Global Gynecological Examination Chairs Market Poised for High-Tech Evolution; Electric Variants to Command 62.8% Share by 2026

As healthcare facilities globally transition toward patient-centric infrastructure, the gynecological examination chairs market is undergoing a significant shift. Driven by a surge in preventive screenings and a focus on ""Barrier-Free"" accessibility, the market is moving away from manual legacy tables in favor of advanced, programmable electric systems.

According to a comprehensive analysis by Fact.MR, electric gynecological chairs are projected to dominate the landscape, capturing nearly 63% of the total market share by late 2026. This momentum is fueled by the critical need for ergonomic efficiency in high-volume environments like hospitals, which currently account for over 37% of end-user demand.

For Details Deep insights, Please Request A sample report for Free:

Strategic Market Snapshot: 2026 Key Metrics

Metric Value / Projection

Electric Chair Market Share 62.8% (by 2026)

Hospital Segment Share 37.1%

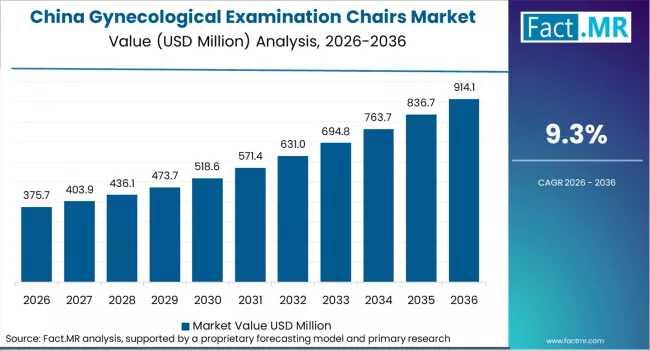

Top Growing Market (CAGR) China (9.3% through 2036)

Emerging Tech Adoption 15% Reduction in total exam time via ""Smart"" chairs

Key Market Driver Rising emphasis on cervical & reproductive health screenings

Market Momentum: Efficiency Meets Patient Comfort

The transition to Electric-Motorized ""Smart"" Chairs is no longer a luxury but a clinical necessity. Modern units now feature IP66-sealed linear actuators and programmable memory settings, allowing practitioners to recall specific positions for procedures like colposcopy with a single touch.

Automation in Care: Healthcare providers are prioritizing chairs with ultra-low entry heights (17-19 inches) to meet ADA compliance and ""Barrier-Free"" standards, significantly reducing caregiver injury during patient transfers.

Infrastructure Growth: In South Asia, India is emerging as a high-growth hub with an 8.6% CAGR, as government investments in maternal health and specialized clinics expand the need for modern diagnostic furniture.

Replacement Cycles: The 2026 ""Trade-In to Trade-Up"" initiatives are accelerating the phase-out of manual equipment, with rebates encouraging the adoption of multi-functional, ergonomic platforms.

""The 2026 valuation reflects a steady demand tied to routine screenings and clinic upgrades. While cost-sensitive settings still use multi-purpose tables, high-value electric units are gaining share due to their integrated lighting, hygiene features, and enhanced procedural access."" - Fact.MR Analyst

Regional CAGR Analysis (2026-2036)

The following countries represent the most aggressive growth corridors for medical equipment manufacturers:

China: 9.3%

India: 8.6%

Germany: 7.9%

France: 7.2%

United Kingdom: 6.6%

Competitive Landscape

The market is characterized by moderate concentration, where differentiation is driven by ergonomic design and regulatory expertise. Leading manufacturers like Oakworks, Inc., Arjo AB, and Malvestio S.r.l. are increasingly securing long-term contracts with large healthcare groups, where the focus has shifted from initial price to Total Cost of Ownership (TCO), including servicing and warranty.