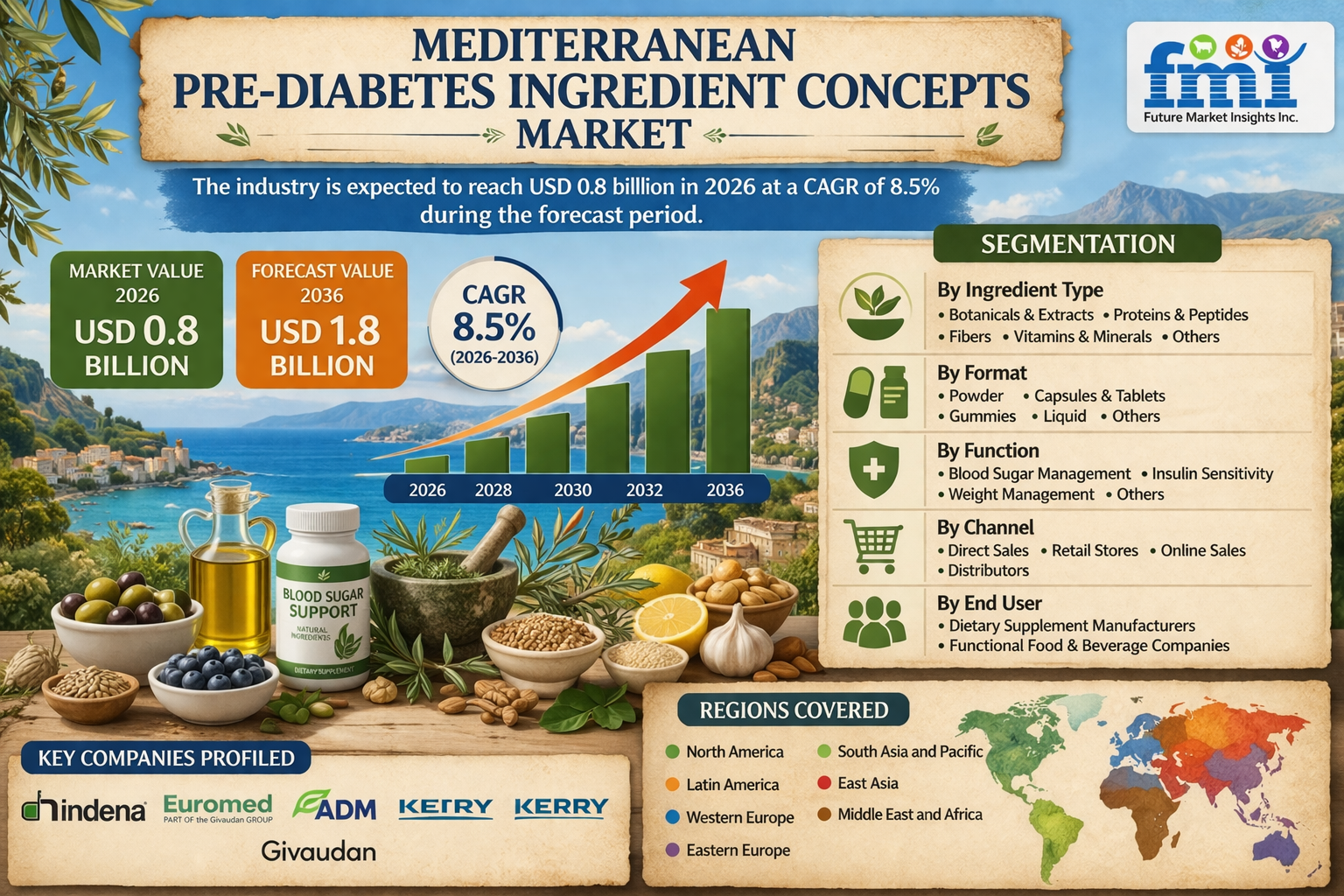

NEWARK, DELAWARE | April 2, 2026 — The global Mediterranean pre-diabetes ingredient concepts market is undergoing a rigorous evolution, maturing from traditional dietary interest into a data-driven nutraceutical powerhouse. Valued at USD 700 million in 2025, the market is projected to grow to USD 800 million in 2026. According to the latest strategic analysis by Future Market Insights (FMI), the sector is set to expand at an 8.5% CAGR, reaching a total valuation of USD 1,800 million by 2036.

