Introduction: The Shift from Silicon to GaN-Powered Charging

The global charging ecosystem is undergoing a significant transformation as consumers, enterprises, and industries demand faster, smaller, and more energy-efficient power solutions. Traditional silicon-based chargers, which have dominated the market for decades, are increasingly being challenged by next-generation Gallium Nitride (GaN) technology.

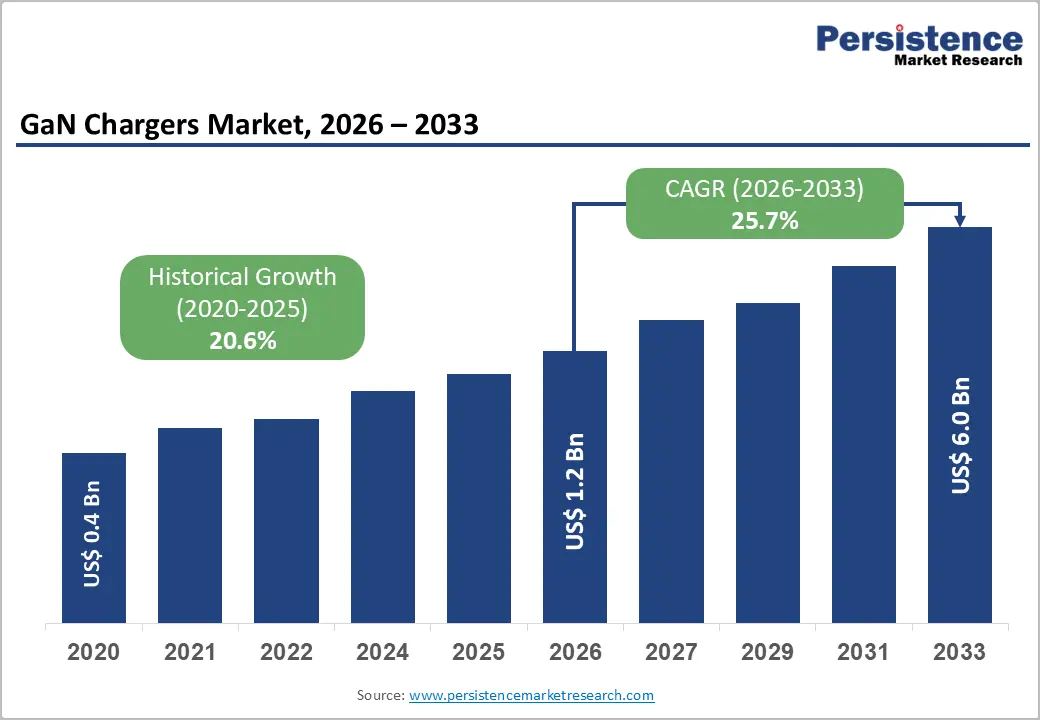

The global GaN chargers market size is projected to reach US$1.2 billion in 2026 and is expected to expand to US$6.0 billion by 2033, registering an impressive CAGR of 25.7% between 2026 and 2033.

This rapid growth reflects the growing need for compact high-power charging solutions across smartphones, laptops, tablets, gaming devices, electric vehicles, industrial equipment, and data center infrastructure.

Gallium Nitride offers major performance advantages compared with conventional silicon semiconductors, including up to 40% smaller charger designs, three times higher switching frequencies, and efficiency levels exceeding 95% at full load. These characteristics are accelerating the transition toward GaN-powered charging architectures across consumer and commercial applications.

As device ecosystems become increasingly interconnected and power-hungry, GaN chargers are emerging as a critical technology enabling the next generation of efficient power delivery.

GaN Chargers Market Growth Drivers

- Rising Demand for Multi-Device Charging Ecosystems

Modern consumers are managing an expanding number of connected devices, including smartphones, laptops, tablets, smartwatches, wireless earbuds, gaming consoles, and smart home devices. This rapid growth in device ownership has created strong demand for compact chargers capable of powering multiple devices simultaneously.

According to Ericsson’s Mobility Report, global smartphone subscriptions are expected to reach approximately 7.7 billion by 2028, creating a massive addressable market for advanced charging accessories.

Unlike traditional silicon chargers, GaN chargers can deliver higher power output while maintaining smaller footprints and lower heat generation. This makes them ideal for consumers seeking travel-friendly and multi-port charging solutions.

USB Power Delivery (USB-PD) technology has further strengthened GaN adoption by enabling higher charging speeds and universal compatibility across different device categories. USB-PD 3.1 supports power delivery up to 240W, allowing a single GaN charger to replace multiple traditional adapters.

- Regulatory Push Toward Energy Efficiency and Universal Chargers

Government regulations worldwide are becoming a major catalyst for GaN charger adoption.

