles

- Delayed technology adoption

- Preference for refurbished or entry-level routers

Regions such as South Asia, Latin America, and Sub-Saharan Africa are particularly impacted, where cost sensitivity limits premium product penetration.

Restraint: Cybersecurity Vulnerabilities

Home routers are increasingly recognized as vulnerable points in cybersecurity ecosystems. Agencies such as CISA (U.S.) and ENISA (EU) have identified outdated firmware and weak passwords as major risks.

Key issues include:

- Unpatched firmware vulnerabilities

- Lack of consumer awareness regarding updates

- Weak encryption configurations

- Increasing IoT-based attack surfaces

As a result, regulators are considering stricter cybersecurity compliance standards for home networking devices. While this improves long-term security, it may temporarily slow market adoption due to increased compliance costs.

Opportunity: Gaming, Streaming, and Remote Work Demand

The normalization of remote and hybrid work has transformed home Wi-Fi performance expectations. High-speed, low-latency connectivity is now essential for professionals and students.

Additionally, cloud gaming platforms such as:

- NVIDIA GeForce NOW

- Xbox Cloud Gaming

- PlayStation streaming services

require ultra-low latency and stable bandwidth.

This has created a strong demand for gaming-optimized routers, featuring:

- QoS (Quality of Service) prioritization

- Low-latency modes

- Dedicated gaming bands

- Multi-gig Ethernet ports

Manufacturers are increasingly targeting these high-value user segments, enabling higher average selling prices and improved profitability.

Opportunity: Cybersecurity-Integrated Routers and Subscription Models

A major structural shift is the integration of cybersecurity features into routers. Modern devices now offer:

- Intrusion detection systems

- Parental controls

- Real-time threat monitoring

- AI-based traffic analysis

This is enabling subscription-based revenue models, where consumers pay for ongoing security services.

This convergence of networking and cybersecurity is creating a new premium segment in the market, particularly in developed regions where regulatory standards are stricter and consumer awareness is higher.

Segment Analysis

By Device Type

Routers dominate the market with over 57% share in 2026. They serve as the central connectivity hub in every household. Growth is supported by:

- Fiber broadband expansion

- Increasing bandwidth requirements

- Demand for dual-band and tri-band performance

- Smart home integration

Meanwhile, mesh systems are the fastest-growing segment, driven by:

- Need for whole-home coverage

- Elimination of Wi-Fi dead zones

- Seamless roaming between nodes

- Growing multi-floor housing structures

By Technology

Wi-Fi 5 continues to dominate due to affordability and widespread adoption. It remains sufficient for HD streaming and general internet usage.

However, Wi-Fi 7 is emerging as the most disruptive technology, driven by:

- Ultra-high-speed broadband expansion

- Cloud gaming and AR/VR applications

- Dense device environments

- Lower latency requirements

Wi-Fi 6E acts as a transitional standard, bridging legacy systems and next-generation connectivity.

By Distribution Channel

Retail channels lead the market, accounting for over 42% share in 2026. Consumers prefer retail due to:

- Product comparison flexibility

- Brand variety

- Promotional discounts

- E-commerce accessibility

However, the ISP/telco bundled segment is growing fastest, with a projected CAGR of 11.6%, as service providers offer:

- Plug-and-play devices

- Bundled broadband packages

- Device financing options

- Managed Wi-Fi services

Regional Analysis

Asia Pacific

Asia Pacific dominates the global market with 37% share in 2026. Growth drivers include:

- Massive broadband subscriber base

- Strong manufacturing ecosystem (China, Taiwan)

- Low-cost internet availability

- Rapid urbanization

India and Southeast Asia are witnessing strong first-time adoption, while Japan and South Korea are early adopters of high-performance routers.

North America

North America accounts for 32% market share. The region benefits from:

- Near-universal broadband access

- High disposable income

- Strong demand for premium Wi-Fi 6E/7 systems

- Early adoption of smart home technologies

Government initiatives such as BEAD are also expanding rural connectivity.

Europe

Europe holds around 24% market share, driven by:

- EU Digital Decade 2030 initiatives

- High FTTH penetration

- Strong cybersecurity regulations

- Growing adoption of mesh systems

Countries such as Germany, the UK, and France dominate regional demand.

Competitive Landscape

The market is moderately consolidated, with key players focusing on innovation, ecosystem integration, and premiumization strategies.

Leading companies include:

- TP-Link Technologies

- NETGEAR Inc.

- ASUS (ASUSTeK Computer Inc.)

- Huawei Technologies

- D-Link Corporation

- Xiaomi Corporation

- Linksys Holdings

- Amazon

- Ubiquiti Inc.

- Nokia

Strategic Trends

- Expansion into Wi-Fi 7 product lines

- AI-powered network optimization tools

- Subscription-based security services

- ISP partnerships and co-branded devices

- Integration with smart home ecosystems (Matter protocol)

Recent innovations such as ASUS’s next-generation Wi-Fi concepts and TP-Link’s expanded Wi-Fi 7 portfolio highlight the industry’s focus on performance and future-ready connectivity.

Conclusion

The home Wi-Fi router and extender market is transitioning from a mature hardware segment into a dynamic, software-enabled connectivity ecosystem. Growth is being driven by increasing data consumption, smart home proliferation, and rapid broadband infrastructure expansion.

Between 2026 and 2033, the market will be shaped by three major forces:

- Technology evolution (Wi-Fi 6E → Wi-Fi 7 → Wi-Fi 8 concepts)

- Convergence of networking and cybersecurity services

- Shift toward mesh and managed Wi-Fi ecosystems

As digital lifestyles deepen globally, home networking devices will become increasingly essential, ensuring sustained long-term growth for the industry.