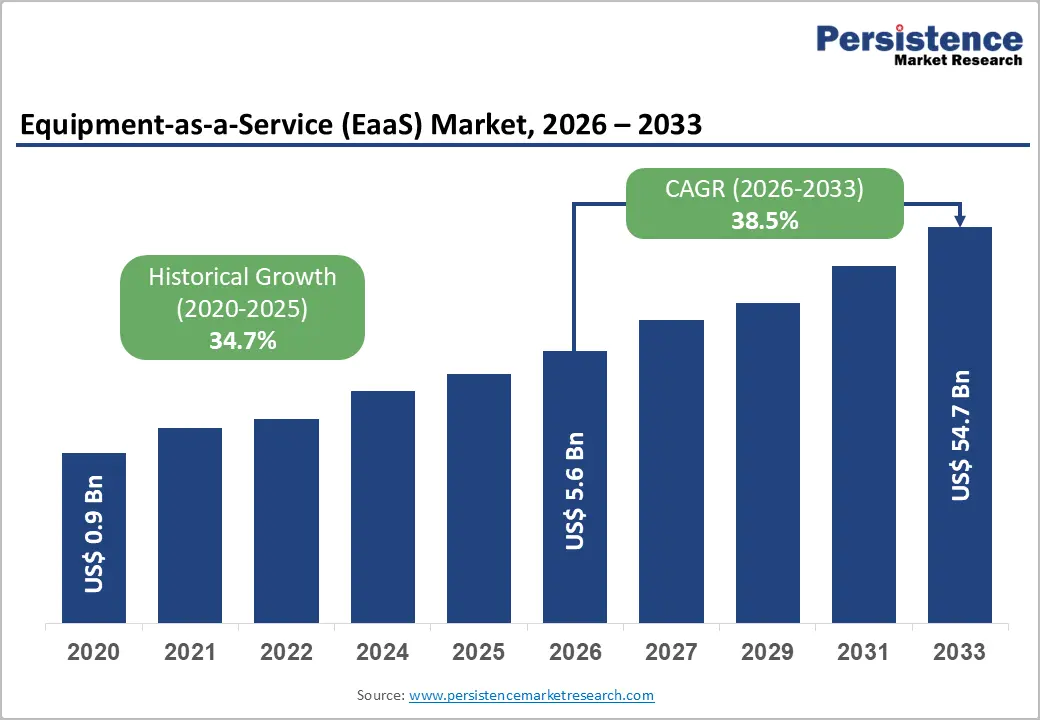

The global Equipment-as-a-Service (EaaS) market is undergoing a structural transformation, reshaping how industrial assets are acquired, financed, and utilized. Valued at approximately US$5.6 billion in 2026, the market is projected to surge dramatically to US$54.7 billion by 2033, reflecting an exceptional CAGR of 38.5% during the forecast period.

This rapid expansion is driven by a fundamental shift from traditional capital expenditure (CapEx) models toward operational expenditure (OpEx) frameworks. Industries that rely heavily on machinery and equipment are increasingly prioritizing flexibility, cost efficiency, and performance-based outcomes over ownership.

The evolution of EaaS is also closely linked to the rise of Industrial IoT (IIoT), artificial intelligence (AI), cloud computing, and 5G connectivity, which together enable real-time equipment monitoring, predictive maintenance, and outcome-based service delivery models. These technologies are turning physical assets into intelligent, connected systems capable of generating continuous value beyond initial deployment.

Key Market Drivers and Structural Shifts

One of the most important forces shaping the EaaS market is the growing emphasis on total cost of ownership (TCO) optimization. Enterprises across manufacturing, construction, energy, and logistics sectors are increasingly focused on reducing downtime, extending asset lifecycles, and improving operational efficiency.

EaaS enables organizations to align equipment usage directly with production demand, minimizing idle capacity and unnecessary capital lock-ins. Instead of purchasing expensive machinery, companies can now subscribe to or pay for equipment based on usage or performance outcomes.