The European Union’s Common Charger Directive (2022/2380/EU) represents one of the strongest market drivers. The regulation requires USB-C charging standardization for many consumer electronics products sold in Europe, triggering a large-scale replacement cycle for outdated chargers.

This transition is benefiting GaN charger manufacturers because consumers and businesses are increasingly choosing compact, high-efficiency USB-C Power Delivery adapters rather than replacing older silicon chargers with similar alternatives.

Energy efficiency regulations are also supporting market growth. The U.S. Department of Energy’s external power supply efficiency standards require improved energy performance from charging devices, pushing manufacturers toward advanced semiconductor technologies such as GaN.

China’s evolving charger certification standards and USB-PD adoption initiatives are further strengthening GaN penetration in the world’s largest electronics manufacturing ecosystem.

Technological Advantages Driving GaN Adoption

GaN technology provides several advantages that position it ahead of traditional silicon-based solutions:

Higher Power Density

GaN semiconductors operate at higher switching frequencies, allowing manufacturers to reduce transformer and passive component sizes. The result is significantly smaller chargers without sacrificing performance.

Improved Energy Efficiency

GaN chargers generate less heat and achieve efficiency ratings above 95%, reducing energy loss during charging cycles.

Higher Charging Capacity

Advanced GaN solutions support high-wattage charging applications, including laptops, professional workstations, gaming devices, and future electric vehicle charging systems.

Better Thermal Management

Lower heat generation improves reliability and extends product lifespan, especially in high-power applications.

These benefits are encouraging both consumer electronics companies and semiconductor manufacturers to invest heavily in GaN-based power solutions.

Market Challenges: Factors Limiting GaN Charger Adoption

Higher Manufacturing Costs

Despite strong advantages, GaN chargers continue to face cost-related challenges.

GaN semiconductor production requires specialized manufacturing processes and more expensive materials compared with silicon alternatives. As a result, GaN chargers generally carry a 40% premium compared with traditional chargers offering similar power ratings.

This price gap remains a barrier in highly price-sensitive markets where consumers prioritize affordability over advanced charging performance.

However, increasing production volumes, improvements in wafer manufacturing, and technological advancements are expected to gradually reduce costs over the forecast period.

Supply Chain Risks for Gallium and GaN Wafers

The GaN semiconductor supply chain remains concentrated among a limited number of manufacturers.

Gallium, a critical material used in GaN production, has significant supply concentration, with China accounting for a substantial portion of global production. Export restrictions introduced by China in 2023 on gallium and germanium highlighted potential vulnerabilities in semiconductor material supply chains.

The European Commission has identified gallium as a strategic raw material under its Critical Raw Materials Act, emphasizing the importance of securing stable supply chains.

Future market expansion will depend on improving wafer availability, increasing manufacturing capacity, and diversifying global supply sources.

Emerging Opportunities in the GaN Chargers Market

Electric Vehicle Charging Applications

The electric vehicle revolution represents one of the most promising growth opportunities for GaN technology.

The International Energy Agency (IEA) reported that global electric vehicle sales exceeded 14 million units in 2023, with the global EV fleet approaching 40 million vehicles.

Electric vehicle manufacturers are increasingly exploring GaN-based solutions for onboard chargers (OBCs) because they enable:

- Higher power density

- Reduced system weight

- Improved charging efficiency

- Smaller vehicle power electronics systems

Companies such as Navitas Semiconductor and GaN Systems are developing automotive-grade GaN solutions certified under AEC-Q101 standards for EV applications.

As automakers focus on improving driving range and reducing vehicle weight, GaN technology is expected to become increasingly important in future EV charging architectures.

GaN Adoption in Data Centers and Industrial Power Systems

Artificial intelligence, cloud computing, and digital transformation are driving unprecedented demand for data center infrastructure.

The U.S. Department of Energy estimates that American data centers consumed nearly 200 billion kWh of electricity in 2023, making power efficiency a critical operational priority.

GaN-based power supplies can deliver efficiency levels approaching 98%, compared with approximately 94% for advanced silicon-based solutions.

This efficiency improvement can significantly reduce:

- Electricity costs

- Cooling requirements

- Infrastructure footprint

Companies including Navitas Semiconductor and Innoscience Technology are expanding GaN solutions for server power supplies, telecom infrastructure, and industrial applications.

Segment Analysis: Where Is the Market Growing Fastest?

Wall Chargers Lead Product Category

Wall chargers represent the dominant product segment, accounting for approximately 46% of total GaN charger market revenue.

The popularity of wall chargers is driven by:

- Growing smartphone and laptop adoption

- USB-C standardization

- Demand for compact travel chargers

- Replacement of traditional bulky adapters

Leading products from companies such as Anker, Belkin, Baseus, and UGREEN demonstrate strong consumer demand for premium GaN wall chargers.

