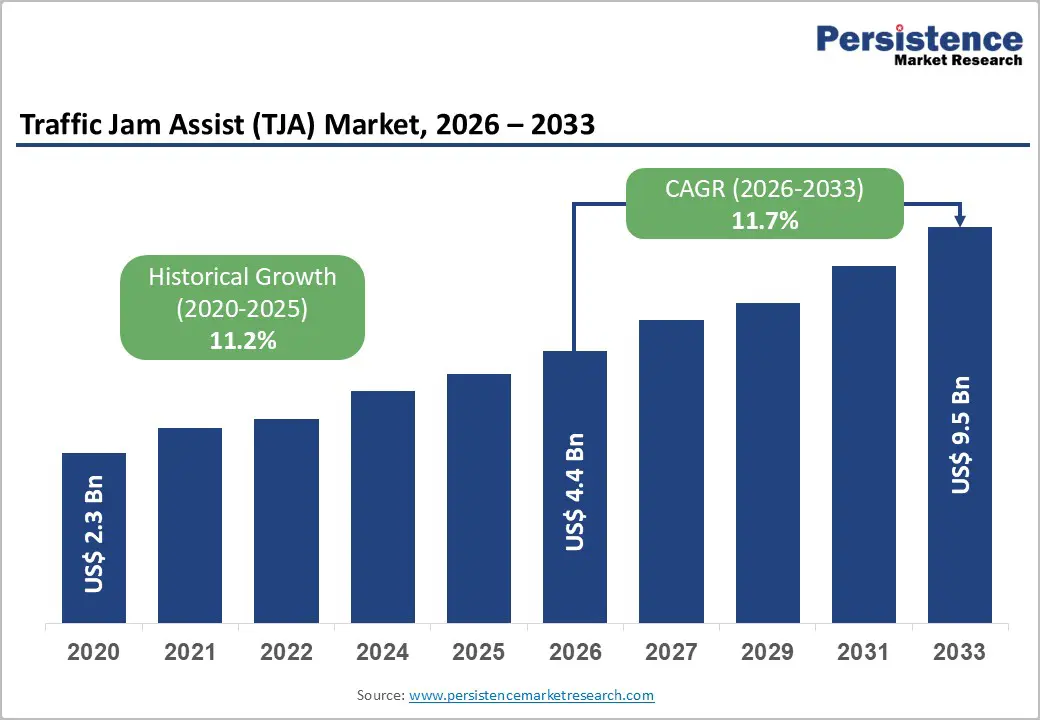

The global Traffic Jam Assist (TJA) market is entering a strong growth phase as automotive intelligence rapidly shifts from basic driver assistance toward semi-autonomous driving capabilities. Valued at approximately US$ 4.4 billion in 2026, the market is projected to reach US$ 9.5 billion by 2033, expanding at a CAGR of 11.7% during the forecast period. This expansion is strongly supported by accelerating adoption of Advanced Driver-Assistance Systems (ADAS), rising urban congestion, and continuous improvements in sensor fusion, artificial intelligence (AI), and connected vehicle ecosystems.

TJA systems are designed to support drivers in stop-and-go traffic conditions by automatically managing acceleration, braking, and steering within defined limits. As global cities become increasingly congested and mobility patterns evolve, these systems are transitioning from premium features to mainstream automotive expectations.

Market Overview

Traffic Jam Assist represents a key building block in the broader evolution toward Level-2 and Level-3 autonomous driving. It integrates radar, cameras, ultrasonic sensors, and AI-based decision-making systems to maintain safe distances, control lane positioning, and reduce driver workload in dense traffic environments.

The market’s expansion is closely tied to the increasing penetration of ADAS across both passenger and commercial vehicles. Automakers are now embedding TJA systems either as standard features in mid-to-high-end vehicles or as optional upgrades in mass-market models. This democratization of semi-autonomous technology is reshaping competitive dynamics in the automotive industry.

Key Market Insights

| Parameter | Value |

| Market Size (2026E) | US$ 4.4 Billion |

| Market Forecast (2033F) | US$ 9.5 Billion |

| CAGR (2026–2033) | 11.7% |

| Historical CAGR (2020–2025) | 11.2% |

| Leading Region (2026) | North America (~38%) |

| Fastest Growing Region | Asia Pacific |

Key Industry Trends

- Expansion of ADAS Across Vehicle Segments

One of the most significant trends shaping the TJA market is the rapid integration of ADAS technologies into both premium and mass-market vehicles. What was once limited to luxury vehicles is now becoming a standard expectation, particularly in urban passenger cars.

- Rise of AI-Driven Mobility Intelligence

AI and machine learning are transforming TJA systems from rule-based automation to adaptive, predictive driving assistants. These systems now learn from traffic patterns, driver behavior, and environmental conditions to improve responsiveness and safety.

- Sensor Fusion as a Core Technology Pillar

Radar continues to dominate due to reliability in all weather conditions, while camera and LiDAR systems enhance object detection and lane tracking. The fusion of these sensors improves system accuracy and reduces false detection rates.

- Electrification and Smart Vehicle Platforms

Electric vehicles (EVs) are emerging as a major growth platform for TJA systems. Their software-defined architecture allows seamless integration of ADAS features, OTA updates, and cloud connectivity.

