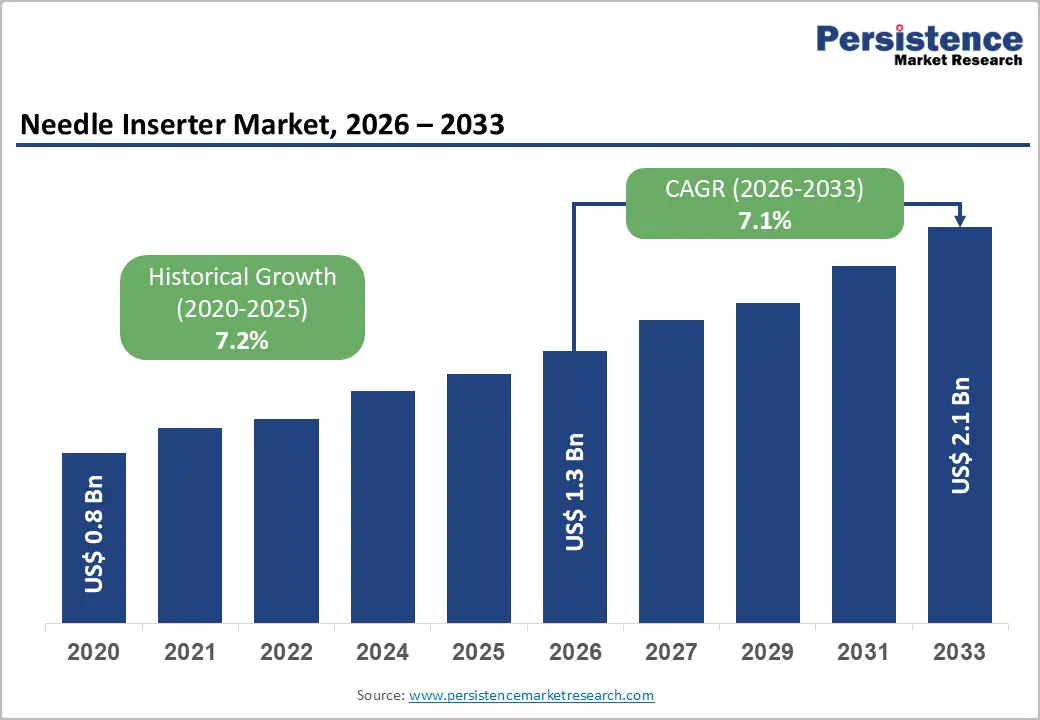

The global needle inserter market is witnessing steady growth, driven by the increasing demand for minimally invasive medical procedures, rising prevalence of chronic diseases, and the growing need for precise and safe drug delivery systems. The market is expected to be valued at US$1.3 billion in 2026 and is projected to reach US$2.1 billion by 2033, expanding at a CAGR of 7.1% during the forecast period from 2026 to 2033. Needle inserters are widely used in healthcare settings to facilitate accurate needle placement for procedures such as biopsies, blood sampling, and drug administration. The increasing adoption of automation in healthcare, coupled with advancements in medical device technologies, is significantly enhancing the efficiency and safety of these devices. Moreover, the rising geriatric population and increasing incidence of conditions such as diabetes and cancer are contributing to the growing demand for needle-based interventions.

From a segmentation perspective, automated needle inserters dominate the market due to their precision, reduced risk of human error, and improved patient comfort. These devices are increasingly preferred in hospitals and diagnostic centers for complex procedures requiring high accuracy. In terms of end users, hospitals and specialty clinics account for the largest share, driven by the high volume of medical procedures performed in these settings. Geographically, North America leads the global needle inserter market, supported by advanced healthcare infrastructure, high adoption of innovative medical technologies, and strong presence of key market players. Meanwhile, the Asia-Pacific region is emerging as a high-growth market, driven by expanding healthcare infrastructure, rising healthcare expenditure, and increasing awareness about advanced medical devices in countries such as China and India.

Get Your FREE Sample Report Instantly Click Now:

https://www.persistencemarketresearch.com/samples/32663

Key Highlights from the Report:

✦ The needle inserter market is projected to grow at a CAGR of 7.1% from 2026 to 2033.

✦ Market size is expected to increase from US$1.3 billion in 2026 to US$2.1 billion by 2033.

✦ Automated needle inserters dominate due to precision and reduced human error.

✦ Hospitals and specialty clinics represent the leading end-user segment.

✦ North America holds the largest market share due to advanced healthcare systems.

✦ Asia-Pacific is emerging as a high-growth region with expanding healthcare infrastructure.

