The global simulators market is witnessing significant expansion as organizations across defence, aviation, healthcare, automotive, education, and industrial sectors increasingly adopt simulation technologies to improve training efficiency, reduce operational risks, and enhance decision-making capabilities. Simulators provide realistic virtual environments that replicate real-world systems, allowing users to practice complex operations without the safety concerns and costs associated with physical training. The growing adoption of advanced technologies such as artificial intelligence (AI), virtual reality (VR), augmented reality (AR), digital twins, and real-time data analytics is transforming simulation platforms into highly immersive and intelligent training solutions. From flight simulators used for pilot certification to medical simulators supporting surgical education, simulation-based learning has become an essential component across multiple industries.

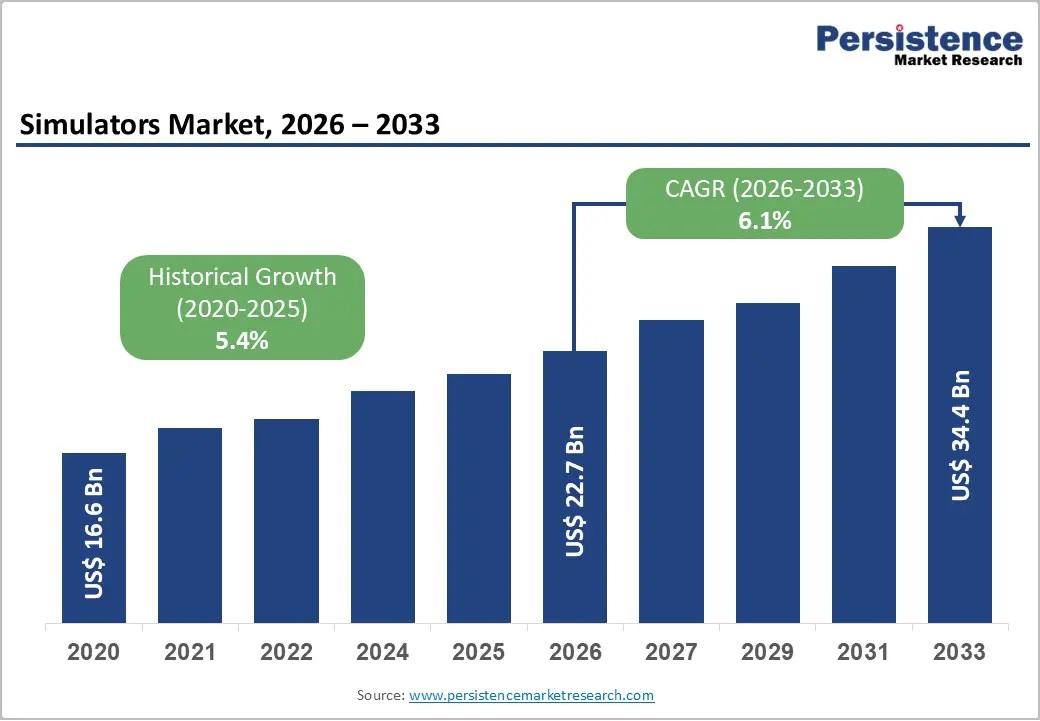

The global simulators market size is expected to reach approximately US$22.7 billion in 2026 and is projected to grow to US$34.4 billion by 2033, expanding at a CAGR of 6.1% between 2026 and 2033. The market growth is primarily driven by increasing defence modernization budgets, mandatory flight crew training requirements in the aviation sector, and rising adoption of simulation-based training across healthcare, automotive, and industrial manufacturing industries. Among market segments, flight simulators represent a leading segment due to strict aviation safety regulations, increasing air passenger traffic, and continuous demand for trained pilots. Geographically, North America dominates the global simulators market because of strong defence spending, the presence of leading simulation technology providers, advanced aerospace infrastructure, and early adoption of innovative training solutions across military and commercial applications.

𝐅𝐑𝐄𝐄 𝐒𝐚𝐦𝐩𝐥𝐞 & 𝐄𝐱𝐩𝐥𝐨𝐫𝐞 𝐭𝐡𝐞 𝐋𝐚𝐭𝐞𝐬𝐭 𝐌𝐚𝐫𝐤𝐞𝐭 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐬:https://www.persistencemarketresearch.com/samples/31052

Key Highlights from the Report

• The global simulators market is forecast to expand from US$22.7 billion in 2026 to US$34.4 billion by 2033.

• Rising defence modernization programs are accelerating demand for advanced military simulation systems.

• Aviation training requirements and pilot shortages are driving increased adoption of flight simulators.

• Healthcare simulation technologies are gaining momentum for improving medical education and clinical training.

• North America leads the market due to strong aerospace, defence, and technology ecosystems.

• Artificial intelligence, virtual reality, and digital twin technologies are shaping next-generation simulators.

Market Segmentation

The simulators market can be segmented based on simulator type, technology, application, and end-user industry. Based on simulator type, the market includes flight simulators, vehicle simulators, maritime simulators, medical simulators, gaming simulators, industrial simulators, and other specialized simulation systems. Flight simulators hold a significant market share due to their critical role in pilot training, aircraft operation testing, and aviation safety compliance. Full-flight simulators, flight training devices, and cockpit simulation systems are widely used by commercial airlines, military organizations, and aviation training centers to provide realistic operational experiences.

Vehicle simulators represent another important segment, covering automotive driving simulators, military vehicle simulators, and autonomous vehicle testing platforms. Automotive manufacturers increasingly use simulation technologies to test vehicle performance, driver behavior, and advanced driver assistance systems (ADAS) before physical production. The growing development of electric vehicles and autonomous driving technologies is further increasing demand for advanced automotive simulation solutions.