The market’s expansion is driven by a "validation mandate." Formulators at mid-tier supplement brands are facing intense pressure from major retail buyers to provide clinical data for blood sugar claims. As procurement departments increasingly reject traditional botanical blends lacking standardized active profiles, the transition toward characterized nutraceutical ingredients has become the baseline for securing shelf space in premium metabolic health aisles.

Key Market Insights & Segment Performance

Olive polyphenols and versatile powder blends currently dominate the landscape, with dietary supplements serving as the primary vehicle for high-dose therapeutic delivery.

- Powder Blends (43.0% Market Share): Leading the format segment in 2026, these blends are favored for their seamless integration across manufacturing lines and diverse delivery formats, despite challenges in batch-to-batch density consistency.

- Glucose Support (34.0% Market Share): This functional application is the primary driver for consumer acquisition, directly addressing the needs of populations monitoring HbA1c levels.

- Olive Polyphenols (31.0% Market Share): Valued for robust clinical dossiers, these extracts are the "gold standard" for modulating insulin sensitivity and meeting EFSA-level regulatory scrutiny.

- Dietary Supplements (46.0% Market Share): Remains the dominant channel, as it allows for the precise, high-concentration dosing required to achieve physiological results that food formats often cannot match.

Regional Velocity: Spain and Italy Lead the Metabolic Pivot

While Southern Europe remains the agricultural engine, North Africa is rapidly emerging as a sophisticated processing hub for high-value botanical exports.

| Country | Projected CAGR (2026-2036) | Strategic Driver |

| Spain | 10.4% | Integrated supply chains connecting domestic olive/grape cultivation to advanced extraction. |

| Italy | 9.8% | High domestic consumer literacy and demand for clinically backed metabolic formulations. |

| Greece | 9.5% | Agricultural cooperatives pivoting from bulk supply to high-value bioactive production. |

| Turkey | 9.2% | Leveraging competitive processing costs to serve as a primary node for regional export. |

| Morocco | 9.0% | State-sponsored modernization elevating local facilities to international pharmaceutical standards. |

| Egypt | 8.7% | Rising domestic diagnostic awareness driving expansion in pharmacy distribution networks. |

| France | 8.1% | Strict regulatory frameworks favoring heavily researched, premium-tier ingredients. |

Strategic Takeaways for Stakeholders

- Clinical Substantiation as a Barrier: Success is no longer determined by raw material cost but by the depth of a proprietary clinical dossier. Brands without validated delivery mechanisms face high churn as consumers fail to see changes in fasting glucose numbers.

- Supply Chain Resilience: Procurement managers must secure multi-year off-take agreements to buffer against the extreme price fluctuations typical of Mediterranean agricultural cycles.

- Bioavailability Innovation: R&D focus is shifting toward "digestive survival," ensuring that active phytochemicals reach intended absorption sites without being neutralized during transit.

"Measurement frameworks in metabolic supplements are shifting," says Nandini Roy Choudhury, Principal Analyst at FMI. "Procurement directors who optimize solely for the lowest cost-per-kilogram often miss the reality that poor bioavailability destroys clinical efficacy. Standardizing the active compound means very little when the extract fails to survive digestive transit."

Competitive Landscape

The market is defined by specialized extraction houses that control the "source-to-standard" pipeline. Leading players like Indena, Euromed, and Pharmactive Biotech Products are maintaining dominance by providing retailers with the "regulatory insurance" of proven clinical dossiers.

Competition is also intensifying in Morocco and Tunisia, where facilities are upgrading to meet European pharmaceutical standards, allowing them to capture higher margins previously reserved for Western European processors.

Key Companies Profiled: Indena S.p.A., Euromed S.A., Pharmactive Biotech Products, Sabinsa Corporation, Vidya Herbs, Nektium Pharma, Gencor Pacific, and Monteloeder (a SuanNutra company)

Get Access to the Full Report Sample: Explore detailed forecasts, regional insights, and competitive analysis: https://www.futuremarketinsights.com/reports/sample/rep-gb-32542

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

+1-347-918-3531

For Sales - sales@futuremarketinsights.com

For Media - Rahul.singh@futuremarketinsights.com

For web - https://www.futuremarketinsights.com