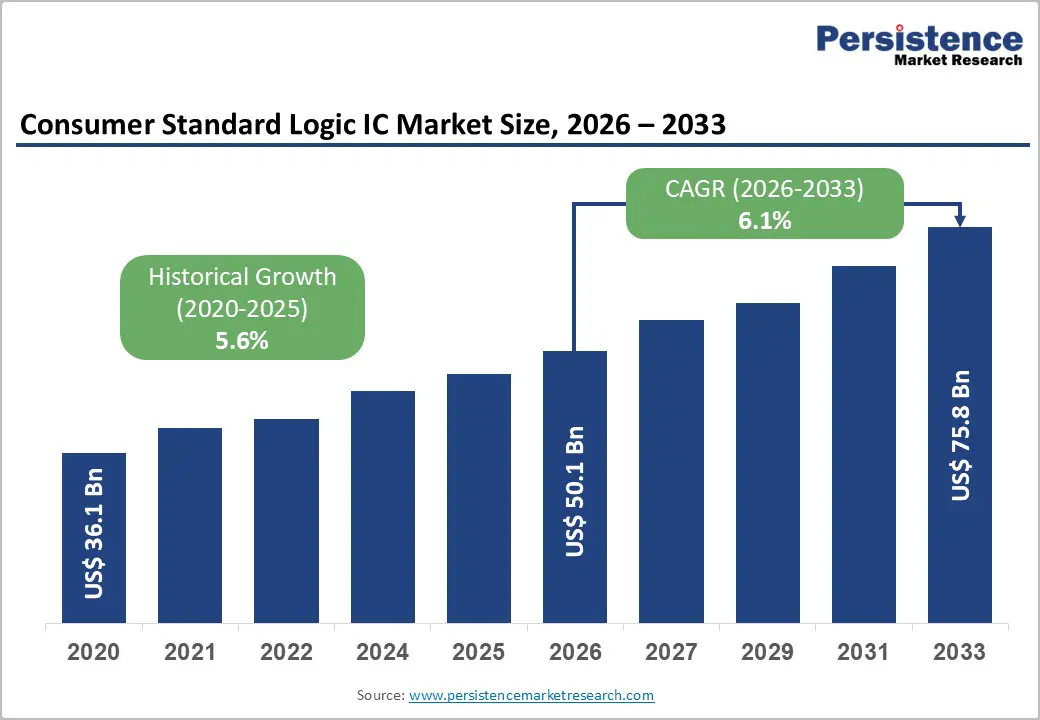

The global consumer standard logic IC market is entering a transformative growth phase as consumer electronics become increasingly sophisticated, compact, and power efficient. The market is projected to grow from US$50.1 billion in 2026 to US$75.8 billion by 2033, registering a CAGR of 6.1% during the forecast period from 2026 to 2033. This expansion is primarily driven by the aggressive integration of 5G communication modules, the rising popularity of IoT-enabled consumer devices, and the increasing demand for ultra-low-power semiconductor architectures.

Standard logic integrated circuits play a foundational role in modern electronics by enabling signal routing, voltage translation, buffering, switching, and interface management across complex device ecosystems. As smartphones, wearables, gaming systems, and smart home appliances evolve toward higher integration density, standard logic ICs are becoming indispensable components within semiconductor supply chains.

The rapid proliferation of advanced consumer electronics across Asia Pacific, North America, and Europe is further strengthening the demand for CMOS-based logic solutions capable of supporting next-generation computing and connectivity standards.

Rising 5G Smartphone Penetration Accelerating Logic IC Demand

The transition toward 5G-enabled consumer electronics is significantly increasing the semiconductor content embedded within smartphones and connected devices. Modern 5G smartphones incorporate complex radio-frequency architectures, multiple antenna systems, advanced camera modules, AI accelerators, and high-speed memory interfaces. These features require large numbers of standard logic gates, level shifters, multiplexers, and signal-conditioning components.

