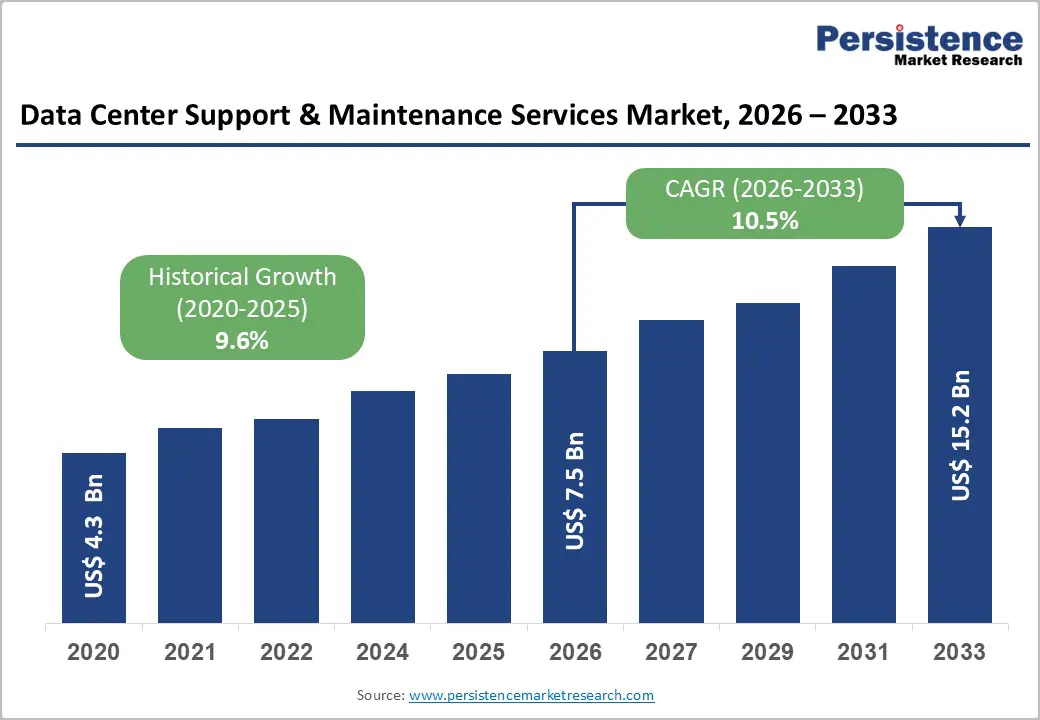

The global data center support & maintenance services market is undergoing a rapid transformation as digital infrastructure becomes the backbone of the modern global economy. Valued at US$ 7.5 billion in 2026, the market is projected to reach US$ 15.2 billion by 2033, expanding at a robust CAGR of 10.5% during the forecast period. This growth reflects the rising dependency on uninterrupted digital services, fueled by AI adoption, hyperscale cloud expansion, and the exponential increase in global data traffic.

As enterprises, governments, and consumers continue shifting toward data-intensive applications, the need for reliable, scalable, and always-on data center infrastructure has never been greater. Support and maintenance services have evolved from traditional break-fix models into predictive, AI-driven, and SLA-based lifecycle management solutions that ensure operational continuity in mission-critical environments.

Market Overview and Growth Dynamics

The expansion of the data center support & maintenance services market is deeply rooted in the accelerating digitization of global economies. Internet usage alone highlights the scale of this transformation. According to the International Telecommunication Union, approximately 5.5 billion people—around 68% of the global population—are now online, with adoption continuing to grow annually at over 3%.

This surge in connectivity has resulted in massive growth in cloud workloads, streaming services, online commerce, and AI-powered applications. Each of these depends on high-availability data centers that require constant monitoring, maintenance, and optimization.

Hyperscale data centers, in particular, are becoming the dominant infrastructure model. These facilities support cloud giants, AI training clusters, and global content delivery networks. Their complexity and scale necessitate advanced predictive maintenance systems, remote diagnostics, and highly specialized engineering support.

Key Market Drivers

- Rapid Expansion of AI and Cloud Infrastructure

Artificial intelligence and cloud computing are the strongest growth catalysts for the market. AI workloads demand high-density GPU clusters, advanced cooling systems, and ultra-low-latency networking environments. These systems generate significantly higher heat loads and operational stress, increasing the need for proactive maintenance.

Cloud service providers are continuously expanding hyperscale campuses across North America, Europe, and Asia Pacific. Each expansion adds thousands of servers, storage units, and networking devices that must be monitored and maintained 24/7.

- Global Internet Penetration and Digital Consumption

The expansion of global internet access is another major driver. China alone has over 1.1 billion internet users, while India has nearly 955 million subscribers. Europe reports internet penetration of over 94% in many countries, while global digital service consumption continues to accelerate.

This widespread connectivity increases demand for digital platforms such as e-commerce, fintech, social media, and cloud-based enterprise tools—all of which rely on resilient data center operations.