Wired Chargers Maintain Market Leadership

Wired GaN chargers dominate the charging type segment, representing approximately 71% market share.

Although wireless charging technologies such as Qi2 and MagSafe are expanding, wired charging maintains advantages in:

- Charging speed

- Cost efficiency

- Energy transfer reliability

USB-PD-enabled wired GaN chargers remain the preferred solution for high-power applications.

Multi-Port Chargers Gain Momentum

Multi-port GaN chargers account for approximately 44% revenue share as consumers increasingly seek single charging solutions for multiple devices.

GaN technology enables manufacturers to provide multiple high-output ports while maintaining compact designs and preventing excessive heat generation.

This advantage is particularly valuable for professionals, travelers, and technology enthusiasts managing multiple devices.

30W–65W Chargers Dominate Power Output Segment

The 30W–65W category leads the power output segment with around 38% market share.

This range perfectly matches the requirements of:

- Premium smartphones

- Tablets

- Ultrabooks

- MacBook Air devices

- USB-C laptops

As more devices transition to USB-C charging, this segment is expected to maintain strong demand.

Regional Analysis: Asia Pacific Leads Global Market Growth

Asia Pacific Market Leadership

Asia Pacific currently dominates the global GaN chargers market with approximately 40% share.

The region’s leadership is supported by:

- Large-scale electronics manufacturing

- Strong semiconductor supply chains

- Major charger brands

- Rapid smartphone adoption

China remains the largest contributor due to its advanced GaN wafer manufacturing ecosystem and presence of leading companies such as:

- Innoscience Technology

- Xiaomi

- Baseus

- UGREEN

Europe: Fastest Growing Regional Market

Europe is expected to record the fastest growth, with a projected CAGR of approximately 30%.

The primary growth catalyst is the EU Common Charger Directive, which is accelerating consumer migration toward USB-C and high-efficiency charging solutions.

Countries including Germany, the U.K., and France are witnessing increasing demand for premium GaN chargers across consumer electronics and automotive applications.

North America Market Outlook

North America remains a major technology-driven market due to:

- High smartphone penetration

- Strong laptop adoption

- Enterprise IT demand

- Energy efficiency regulations

The U.S. market benefits from widespread USB-C adoption and growing demand for high-power charging accessories.

Competitive Landscape: Companies Shaping the GaN Charger Industry

The GaN chargers market features competition across semiconductor manufacturers and consumer electronics brands.

Leading companies include:

- Anker Innovations Technology Co., Ltd.

- Baseus

- UGREEN Group Limited

- Belkin International

- Zendure

- AUKEY

- RAVPower

- Spigen

- Navitas Semiconductor

- GaN Systems

- Innoscience Technology

- Infineon Technologies

- STMicroelectronics

- Xiaomi Corporation

Consumer brands compete through product design, charging speed, portability, and ecosystem compatibility, while semiconductor companies focus on improving GaN efficiency, reducing costs, and expanding application areas.

Recent Industry Developments

Anker Launches 240W GaN Charging Station

In January 2025, Anker introduced its Prime 240W GaN Desktop Charging Station featuring six ports and smart power monitoring capabilities for professionals managing multiple high-power devices.

Navitas Expands High-Efficiency GaN IC Portfolio

In October 2024, Navitas Semiconductor announced mass production of its third-generation GaNFast NV6177 power IC, delivering up to 98% efficiency for 65W–140W charging applications.

Innoscience Advances GaN Wafer Manufacturing

In April 2024, Innoscience began commercial shipments of 8-inch GaN-on-Silicon wafers, helping reduce production costs and improve scalability.

Future Outlook: GaN Chargers Moving Beyond Consumer Electronics

The GaN chargers market is entering a period of accelerated expansion as industries prioritize efficiency, miniaturization, and high-power performance.

While smartphones and laptops remain the primary adoption drivers, future growth will increasingly come from:

- Electric vehicle charging systems

- Data center power infrastructure

- Industrial automation

- Renewable energy systems

- High-performance computing

As manufacturing costs decline and supply chains mature, GaN technology is expected to move from premium charging accessories into mainstream power electronics applications.

Conclusion

The global GaN chargers market is positioned for exceptional growth, expanding from US$1.2 billion in 2026 to US$6.0 billion by 2033.

The combination of faster charging speeds, smaller designs, improved efficiency, regulatory support, and growing demand for sustainable electronics is transforming GaN into one of the most important semiconductor innovations in modern power management.

As consumer expectations evolve and industries demand higher energy efficiency, GaN chargers will play a central role in shaping the future of global charging infrastructure.