Robotic Process Automation Market Overview

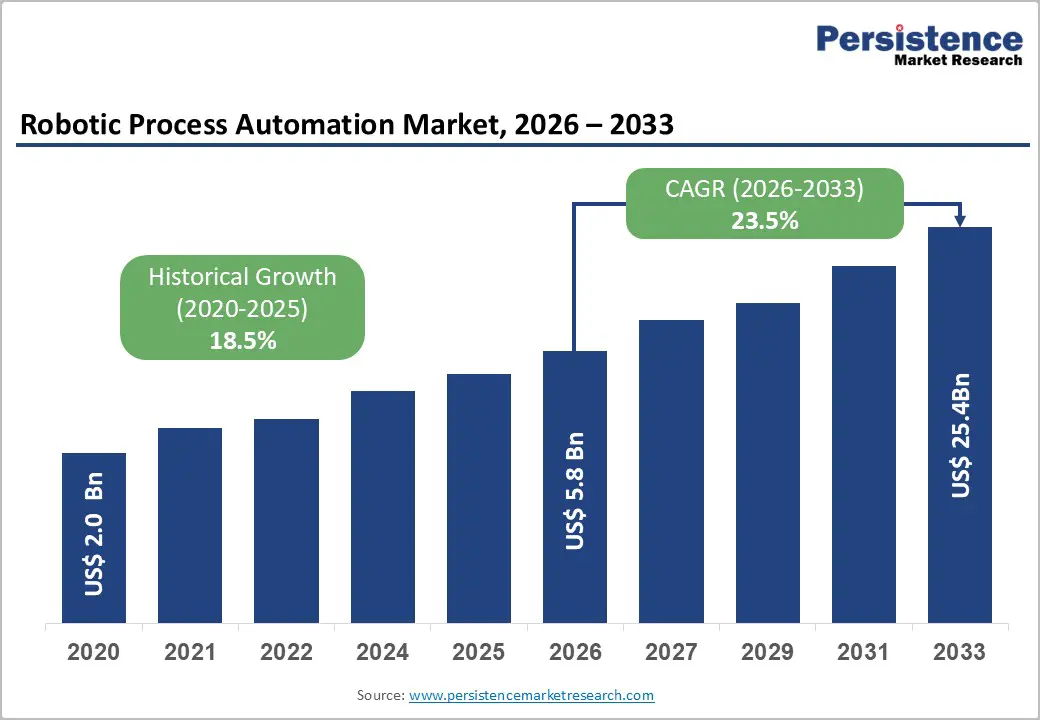

The global robotic process automation (RPA) market size is expected to reach US$ 5.8 billion in 2026 and is projected to expand significantly to US$ 25.4 billion by 2033, registering a CAGR of 23.5% between 2026 and 2033. The rapid adoption of enterprise automation technologies, increasing demand for operational efficiency, and integration of artificial intelligence (AI) with automation platforms are transforming how organizations manage repetitive and rule-based business processes.

Enterprises across industries are increasingly deploying RPA solutions to automate high-volume workflows, reduce operational costs, improve accuracy, and accelerate digital transformation initiatives. Traditional automation focused primarily on structured data entry and repetitive tasks; however, modern RPA platforms integrated with AI, machine learning, natural language processing, and computer vision are evolving into intelligent automation ecosystems capable of managing complex decision-based processes.

The growing adoption of cloud-based automation platforms, low-code/no-code development environments, and AI-powered software bots is further expanding RPA accessibility among large enterprises, mid-sized businesses, and small organizations. As companies continue to prioritize scalability, productivity, and customer experience improvement, robotic process automation is becoming a strategic technology investment across multiple sectors.

Key Market Highlights

- Market Size (2026): US$ 5.8 billion

- Forecast Value (2033): US$ 25.4 billion

- Growth Rate (2026–2033): CAGR of 23.5%

- Leading Region: North America with approximately 38% market share

- Fastest-Growing Region: Europe supported by regulatory-driven automation adoption

- Leading Industry: BFSI accounting for around 27% market share

- Fastest-Growing Industry: Healthcare & Pharmaceuticals

- Dominant Component: Software segment with nearly 68% share

Major Factors Driving Robotic Process Automation Market Growth

Enterprise Digital Transformation Accelerating Automation Adoption

Organizations worldwide are undergoing large-scale digital transformation programs to improve productivity, reduce operational expenses, and enhance business agility. The increasing complexity of enterprise operations, growing transaction volumes, and demand for faster service delivery are creating strong demand for RPA solutions.

