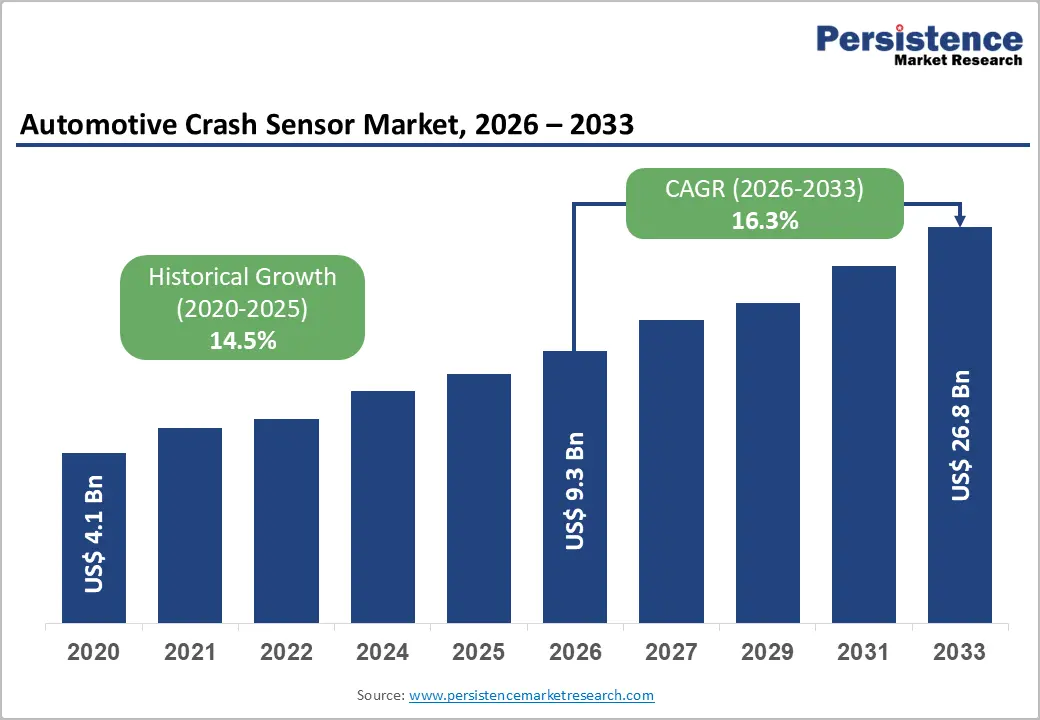

The global automotive crash sensor market is undergoing a period of rapid structural expansion, driven by tightening safety regulations, accelerated electrification, and the growing integration of advanced driver assistance systems (ADAS). Valued at US$ 9.3 billion in 2026, the market is projected to reach US$ 26.8 billion by 2033, reflecting a strong CAGR of 16.3% during the forecast period. This growth trajectory highlights a fundamental shift in how modern vehicles are designed, where crash sensing has evolved from a passive safety function to a core intelligence layer within vehicle architecture.

A combination of regulatory mandates, technological innovation in MEMS (Micro-Electro-Mechanical Systems), and rising consumer expectations for safety is reshaping the competitive landscape. Crash sensors are no longer limited to airbag deployment systems; they now play a critical role in predictive safety systems, battery isolation in electric vehicles, rollover detection, and multi-domain sensor fusion platforms that underpin semi-autonomous driving.

Market Drivers: Regulation, Electrification, and ADAS Expansion

The most powerful growth driver for the automotive crash sensor market is the global tightening of vehicle safety regulations. In the United States, the National Highway Traffic Safety Administration (NHTSA) finalized FMVSS No. 127, mandating Automatic Emergency Braking (AEB) systems, including pedestrian detection, across all new passenger vehicles by September 2029. This regulation alone is expected to prevent thousands of fatalities and injuries annually, while significantly increasing the sensor content per vehicle.

Similarly, Europe’s Euro NCAP protocols are becoming increasingly stringent, requiring advanced side-impact protection, improved frontal collision response, and expanded occupant safety systems. These evolving standards compel automakers to integrate multi-sensor crash detection systems, including accelerometers, gyroscopes, and pressure sensors, across multiple vehicle zones.

The second major driver is the rapid rise of electric vehicles (EVs) and ADAS-equipped vehicles. Global EV sales surpassed 14 million units in 2023, growing more than 35% year-on-year according to the International Energy Agency. EV platforms require specialized crash sensing systems capable of triggering high-voltage battery isolation within milliseconds of impact to prevent thermal runaway. This requirement significantly increases both the complexity and value of crash sensor systems per vehicle.

Additionally, modern ADAS architectures depend on crash sensors as foundational inputs for systems such as lane-keeping assist, automatic emergency braking, and adaptive stability control. As vehicles transition toward semi-autonomous and autonomous operation, sensor density per vehicle continues to rise sharply, reinforcing long-term demand growth.

Technology Trends: MEMS Miniaturization and Sensor Fusion

A key technological enabler of market expansion is the advancement of MEMS-based crash sensors. MEMS technology has enabled dramatic reductions in sensor size, cost, and power consumption while improving accuracy and reliability. Leading suppliers such as Bosch have produced billions of MEMS sensors, with modern vehicles now integrating more than 50 sensors on average across multiple safety and control systems.

This miniaturization trend has allowed crash sensors to be embedded not only in traditional airbag systems but also in structural zones such as bumpers, doors, roof pillars, and battery enclosures. The result is a distributed sensing architecture that enhances crash detection accuracy and response time.