Market Drivers

Rising Safety Awareness and Accident Reduction Efforts

Road safety remains a major global concern. Millions of accidents occur annually due to human error, distraction, and congestion-related fatigue. Governments and safety organizations are increasingly promoting driver assistance systems that reduce collision risks.

In regions like North America and Europe, regulatory bodies such as the National Highway Traffic Safety Administration (NHTSA) are strengthening ADAS guidelines. These initiatives encourage automakers to integrate systems like Traffic Jam Assist as part of broader safety compliance strategies.

Urbanization and Traffic Congestion

Rapid urbanization has led to severe traffic congestion in major metropolitan regions. As commuting times increase, drivers experience fatigue and stress, creating demand for automated support systems that enhance comfort and reduce workload.

Regulatory Push for Vehicle Safety Standards

Governments worldwide are introducing structured frameworks for semi-autonomous systems. These policies not only ensure safer deployment but also accelerate commercialization by providing clear technical and legal guidelines for OEMs.

Market Restraints

High Implementation Costs

One of the major challenges for the TJA market is the high cost of advanced sensors, ECUs, and AI-based software systems. Radar, camera arrays, and control modules require precise engineering and calibration, increasing production costs.

These costs are particularly challenging for entry-level and mid-range vehicles, where price sensitivity limits adoption rates.

Technical Complexity and Reliability Issues

Traffic Jam Assist systems must operate in highly dynamic and unpredictable environments. Variations in weather, road markings, and driver behavior can impact performance reliability.

Ensuring consistent operation across global markets requires extensive testing and validation, increasing development timelines and costs.

Supply Chain Constraints

Semiconductor shortages and sensor supply limitations continue to affect production stability. These constraints directly impact manufacturing scalability and pricing structures.

Market Opportunities

Expansion of Semi-Autonomous and Connected Vehicles

The growing ecosystem of connected and semi-autonomous vehicles presents a major opportunity. Vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication systems enhance TJA performance by enabling real-time traffic coordination.

Entry into Mass-Market Vehicles

As production scales and component costs decline, TJA systems are increasingly being integrated into mid-range and economy vehicles. This expansion significantly increases the addressable market size.

Growth in EV and Shared Mobility Fleets

Electric and shared mobility fleets are ideal platforms for TJA adoption due to predictable routes, centralized management, and high utilization rates. Ride-sharing companies are increasingly adopting ADAS features to improve safety and operational efficiency.

Component Analysis

Radar Sensors – Leading Segment

Radar sensors are expected to hold over 40% market share in 2026 due to their reliability in adverse weather conditions and accurate distance measurement capabilities. They form the backbone of most TJA systems.

Software and AI – Fastest Growing Segment

AI-driven software solutions are projected to be the fastest-growing segment from 2026 to 2033. These systems enable real-time decision-making, predictive analytics, and over-the-air upgrades, making them essential for next-generation mobility platforms.

Vehicle Type Analysis

Passenger Cars – Dominant Segment

Passenger vehicles account for approximately 60% of total market share in 2026, driven by rising urban adoption and increasing consumer preference for safety and convenience features.

Electric Vehicles – Fastest Growing Segment

EVs are expected to show the highest growth rate due to their software-defined architecture and compatibility with advanced driver-assistance systems. Their integration flexibility makes them ideal for TJA deployment.

Regional Analysis

North America

North America leads the global TJA market with approximately 38% share in 2026. Strong OEM presence, advanced infrastructure, and early adoption of ADAS technologies support regional dominance. The U.S. remains a key innovation hub for autonomous driving systems.

Europe

Europe demonstrates strong regulatory-driven adoption. Strict safety regulations, long commuting durations, and high consumer awareness drive demand for Traffic Jam Assist systems. OEMs actively integrate ADAS features to meet compliance standards.

Asia Pacific

Asia Pacific is the fastest-growing region due to rapid urbanization, rising vehicle ownership, and expanding smart mobility initiatives. Countries like China, India, Japan, and South Korea are investing heavily in connected transportation systems.

Competitive Landscape

The TJA market is moderately consolidated, with major Tier-1 suppliers and automotive technology firms dominating the ecosystem. Key players include:

- Bosch

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- Valeo SA

- Hyundai Mobis

- Magna International

- NXP Semiconductors

- Texas Instruments

- Infineon Technologies AG

- Veoneer AB

These companies compete through innovation in sensor fusion, AI software, system integration, and global OEM partnerships. Strategic collaborations and acquisitions are common as firms aim to strengthen their ADAS portfolios.

Recent Developments

In 2025, several automakers expanded their ADAS offerings with integrated Traffic Jam Assist features:

- MG introduced the Windsor EV Pro featuring Level-2 TJA for automated stop-and-go traffic management.

- Geely launched the Cityray, incorporating radar- and camera-based TJA functionality for improved urban driving comfort.

These developments highlight the growing shift toward mainstream adoption of semi-autonomous driving features.

Conclusion

The Traffic Jam Assist (TJA) market is positioned for sustained expansion through 2033, driven by rapid technological advancements, increasing urban congestion, and strong regulatory support for vehicle safety systems. As AI, sensor fusion, and connected vehicle technologies continue to mature, TJA will evolve from a convenience feature into a standard component of modern mobility ecosystems.

With strong growth in electric vehicles, expansion into mass-market segments, and increasing consumer demand for safety and comfort, Traffic Jam Assist systems are expected to play a central role in shaping the future of intelligent transportation.