Businesses are increasingly automating repetitive processes such as invoice processing, employee onboarding, customer verification, financial reconciliation, inventory management, and compliance reporting. Unlike traditional automation methods requiring significant system modifications, RPA enables organizations to automate existing workflows without replacing legacy applications.

The rapid expansion of digital commerce, online banking, and cloud-based enterprise systems is generating massive volumes of structured and semi-structured data. Processing these increasing data volumes manually is becoming inefficient, encouraging organizations to adopt software robots for faster and more accurate execution.

The global B2B e-commerce ecosystem is expected to generate trillions of dollars in transaction value, creating significant automation opportunities across procurement, supply chain management, logistics documentation, and payment processing workflows.

AI Integration Transforming Traditional RPA into Intelligent Automation

Artificial intelligence integration represents one of the most significant trends shaping the robotic process automation market. Traditional RPA systems were primarily rule-based, performing predefined tasks according to fixed instructions. However, AI-powered RPA platforms are enabling intelligent decision-making, predictive analytics, and adaptive workflow management.

The combination of machine learning, natural language processing, and computer vision allows automation systems to process unstructured information such as emails, documents, images, and customer interactions.

AI-enhanced RPA solutions are increasingly being deployed for:

- Automated customer service operations

- Intelligent document processing

- Fraud detection

- Claims processing

- Compliance monitoring

- Predictive workflow optimization

In January 2023, NICE introduced AI-powered enhancements to its RPA portfolio through the NEVA Discover platform, enabling organizations to identify automation opportunities using machine learning-based process analytics.

The industry is also moving toward agentic automation, where AI-powered bots can independently analyze situations, make decisions, and execute business processes without continuous human supervision.

BFSI Sector Dominates Robotic Process Automation Adoption

The Banking, Financial Services, and Insurance (BFSI) sector represents the largest end-use industry, accounting for approximately 27% of the robotic process automation market.

Financial institutions manage enormous volumes of repetitive and compliance-heavy processes, making them ideal candidates for automation. Banks and insurance companies are implementing RPA solutions across:

- Know Your Customer (KYC) verification

- Fraud monitoring

- Loan processing

- Regulatory reporting

- Account reconciliation

- Customer onboarding

- Claims management

The rapid expansion of digital banking services has further increased operational complexity. Financial institutions must process millions of transactions daily while maintaining strict regulatory compliance, creating strong demand for automated workflows.

India’s BFSI sector, for example, has experienced significant expansion in market capitalization and digital adoption, resulting in increased demand for automation solutions across banking, insurance, and investment management operations.

European financial institutions are also investing heavily in RPA to improve operational efficiency, reduce processing times, and manage regulatory requirements.

Healthcare and Pharmaceutical Sector Emerging as High-Growth Opportunity

Healthcare and pharmaceutical companies represent the fastest-growing application area for robotic process automation due to increasing administrative complexity, regulatory requirements, and demand for operational efficiency.

Healthcare organizations are deploying RPA for:

- Patient record management

- Insurance claims processing

- Appointment scheduling

- Billing automation

- Clinical documentation

- Pharmaceutical supply chain management

- Regulatory submissions

The healthcare industry faces growing pressure to control costs while improving service quality. RPA provides a cost-effective solution by automating repetitive administrative processes without requiring complete replacement of existing healthcare IT systems.

Pharmaceutical companies are also adopting automation for compliance documentation, clinical trial management, inventory monitoring, and regulatory reporting.

Market Restraints: Legacy Infrastructure and Security Challenges

Despite strong growth opportunities, several challenges may limit robotic process automation adoption.

Legacy System Integration Complexity

Many large organizations continue to operate on outdated IT infrastructure, including legacy ERP platforms and mainframe systems. Integrating modern RPA solutions with these systems can require significant customization, increasing implementation costs and deployment timelines.

Financial institutions and government organizations often face additional complexity due to decades-old applications with limited API compatibility.

Other challenges include:

- Process standardization requirements

- Employee resistance to automation

- Bot maintenance requirements

- Lack of internal automation expertise

Organizations must develop strong governance frameworks and automation strategies to achieve long-term benefits.

Data Security and Regulatory Compliance Concerns

RPA systems frequently interact with sensitive financial, healthcare, and customer information, creating cybersecurity concerns.

Organizations must ensure:

- Secure bot credential management

- Data privacy compliance

- Access control mechanisms

- Regulatory reporting accuracy

Different regions follow varying data protection requirements, including GDPR in Europe, HIPAA regulations in the United States, and data localization policies in several Asian countries.