Market Segmentation

The needle inserter market is segmented based on product type, application, and end-user categories. By product type, the market includes manual needle inserters and automated needle inserters. Automated systems are gaining significant traction due to their ability to enhance procedural accuracy and minimize patient discomfort. These devices are particularly useful in complex procedures such as biopsies and targeted drug delivery, where precision is critical. Manual needle inserters, while still widely used, are gradually being replaced by automated solutions in advanced healthcare settings.

In terms of application, the market is categorized into drug delivery, blood collection, biopsy procedures, and others. Drug delivery represents a major segment, driven by the increasing prevalence of chronic diseases such as diabetes, which require regular injections. Biopsy procedures are also contributing significantly to market demand, as early diagnosis of diseases such as cancer becomes increasingly important. Blood collection remains a fundamental application, supported by routine diagnostic testing and healthcare monitoring.

Based on end users, the market is divided into hospitals, diagnostic centers, ambulatory surgical centers, and research institutions. Hospitals dominate the segment due to the high volume of procedures performed and the availability of advanced medical equipment. Diagnostic centers are also witnessing growth due to the increasing demand for early disease detection and screening services.

Regional Insights

· North America dominates the needle inserter market due to its advanced healthcare infrastructure, high adoption of innovative medical technologies, and strong presence of leading market players. The United States plays a key role in driving regional growth, supported by significant healthcare expenditure and ongoing research and development activities.

· Europe holds a substantial market share, driven by well-established healthcare systems, increasing focus on patient safety, and rising adoption of advanced medical devices. Countries such as Germany, France, and the UK are key contributors to regional growth.

· Asia-Pacific is emerging as a lucrative market, fueled by expanding healthcare infrastructure, rising healthcare expenditure, and increasing awareness about advanced medical technologies. Countries such as China, India, and Japan are witnessing significant growth in demand for needle inserters.

· Latin America and the Middle East & Africa are experiencing gradual growth, supported by improving healthcare facilities, increasing investments in medical infrastructure, and rising awareness about advanced healthcare solutions.

Market Drivers

The needle inserter market is primarily driven by the growing demand for minimally invasive procedures, which offer benefits such as reduced recovery time, lower risk of complications, and improved patient outcomes. The increasing prevalence of chronic diseases such as diabetes, cancer, and cardiovascular conditions is driving the need for frequent injections and diagnostic procedures, boosting demand for needle inserters. Technological advancements, including automation and robotics, are enhancing the precision and efficiency of these devices, further supporting market growth. Additionally, the rising focus on patient safety and comfort is encouraging healthcare providers to adopt advanced needle insertion systems.

Market Restraints

Despite its growth potential, the needle inserter market faces several challenges. The high cost of advanced automated devices may limit their adoption in developing regions with limited healthcare budgets. Additionally, the complexity of these devices requires skilled professionals for operation, which may pose a barrier in regions with a shortage of trained healthcare personnel. Regulatory challenges and stringent approval processes for medical devices can also delay product launches and impact market growth. Furthermore, concerns related to device malfunctions and patient safety may hinder widespread adoption.

Market Opportunities

The needle inserter market presents significant opportunities for innovation and expansion. The increasing adoption of robotic-assisted procedures and smart medical devices is opening new avenues for market growth. The development of portable and user-friendly needle inserters for home healthcare applications is also gaining traction, driven by the growing trend of self-administration of medications. Emerging markets in Asia-Pacific and Latin America offer untapped potential due to improving healthcare infrastructure and rising demand for advanced medical devices. Additionally, ongoing research and development activities aimed at enhancing device performance and safety are expected to create new growth opportunities.

Company Insights

• Becton, Dickinson and Company

• Medtronic plc

• B. Braun Melsungen AG

• Terumo Corporation

• Smiths Medical

• Nipro Corporation

• Boston Scientific Corporation

• Cardinal Health Inc.

• Teleflex Incorporated

• Cook Medical

Recent Developments:

The market has witnessed increased adoption of automated and robotic needle insertion systems designed to improve accuracy and reduce patient discomfort. Additionally, companies are focusing on developing portable and home-use devices to cater to the growing demand for self-administration and remote healthcare solutions.

Conclusion

The global needle inserter market is poised for steady growth, driven by increasing demand for minimally invasive procedures, rising prevalence of chronic diseases, and technological advancements in medical devices. With a projected market size of US$2.1 billion by 2033 and a CAGR of 7.1%, the industry presents significant opportunities for innovation and expansion. While challenges such as high costs and regulatory hurdles persist, ongoing advancements in automation and healthcare infrastructure are expected to drive market growth. As the healthcare industry continues to evolve, needle inserters will play a crucial role in enhancing patient care, safety, and procedural efficiency.