The increasing complexity of modern industrial equipment also plays a critical role. Advanced machinery now requires specialized maintenance, digital diagnostics, and software-based optimization—capabilities that are more efficiently delivered by OEMs and service providers rather than in-house teams.

Additionally, rising global competition and supply chain volatility are pushing enterprises to adopt more agile asset management strategies, further accelerating EaaS adoption.

Key Industry Highlights

Several structural insights define the current and future landscape of the EaaS market:

- Leading Service Type: Maintenance & Support services dominate with over 30% share in 2026, valued at more than US$1.7 billion, driven by the need for continuous uptime and predictive maintenance.

- Leading Service Model: Subscription-based models account for over 48% share, valued at more than US$2.7 billion, due to predictable cost structures and bundled offerings.

- Leading End User: Manufacturing leads with over 32% share, valued at more than US$1.8 billion, supported by high machinery dependency and automation trends.

- Leading Region: North America dominates with over 37% share, valued at around US$2.1 billion, due to strong digital infrastructure and mature rental ecosystems.

These highlights demonstrate that EaaS is no longer a niche financing alternative but a mainstream industrial operating model.

Service Type Analysis

Maintenance & Support Services

Maintenance and support services remain the backbone of the EaaS ecosystem, capturing over 30% market share in 2026. The dominance of this segment is rooted in the critical importance of minimizing downtime in industrial operations.

Organizations are increasingly outsourcing maintenance functions to specialized providers to reduce operational risks and avoid unexpected breakdown costs. Predictive and preventive maintenance strategies—powered by IoT sensors and AI analytics—are extending equipment lifespans and improving reliability.

As industrial systems become more sophisticated, the need for highly skilled technical support continues to grow. This trend reinforces long-term service contracts and deepens vendor-client integration.

Monitoring & Remote Management

The monitoring and remote management segment is emerging as one of the fastest-growing areas in the EaaS market. IoT-enabled sensors and cloud-based platforms allow real-time tracking of equipment performance, enabling predictive insights and rapid issue detection.

This capability significantly reduces the need for manual inspections and on-site maintenance, lowering operational costs. Remote monitoring also improves decision-making by providing data-driven insights into equipment utilization, efficiency, and failure risks.

Service Model Analysis

Subscription-Based Models

Subscription-based EaaS models dominate the market with over 48% share in 2026. These models provide businesses with predictable expenses, eliminating large upfront capital investments.

For small and medium enterprises (SMEs), this structure improves accessibility to advanced machinery that would otherwise be financially prohibitive. For large enterprises, subscription models simplify budgeting and align equipment costs with production cycles.

Additionally, subscription contracts often include maintenance, upgrades, and software updates, ensuring continuous access to the latest technology. This strengthens long-term customer relationships and creates recurring revenue streams for providers.

Pay-Per-Use Models

Pay-per-use models are expected to grow at an impressive CAGR of 44.1%, driven by demand for flexibility and efficiency. These models are particularly valuable in industries with fluctuating workloads, such as construction, logistics, and seasonal manufacturing.

By charging based on actual usage, companies avoid the risk of underutilized assets. Advanced metering technologies and digital tracking systems now make precise usage-based billing possible.

This model also aligns with sustainability goals, as it encourages efficient resource utilization and reduces wasteful consumption of equipment capacity.

End-User Analysis

Manufacturing Sector

Manufacturing remains the largest end-user segment, accounting for over 32% market share in 2026. The sector’s reliance on high-value machinery and continuous production cycles makes EaaS particularly attractive.

With the rise of smart factories and Industry 4.0, manufacturers are increasingly integrating connected equipment and automated systems. EaaS enables them to maintain operational agility without heavy capital investment.

It also allows manufacturers to scale production quickly in response to demand fluctuations while minimizing downtime risks through predictive maintenance.

Construction Sector

The construction industry is projected to grow at a CAGR of 41.6%, making it one of the fastest-expanding EaaS segments. Construction projects are inherently temporary and variable, making ownership of heavy equipment inefficient.