These regulatory differences increase complexity for multinational enterprises implementing global RPA strategies.

Component Analysis: Software Segment Leads the Market

The software segment dominates the robotic process automation market with approximately 68% share.

RPA software platforms include:

- Bot development tools

- Process discovery platforms

- Workflow orchestration systems

- Analytics dashboards

- AI automation capabilities

Leading vendors such as UiPath, Automation Anywhere, Microsoft, and SS&C Blue Prism are continuously enhancing their platforms with cloud capabilities and AI-powered automation features.

The growing adoption of subscription-based SaaS models is further supporting software segment growth by reducing upfront investment requirements.

Meanwhile, the services segment is expected to witness strong expansion as enterprises require consulting, implementation, training, and managed automation services.

Deployment Model Analysis: Cloud-Based RPA Gains Momentum

Cloud deployment accounts for the largest share of the robotic process automation market due to advantages including:

- Lower infrastructure costs

- Faster implementation

- Easy scalability

- Automatic software updates

- Integration with enterprise cloud platforms

Cloud-based RPA solutions align with enterprise migration toward SaaS-based business applications and cloud infrastructure.

Platforms such as Microsoft Power Automate benefit from integration with Microsoft 365 and Azure ecosystems, enabling organizations to deploy automation capabilities more easily.

However, on-premises deployment continues to grow among highly regulated industries requiring greater control over sensitive data.

Regional Market Insights

North America Leads Global RPA Adoption

North America holds the largest market share at approximately 38%, supported by a mature enterprise automation ecosystem and strong presence of leading RPA providers.

The United States represents the largest contributor due to:

- High enterprise automation investment

- Presence of major RPA companies

- Strong technology infrastructure

- Advanced BFSI and manufacturing sectors

Companies including UiPath, Automation Anywhere, Pegasystems, and Microsoft have strengthened the region’s leadership position.

Industries such as financial services, healthcare, retail, and manufacturing are major adopters of automation technologies.

Europe Experiences Strong Regulatory-Driven Growth

Europe accounts for nearly 27% of the global robotic process automation market.

Automation adoption in Europe is driven by:

- Strict compliance requirements

- Digital transformation initiatives

- Manufacturing modernization

- Banking sector efficiency programs

Germany remains one of the leading European markets due to its advanced industrial manufacturing ecosystem and strong financial services sector.

Organizations across Europe are adopting RPA to improve productivity while meeting increasingly complex regulatory requirements.

Asia Pacific Offers Significant Growth Potential

Asia Pacific represents approximately 24% of the global RPA market and is expected to experience strong growth due to rapid digitalization across emerging economies.

Countries including China, India, Japan, and South Korea are investing heavily in enterprise automation.

India represents one of the fastest-growing RPA markets due to:

- Expansion of digital banking

- Growth of e-commerce

- Logistics modernization

- Increasing adoption among enterprises

Industries beyond BFSI, including manufacturing, retail, and logistics, are increasingly implementing RPA solutions.

Competitive Landscape

The global robotic process automation market is moderately consolidated, with leading technology providers competing through AI integration, cloud capabilities, platform scalability, and industry-specific solutions.

Major market players include:

- UiPath Inc.

- Automation Anywhere Inc.

- SS&C Blue Prism Limited

- Microsoft Corporation

- NICE Ltd.

- Pegasystems Inc.

- SAP SE

- WorkFusion Inc.

- EdgeVerve Systems Limited

- Tungsten Automation Corporation

- BlackLine Inc.

- Uniphore

Companies are increasingly focusing on AI-powered automation, intelligent workflow orchestration, and agentic automation capabilities.

In 2025, UiPath, Automation Anywhere, and SS&C Blue Prism were recognized as Leaders in Gartner’s Magic Quadrant for Robotic Process Automation, highlighting their strong market positioning.

Future Outlook of the Robotic Process Automation Market

The robotic process automation market is entering a new phase driven by artificial intelligence, cloud computing, and enterprise automation strategies. Future growth will increasingly depend on intelligent automation capabilities that combine RPA with AI agents, analytics, and decision-making technologies.

The expansion of low-code/no-code automation platforms will enable more businesses, including small and medium enterprises, to adopt RPA without requiring specialized programming expertise.

Healthcare, financial services, logistics, manufacturing, and retail are expected to remain key growth sectors as organizations seek greater operational efficiency and digital resilience.

With enterprises worldwide prioritizing automation-led transformation, the global robotic process automation market is projected to maintain strong double-digit growth through 2033, creating significant opportunities for technology providers and organizations adopting intelligent automation solutions.