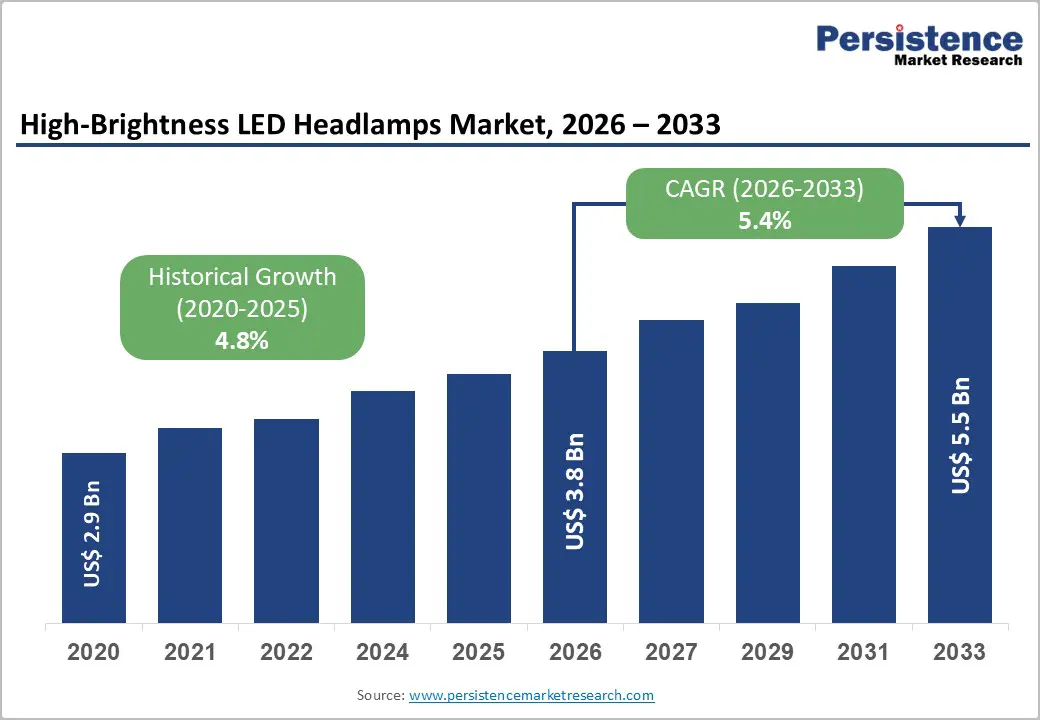

The global high-brightness light-emitting diodes (LED) headlamps market is undergoing a steady but structurally transformative growth phase, shaped by regulatory pressure, electrification of mobility, and rapid advances in adaptive lighting technologies. Valued at approximately US$3.8 billion in 2026, the market is projected to reach US$5.5 billion by 2033, expanding at a CAGR of 5.4% during the forecast period.

Unlike earlier generations of automotive lighting, which evolved primarily on cost and durability metrics, the current wave of innovation is being driven by safety compliance, software-defined lighting systems, and the integration of advanced driver assistance systems (ADAS). High-brightness LED headlamps have transitioned from premium optional features to baseline expectations in many vehicle categories, especially in developed markets.

Market Overview

High-brightness LED headlamps represent the most advanced form of automotive forward lighting currently in mass deployment. These systems deliver superior luminous efficiency, longer service life, and significantly improved beam control compared to halogen and HID alternatives.

Between 2020 and 2025, the market grew at a historical CAGR of 4.8%, primarily driven by early adoption in premium passenger vehicles. However, the next phase of growth is broader and more systemic. From 2026 onward, LED headlamp adoption is increasingly tied to global vehicle electrification and regulatory enforcement of safety lighting standards.

Key demand drivers include:

- Expansion of electric and hybrid vehicle production

- Mandatory adoption of energy-efficient lighting systems

- Rising consumer preference for adaptive driving safety features

- OEM integration of intelligent and pixel-based lighting systems

Key Market Highlights

Leading Region: Europe

Europe holds approximately 38% of global market share, making it the dominant region in LED headlamp technology adoption. The region benefits from:

- Strong presence of premium OEMs such as BMW, Mercedes-Benz, and Volkswagen

- Advanced Tier 1 suppliers including Valeo and Hella

- Strict UNECE lighting regulations enforcing high-performance standards

According to ACEA, the EU recorded around 10.5 million new car registrations in 2023, with LED headlamps widely standard across new vehicle platforms.

Fastest Growing Region: Asia Pacific

Asia Pacific is expected to grow at the fastest CAGR of 6.8%, led by China and India.

- China produces over 30 million vehicles annually, driving large-scale LED integration.

- India’s regulatory push for Automatic Headlamp On (AHO) in two-wheelers accelerates LED penetration.

- Electric two-wheeler adoption is rapidly expanding, supported by government subsidies and urban mobility shifts.

The region is also a global hub for LED component manufacturing, giving it a strong cost and supply chain advantage.

Dominant Segment: Passenger Cars

Passenger cars account for approximately 55% of total market share due to:

- High global production volumes (~67 million units annually)

- Rapid penetration of LED systems in new models

- Strong consumer preference for safety and aesthetic lighting upgrades

LED headlamps are now standard in most mid-to-high-end passenger vehicles, particularly in Europe, Japan, and North America.

Fastest Growing Technology: Adaptive Driving Beam (ADB)

ADB systems are reshaping automotive lighting architecture.

Key growth catalysts include:

- NHTSA approval of ADB technology in 2022 (U.S.)

- Up to 20% reduction in nighttime crash rates (IIHS studies)

- Increasing adoption of matrix and pixel LED systems in premium EV platforms

ADB enables dynamic beam shaping, eliminating glare while maximizing visibility, making it a critical feature in next-generation vehicles.