Medical simulators are gaining rapid adoption as healthcare institutions focus on improving clinical skills, reducing medical errors, and enhancing patient safety. These systems provide realistic environments for practicing surgical procedures, emergency response, anesthesia techniques, and diagnostic skills. Simulation-based healthcare training enables medical professionals and students to gain practical experience without involving actual patients, making it a valuable tool in modern medical education.

Based on technology, the simulators market includes virtual reality-based simulators, augmented reality-based systems, mixed reality platforms, and traditional simulation technologies. VR and AR-based simulators are experiencing strong growth because they provide immersive learning environments, improved user engagement, and cost-effective training solutions. Digital twin technology is also emerging as a major innovation, allowing organizations to create virtual replicas of physical systems for monitoring, testing, and optimization.

By end user, the market serves defence organizations, aviation companies, healthcare institutions, automotive manufacturers, educational institutions, energy companies, and industrial enterprises. Defence and aerospace sectors remain major contributors due to continuous investments in military readiness and operational training. However, healthcare, automotive, and industrial applications are expected to experience strong growth as businesses increasingly prioritize safe and efficient workforce training.

Regional Insights

North America represents the largest regional market for simulators due to significant investments in defence technology, aerospace development, and advanced training infrastructure. The United States plays a major role in regional growth through extensive military simulation programs, commercial aviation training requirements, and strong demand for healthcare simulation solutions. The presence of major simulation technology providers and research institutions further strengthens North America's leadership position.

Europe holds a substantial share of the global simulators market, supported by strong aerospace manufacturing capabilities, defence modernization initiatives, and increasing adoption of digital training solutions. Countries such as Germany, France, the United Kingdom, and Italy are investing heavily in simulation technologies for aviation, automotive engineering, industrial operations, and defence applications. European industries are also adopting simulation platforms to improve manufacturing efficiency and support Industry 4.0 transformation.

Asia-Pacific is expected to witness significant growth during the forecast period due to expanding aviation industries, rising defence expenditures, increasing healthcare investments, and rapid industrial development. Countries including China, India, Japan, and South Korea are investing in advanced simulation systems for pilot training, military applications, automotive development, and technical education. The region’s growing aviation passenger traffic and increasing number of commercial aircraft deliveries are creating strong demand for flight simulation technologies.

Latin America and the Middle East & Africa are also experiencing gradual market expansion as governments and industries invest in modernization programs. Defence training requirements, aviation infrastructure development, healthcare improvements, and industrial automation initiatives are supporting the adoption of simulators across these regions.

Market Drivers

The primary factor driving the simulators market is the increasing need for safe, cost-effective, and realistic training environments across multiple industries. In aviation, strict regulatory requirements and the rising complexity of aircraft systems are increasing demand for advanced flight simulators that enable pilots to complete training hours efficiently. Defence organizations are investing in military simulators to improve combat preparedness while reducing the expenses and risks associated with live training exercises. Healthcare institutions are adopting medical simulation systems to enhance clinical education and improve patient safety. Additionally, the integration of artificial intelligence, virtual reality, augmented reality, and advanced analytics is improving simulator capabilities by enabling more realistic scenarios, adaptive learning experiences, and real-time performance assessment.

Market Restraints

Despite strong growth potential, the simulators market faces several challenges, including high initial investment costs, complex development requirements, and expensive maintenance processes. Advanced simulation systems require significant capital for hardware, software development, infrastructure setup, and regular upgrades. Small organizations and educational institutions may face difficulties adopting sophisticated simulators due to budget limitations. Additionally, developing highly realistic simulation environments requires specialized expertise, advanced computing capabilities, and continuous technological improvements. Compatibility issues between simulation platforms and existing operational systems can also create implementation challenges for end users.

Market Opportunities

The simulators market offers significant opportunities through the increasing adoption of immersive technologies, cloud-based simulation platforms, and artificial intelligence-driven training solutions. The growing demand for remote learning and virtual training environments is creating new opportunities for cloud-enabled simulators that allow users to access training programs from different locations. The expansion of autonomous vehicles, smart manufacturing, and digital twin applications is expected to increase demand for simulation technologies across automotive and industrial sectors. Furthermore, emerging economies are investing in aviation infrastructure, healthcare education, and defence modernization, creating new growth opportunities for simulator manufacturers.

Company Insights

• CAE Inc.

• L3Harris Technologies

• Thales Group

• RTX Corporation

• Lockheed Martin Corporation

• Boeing Company

• Dassault Aviation

• FlightSafety International

Recent Developments

Leading simulator manufacturers are increasingly integrating artificial intelligence, cloud computing, and extended reality technologies into simulation platforms to deliver more adaptive and realistic training experiences.

Companies are also expanding partnerships with aviation, defence, healthcare, and industrial organizations to develop customized simulation solutions that support next-generation workforce training and operational efficiency.

Conclusion

The global simulators market is expected to experience steady growth through 2033 as industries continue adopting simulation technologies to improve safety, reduce training costs, and enhance operational performance. Increasing defence modernization spending, aviation training requirements, healthcare simulation adoption, and industrial digital transformation are creating strong demand for advanced simulation platforms. Although high implementation costs and technological complexity remain challenges, advancements in artificial intelligence, virtual reality, augmented reality, and digital twin technologies are expected to unlock new opportunities. With continued innovation and expanding applications across diverse industries, the simulators market will remain a critical component of future training, testing, and operational development ecosystems.