Another transformative trend is sensor fusion and AI-driven predictive safety systems. Instead of relying solely on post-impact signals, next-generation platforms combine data from accelerometers, pressure sensors, radar, and cameras to predict collisions before they occur. This enables pre-emptive airbag deployment and proactive occupant protection strategies. Partnerships such as Bosch’s collaboration with Microsoft to integrate generative AI into mobility systems highlight the increasing convergence of automotive safety and artificial intelligence.

Market Restraints: Complexity and Supply Chain Challenges

Despite strong growth momentum, the automotive crash sensor market faces several structural challenges. One of the primary restraints is the high integration complexity associated with modern sensor systems. Crash sensors must operate within millisecond-level response windows while maintaining full compatibility with electronic control units (ECUs), restraint systems, and ADAS platforms. Achieving this level of precision requires extensive calibration and validation, significantly increasing development timelines.

Compliance with functional safety standards such as ISO 26262 further adds to the complexity. Achieving Automotive Safety Integrity Level (ASIL) certification requires rigorous testing and verification, which can extend product development cycles to several years. This creates a high entry barrier for new market participants and consolidates the position of established Tier 1 suppliers.

Supply chain constraints also pose challenges. Crash sensors depend heavily on MEMS wafers, ASICs, and automotive-grade semiconductors, all of which are subject to global supply volatility. Long qualification cycles—often 18 to 24 months—limit flexibility and slow down production scaling. While increasing 300 mm wafer capacity is gradually easing pressure, regional localization requirements in markets such as China and India continue to complicate global supply chain structures.

Opportunities: EV-Specific Systems and Predictive Safety Innovation

One of the most significant opportunities in the automotive crash sensor market lies in EV-specific crash sensing architectures. Unlike internal combustion engine vehicles, EVs require crash sensors capable of simultaneously detecting collision severity, triggering occupant protection systems, and isolating high-voltage battery packs within milliseconds. This multi-function requirement significantly increases the value per sensor system.

Companies such as Denso are actively developing next-generation crash sensors tailored for EV platforms, reflecting a broader industry shift toward electrification-specific safety solutions. With EV adoption expected to continue growing at a double-digit pace globally, this segment is poised to become one of the most lucrative areas of market expansion.

Another major opportunity is the emergence of AI-integrated predictive crash sensing. By leveraging sensor fusion and machine learning, future systems will be capable of anticipating crashes and initiating safety responses before impact occurs. These capabilities are increasingly being rewarded under evolving Euro NCAP and NHTSA frameworks, allowing suppliers offering advanced predictive systems to command premium pricing and secure long-term OEM contracts.

Segment Analysis

Accelerometers dominate the product landscape, accounting for approximately 38% of global market share. Their critical role in detecting vehicle deceleration makes them essential for airbag deployment and stability control systems. Gyroscopes and pressure sensors also play important supporting roles in multi-axis crash detection systems.

By application, airbag systems remain the largest segment, representing about 55% of total demand. Increasing airbag penetration across vehicle classes, particularly in emerging markets, continues to drive sensor adoption. Regulatory pushes in regions like India and China are accelerating the shift toward multi-airbag configurations even in mid-range vehicles.

In terms of vehicle type, hatchbacks and sedans lead the market with approximately 45% share due to their high global production volumes. These platforms serve as the primary adoption base for crash sensors, especially in Asia Pacific and Europe.

Front bumper-mounted sensors represent the largest placement segment, accounting for roughly 40% of demand. These sensors are essential for front-impact detection and AEB systems, which are now central to global safety regulations.

Regional Insights

North America remains the leading regional market due to strong regulatory enforcement and technological leadership. The FMVSS No. 127 mandate has created a structural demand base for advanced crash sensing systems, while major suppliers such as Bosch, Continental, and Honeywell continue to drive innovation in the region.

Asia Pacific is the fastest-growing region, led by China, India, and Japan. China’s C-NCAP program and India’s Bharat NCAP are rapidly increasing safety requirements, while domestic EV manufacturers such as BYD, NIO, and Geely are accelerating sensor adoption. Japan continues to serve as a global hub for MEMS manufacturing and sensor innovation.

Europe remains a key innovation center, driven by Euro NCAP standards and strong OEM presence in Germany, France, and the UK. Companies such as Bosch, Continental, and ZF are leading advancements in sensor fusion and integrated safety systems.

Competitive Landscape

The automotive crash sensor market is moderately consolidated, dominated by global Tier 1 suppliers including Bosch Mobility Solutions, Continental AG, ZF Friedrichshafen, and Denso Corporation. These companies maintain strong OEM relationships and lead in MEMS innovation, functional safety certification, and sensor fusion technologies.

Competition is increasingly centered around software capabilities, AI integration, and platform-level safety solutions rather than standalone hardware. Strategic partnerships, such as Bosch’s collaboration with Microsoft, reflect the industry’s shift toward software-defined vehicle safety ecosystems.

Conclusion

The automotive crash sensor market is entering a transformative growth phase driven by regulatory mandates, electrification, and intelligent vehicle architectures. From US$ 9.3 billion in 2026 to US$ 26.8 billion by 2033, the market’s expansion reflects a broader evolution in automotive safety philosophy—moving from reactive protection to predictive intelligence. As vehicles become more autonomous and electrified, crash sensors will remain at the core of next-generation mobility safety systems, creating sustained opportunities for innovation and high-value market expansion.