EaaS provides contractors with flexible access to machinery, enabling them to scale equipment usage based on project requirements. This reduces idle equipment costs and improves cash flow efficiency.

Additionally, the adoption of smart construction technologies and connected machinery is further accelerating demand for service-based equipment models.

Regional Analysis

North America

North America leads the global EaaS market with over 37% share in 2026, valued at approximately US$2.1 billion. The region benefits from a highly mature rental and leasing ecosystem, strong digital adoption, and advanced financial infrastructure.

Government initiatives such as the Infrastructure Investment and Jobs Act (US$1.2 trillion) and semiconductor reshoring through the CHIPS Act are fueling demand for industrial equipment across construction and manufacturing sectors.

The presence of leading OEMs and technology providers further strengthens the region’s dominance. Predictive maintenance and performance-based contracts are increasingly standard across industries.

Asia Pacific

Asia Pacific is expected to be the fastest-growing region, with a CAGR of 45.2%. Rapid industrialization, urbanization, and infrastructure development across China, India, Japan, and Southeast Asia are driving demand.

India’s National Infrastructure Pipeline and China’s manufacturing modernization programs are significantly boosting equipment demand. Japan’s Society 5.0 initiative is also accelerating adoption of smart, connected industrial systems.

However, challenges such as fragmented leasing markets and SME financing constraints may slightly slow adoption in certain segments.

Europe

Europe is projected to hold more than 26% market share by 2026, driven by strong regulatory frameworks and sustainability initiatives. Germany, the UK, and France are leading adopters due to advanced industrial automation.

Policies such as the European Green Deal and EU Machinery Regulation (2023/1230) are encouraging efficient, low-emission equipment usage. These regulations are indirectly accelerating EaaS adoption by promoting asset optimization and lifecycle efficiency.

The market remains fragmented, creating consolidation opportunities for strategic investors and private equity firms.

Competitive Landscape

The global EaaS market is highly fragmented, with the top players accounting for only a modest share of total market concentration. This fragmentation creates significant opportunities for consolidation, mergers, and acquisitions.

Leading companies are focusing on integrating IoT, AI-driven diagnostics, digital twins, and ESG-compliant equipment fleets into their service offerings. These enhancements allow providers to shift from product-based sales models to outcome-based service ecosystems.

Large incumbents benefit from established equipment bases and long-term customer relationships, enabling them to build stable recurring revenue streams. Meanwhile, emerging players are introducing innovative financing and usage-based models to capture niche segments.

Recent Developments

Several key developments highlight the accelerating adoption of EaaS models:

- In December 2025, Volvo CE India reported that its EaaS model reached a revenue milestone of approximately INR 100 crore, with services contributing nearly 30% of total revenue.

- In April 2025, EASE expanded its EaaS model into South Africa by securing its first international lender, enabling pay-per-use access to medical equipment for healthcare providers.

These developments reflect the growing diversification of EaaS applications beyond traditional industrial sectors into healthcare and emerging markets.

Key Companies in the EaaS Market

Major players shaping the global EaaS ecosystem include:

Caterpillar Inc., Komatsu Ltd., Atlas Copco AB, Hitachi Construction Machinery Co., Volvo Group, Siemens AG, Deere & Company, Sandvik AB, Schneider Electric SE, Hilti Corporation, Raiffeisen Leasing d.o.o., TRUMPF, Nitrobox GmbH, United Rentals, Inc., among others.

Conclusion

The Equipment-as-a-Service (EaaS) market is transitioning from a disruptive concept into a mainstream industrial model. With projected growth from US$5.6 billion in 2026 to US$54.7 billion by 2033, the sector represents one of the most significant transformations in industrial asset management.

Driven by digitalization, sustainability goals, and financial flexibility, EaaS is redefining how businesses access and utilize equipment. As industries continue to prioritize efficiency, uptime, and capital optimization, EaaS is expected to become a foundational pillar of the global industrial economy.