Smartphones are projected to account for approximately 47% of the global consumer standard logic IC market in 2026 due to their recurring upgrade cycles and broad global adoption. Flagship devices powered by processors such as Qualcomm Snapdragon, Samsung Exynos, and MediaTek Dimensity rely heavily on companion logic ICs to maintain efficient communication between multiple subsystems.

Foldable smartphones and AI-enabled mobile devices are intensifying board-level complexity. Flexible printed circuit boards and high-density packaging technologies require miniaturized logic devices capable of operating within tight thermal and power constraints. As manufacturers continue integrating advanced features such as real-time AI processing, augmented reality, and computational photography, demand for high-performance logic ICs is expected to accelerate further.

The growth of multi-band 5G networks is also increasing voltage-domain complexity within consumer devices. Logic ICs are essential in ensuring interoperability between heterogeneous voltage environments, especially in RF modules and sensor arrays. This structural shift is creating sustained long-term demand for compact, power-efficient semiconductor solutions.

IoT and Wearable Electronics Reshaping Market Dynamics

The rapid expansion of IoT ecosystems is transforming the consumer electronics industry and significantly influencing the demand profile of standard logic ICs. Connected devices such as smartwatches, wireless earbuds, fitness trackers, smart glasses, and home automation products require ultra-low-power semiconductor components capable of operating continuously while preserving battery life.

Wearables and hearables are expected to emerge as the fastest-growing application segment during the forecast period. Devices such as Apple AirPods Pro, Samsung Galaxy Buds, and Galaxy Ring increasingly depend on miniaturized logic ICs for touch sensing, biometric monitoring, audio processing, and wireless connectivity.

Ultra-low-power CMOS architectures are gaining traction because they reduce leakage currents and optimize switching efficiency. Semiconductor manufacturers are prioritizing wafer-level chip-scale packaging and compact design formats to meet the miniaturization requirements of wearable devices.

The growing adoption of health-monitoring technologies is also driving semiconductor integration intensity. Advanced wearable devices now include ECG sensors, temperature monitors, SpO2 tracking systems, and sleep analysis capabilities. These functionalities require precision signal management and voltage translation supported by standard logic ICs.

Additionally, the proliferation of smart home ecosystems is creating new opportunities for logic semiconductor vendors. Connected appliances such as smart refrigerators, surveillance systems, thermostats, and intelligent lighting systems rely on distributed sensor networks and localized edge processing, increasing the need for interface logic and signal-control components.

CMOS Technology Dominating the Competitive Landscape

CMOS technology is expected to dominate the global consumer standard logic IC market, accounting for nearly 88% of total market share in 2026. The widespread adoption of CMOS logic stems from its superior energy efficiency, low static power consumption, high noise immunity, and compatibility with advanced semiconductor nodes.

CMOS-based logic devices are deeply integrated across smartphones, IoT modules, wearables, gaming systems, and connected consumer appliances. Their ability to support high integration density while maintaining thermal efficiency makes them ideal for modern portable electronics.

Leading semiconductor companies including Texas Instruments, Nexperia, and STMicroelectronics continue expanding their CMOS logic portfolios to address increasing demand from OEMs and device manufacturers. Advanced CMOS nodes also support higher switching speeds and reduced standby power consumption, enabling longer battery life in compact consumer products.

The migration toward sub-7nm fabrication processes is further strengthening CMOS adoption. Advanced lithography techniques allow manufacturers to improve transistor density while reducing power leakage and enhancing device performance. These advancements are especially important in AI-enabled smartphones, AR devices, and ultra-compact wearables.

AI-assisted electronic design automation tools are also helping semiconductor companies optimize layout complexity, improve yields, and reduce manufacturing inefficiencies. As semiconductor process technologies mature, CMOS logic solutions are expected to remain the preferred choice across high-volume consumer electronics applications.

Asia Pacific Emerging as the Global Semiconductor Powerhouse

Asia Pacific is projected to remain both the largest and fastest-growing regional market for consumer standard logic ICs, accounting for approximately 65% of global market share in 2026. The region’s dominance is driven by its concentration of semiconductor foundries, electronics manufacturing hubs, advanced packaging facilities, and vertically integrated OEM ecosystems.