- Growth of E-Commerce and Digital Platforms

The global B2B e-commerce sector has grown dramatically, reaching trillions of dollars in gross merchandise value. Asia Pacific dominates global digital commerce activity, accounting for nearly 80% of total GMV.

Each transaction, recommendation engine, and logistics system depends on continuous backend data processing. This directly increases demand for data center uptime assurance, hardware lifecycle optimization, and network reliability services.

Regional Market Analysis

Asia Pacific: Fastest Expanding Digital Infrastructure Hub

Asia Pacific holds approximately 30% of the global market share and continues to be the fastest-growing region. China and India are the primary growth engines, driven by massive internet populations and large-scale government digital initiatives.

China’s advanced digital ecosystem, including e-government platforms and AI applications, places enormous pressure on data center infrastructure. India’s BharatNet program and expanding telecom infrastructure have significantly increased connectivity across rural and urban areas, expanding the installed base of IT infrastructure requiring maintenance.

North America: Market Leader in Revenue Share

North America accounts for around 38% of global revenue, making it the largest regional market. The United States leads in hyperscale data center deployment, AI innovation, and predictive maintenance technologies.

The presence of major cloud providers and technology giants has created a highly advanced ecosystem where AI-driven monitoring, remote diagnostics, and automated maintenance systems are widely adopted. Government digital transformation programs further strengthen demand for secure and resilient data center operations.

Europe: Stable Growth with Strong Regulatory Frameworks

Europe holds nearly 20% of the market share. Countries such as Germany, the UK, France, and the Netherlands are key contributors due to high digital adoption and strong enterprise cloud usage.

Strict data protection regulations and sustainability requirements in Europe are also influencing maintenance strategies. Organizations increasingly prioritize energy-efficient infrastructure, lifecycle optimization, and compliance-driven maintenance frameworks.

Segment Analysis

By Data Center Type

Hyperscale data centers dominate the market with nearly 48% share. These facilities support global cloud platforms and AI workloads, requiring highly structured maintenance systems that include predictive analytics, automated fault detection, and real-time monitoring.

Enterprise data centers, however, are the fastest-growing segment. Businesses in BFSI, healthcare, manufacturing, and logistics are increasingly adopting hybrid IT models, requiring third-party maintenance and extended lifecycle support for cost efficiency and regulatory compliance.

By Component Type

Servers represent the largest component segment, accounting for more than half of total revenue. The increasing adoption of AI, virtualization, and high-performance computing has intensified server complexity and maintenance needs.

Networking equipment is the fastest-growing segment, driven by the transition to 400G and 800G network architectures and software-defined networking environments. These systems require specialized configuration management and continuous optimization to maintain performance at scale.

By Industry

IT and telecommunications lead the market, accounting for around 34% of total revenue. These sectors operate large-scale, highly complex infrastructure that requires continuous uptime and performance optimization.

Healthcare is the fastest-growing industry segment. The adoption of electronic health records, telemedicine, and AI-based diagnostics has significantly increased reliance on secure and high-availability data centers. Any downtime in healthcare IT systems can directly impact patient safety, making maintenance services critical.

Market Challenges

Despite strong growth, the market faces several constraints.

One major challenge is the high cost of specialized expertise. Maintaining AI-optimized servers, GPU clusters, and multi-vendor infrastructure requires certified engineers, which increases operational costs. For smaller enterprises, these costs can be prohibitive.

Another challenge is supply chain disruption for spare parts. Semiconductor shortages and long procurement cycles can delay repairs and increase downtime risk. As organizations extend hardware lifecycles beyond OEM support periods, dependency on third-party maintenance providers becomes more complex.

Opportunities in the Market

Healthcare digitalization presents one of the most significant opportunities. Hospitals and healthcare networks are rapidly adopting digital systems that require uninterrupted uptime. Regulatory requirements further mandate strict maintenance protocols and audit-ready infrastructure management.

Government and defense modernization programs also represent a major opportunity. National digital initiatives, smart infrastructure projects, and sovereign cloud deployments are increasing demand for secure and resilient data center maintenance services.

Competitive Landscape

The market is moderately consolidated, with key players including IBM, Dell Technologies, Hewlett Packard Enterprise, Cisco Systems, Vertiv, and Schneider Electric.

Competition is driven by predictive maintenance capabilities, AI-enabled monitoring platforms, and global service networks. Companies are increasingly investing in digital twin technology, remote diagnostics, and outcome-based service contracts.

Recent innovations include AI-powered predictive maintenance platforms and next-generation data center architectures designed for AI workloads, reflecting a shift toward automation and intelligence-driven operations.

Conclusion

The global data center support & maintenance services market is entering a high-growth phase, driven by AI adoption, hyperscale infrastructure expansion, and increasing global digitalization. As data becomes the foundation of economic activity, ensuring uptime, reliability, and performance of data centers will remain a critical priority for enterprises and governments alike.

Between 2026 and 2033, the market’s projected doubling in size reflects not just infrastructure expansion but also a fundamental shift toward intelligent, predictive, and automated maintenance ecosystems. Organizations that invest in advanced maintenance strategies will be best positioned to support the next generation of digital workloads in an increasingly connected world.