Market Dynamics

Drivers

- Stringent Global Lighting Safety Regulations

Regulatory frameworks such as:

- UNECE Regulation No. 112 and 123

- NHTSA adaptive beam approval (U.S.)

- EU General Safety Regulation (GSR 2019/2144)

are collectively pushing OEMs to adopt high-performance LED systems. These rules emphasize beam precision, energy efficiency, and nighttime visibility improvements.

Poor lighting is recognized as a contributing factor in nighttime road fatalities, reinforcing policy urgency for adoption.

- Electrification of Vehicles

The rise of electric vehicles (EVs) is a structural growth engine for LED headlamps.

- EVs prioritize energy efficiency at every component level

- LED headlamps consume up to 75% less energy than halogen systems

- Global EV sales exceeded 14 million units in 2023 (IEA)

Major EV manufacturers such as Tesla, BYD, and Rivian have standardized LED lighting across product lines, setting a global benchmark.

Restraints

- High Cost of Advanced Systems

Matrix LED and ADB systems significantly increase vehicle costs.

- Advanced systems may add US$300–US$800 per headlamp unit

- Limits adoption in low-cost vehicle segments

- Slows penetration in price-sensitive emerging markets

- Thermal Management Challenges

High-intensity LEDs generate heat that must be carefully managed.

According to the U.S. DOE:

- A 10°C rise in temperature can reduce LED lifespan by ~50%

- Poor thermal design leads to performance degradation and warranty risks

This remains a technical barrier for low-cost manufacturing environments.

Opportunities

- Regulatory Opening of ADB in North America

The NHTSA’s 2022 approval unlocks a major new market.

Benefits include:

- Strong demand from U.S. OEMs (GM, Ford, Toyota, BMW)

- Expansion of premium lighting features in mid-range vehicles

- Increased supplier contracts for pixel LED systems

- Electric Two-Wheeler Boom in Asia

The two-wheeler segment represents a massive volume opportunity.

- Over 300 million electric two-wheelers globally

- India alone recorded 800,000+ e2W sales in FY 2022–23

- LED headlamps increasingly standard for energy efficiency and branding

This segment offers high-volume, cost-optimized LED demand.

Segment Analysis

Product Type

Front LED headlamps dominate the market with 44% share, supported by:

- Broad OEM standardization

- Cost reductions from LED efficiency gains

- Replacement of halogen and HID systems

Technology

Standard LED systems lead with 46% share, driven by:

- Mature manufacturing ecosystem

- Long lifespan (25,000+ hours)

- High luminous efficiency (>200 lm/W in advanced designs)

However, matrix and ADB systems are growing fastest due to premium vehicle integration.

Application

OEM fitment accounts for 72% of total revenue, reflecting:

- Deep integration with vehicle electronics and ADAS systems

- High technical complexity of modern lighting systems

- Limited aftermarket substitution feasibility

Sales Channel

Dealerships dominate aftermarket distribution with 38% share, while online retail is rapidly growing due to:

- Expanding e-commerce adoption

- Rising consumer awareness of LED upgrades

- Competitive pricing for replacement kits

Regional Analysis

North America

The U.S. market is shaped by:

- Large vehicle base (~290 million registered vehicles)

- IIHS headlamp safety ratings influencing OEM design

- Regulatory shift enabling ADB systems

Canada follows similar adoption patterns due to regulatory alignment.

Europe

Europe remains the global innovation hub for LED headlamps.

Key factors:

- Strong premium OEM presence

- Advanced regulatory ecosystem (UNECE standards)

- High penetration of adaptive lighting systems

Germany leads R&D activity with major suppliers like Hella and OSRAM.

Asia Pacific

Asia Pacific is the most dynamic growth region.

- China dominates production and consumption

- Japan leads in Tier 1 supplier innovation (Koito, Stanley Electric)

- India is rapidly expanding LED adoption in two-wheelers

Southeast Asia also shows strong growth potential due to urbanization and vehicle expansion.

Competitive Landscape

The market is moderately consolidated, led by Tier 1 suppliers including:

- Koito Manufacturing Co., Ltd.

- Valeo S.A.

- Hella GmbH & Co. KGaA

- Stanley Electric Co., Ltd.

- ZKW Group GmbH

Key component suppliers:

- OSRAM GmbH

- Lumileds Holding B.V.

- Nichia Corporation

- Philips N.V.

Competition is increasingly defined by:

- Pixel density and beam control precision

- Software-driven adaptive lighting algorithms

- Thermal efficiency and durability

- Integration with ADAS and autonomous systems

Recent Developments

- Feb 2025: Koito announced mass production of 1,024-pixel matrix LED headlamp modules for premium OEMs

- Oct 2024: Valeo launched SCALA® 3 LiDAR-integrated headlamp system for autonomous driving platforms

- Apr 2024: OSRAM introduced SYNIOS® P2720 LED series with improved thermal stability and efficiency

Conclusion

The high-brightness LED headlamps market is evolving from a component-driven lighting segment into a software-defined automotive safety ecosystem. Growth is no longer solely dependent on hardware upgrades but increasingly tied to intelligent beam control, regulatory evolution, and electrified mobility platforms.

Between 2026 and 2033, the market’s expansion will be shaped by three core forces:

- Global EV adoption and efficiency-driven design requirements

- Regulatory endorsement of adaptive lighting systems

- Rapid penetration of LED systems in mass-market vehicles and two-wheelers

As vehicle lighting becomes more intelligent and integrated, LED headlamps will move from being a visibility tool to a critical safety and perception-enhancing technology across global mobility systems.