Countries such as China, Taiwan, South Korea, and Japan collectively form the backbone of global semiconductor production. Industry leaders including TSMC, Samsung Electronics, and SMIC are continuing to expand advanced-node fabrication capacity to support growing demand for logic semiconductors.

China is expected to remain a critical regional anchor due to its strong domestic electronics manufacturing industry and government-backed semiconductor self-reliance initiatives. The country’s investment in localized semiconductor production, advanced packaging, and AI-driven electronics manufacturing is strengthening supply chain resilience across the Asia-Pacific region.

Taiwan continues to lead advanced semiconductor fabrication, particularly in sub-7nm logic production. South Korea’s dominance in memory and advanced mobile processors further supports regional growth. Meanwhile, Japan’s expertise in semiconductor materials, equipment, and precision electronics remains strategically important for the global supply chain.

The rapid expansion of 5G infrastructure, IoT deployment, and edge AI adoption across Asia Pacific is expected to sustain strong demand for standard logic ICs throughout the forecast period.

Rising Manufacturing Costs Creating Industry Challenges

Despite favorable growth prospects, the consumer standard logic IC market faces significant structural challenges related to escalating manufacturing complexity and capital intensity.

The migration toward advanced semiconductor nodes requires substantial investments in lithography equipment, fabrication infrastructure, and process optimization. Building advanced semiconductor fabrication facilities can cost up to US$20 billion, creating high barriers to entry for smaller manufacturers.

As transistor geometries shrink below seven nanometers, semiconductor design complexity increases dramatically. Manufacturers must address issues related to leakage current, thermal management, electromigration, and yield optimization. These factors increase research and development expenditures while compressing profitability in traditionally low-margin standard logic categories.

The adoption of extreme ultraviolet lithography further raises production costs and limits participation to highly capitalized semiconductor companies. Smaller suppliers may struggle to compete in advanced-node production environments, contributing to industry consolidation.

Supply chain volatility and geopolitical tensions also remain ongoing concerns. Export controls, semiconductor trade restrictions, and regional sourcing realignments are influencing procurement strategies and manufacturing localization initiatives across the industry.

Edge AI and Green Electronics Creating Future Opportunities

The integration of edge artificial intelligence within consumer electronics represents a major long-term opportunity for standard logic IC manufacturers. Smart home appliances, AI-enabled surveillance systems, and connected consumer platforms increasingly process data locally rather than relying solely on cloud infrastructure.

Localized AI processing requires complex mixed-voltage architectures, creating demand for advanced-level shifters, buffers, and signal-conditioning logic. Standard logic ICs serve as critical bridging components between legacy sensors, AI processors, and communication modules.

The rise of green electronics is also reshaping semiconductor design priorities. Governments and regulatory bodies worldwide are emphasizing energy-efficient consumer electronics to support sustainability objectives and reduce carbon emissions.

Ultra-low-power logic architectures are becoming essential for always-on devices operating under strict battery and energy consumption constraints. Advanced CMOS and BiCMOS technologies enable substantial reductions in standby leakage currents, improving device longevity and reducing cumulative energy footprints.

As environmental regulations become more stringent, semiconductor vendors capable of delivering energy-efficient logic solutions are expected to gain competitive advantages across consumer electronics markets.

Competitive Landscape

The global consumer standard logic IC market is moderately consolidated, with major players focusing on product innovation, low-power architectures, packaging miniaturization, and ecosystem partnerships.

Key companies operating in the market include:

- Texas Instruments

- Nexperia

- ON Semiconductor

- Toshiba Electronic Devices & Storage Corporation

- Renesas Electronics Corporation

- STMicroelectronics

- Diodes Incorporated

- Microchip Technology

- Analog Devices

- NXP Semiconductors

- ROHM Semiconductor

- Broadcom

- Infineon

- MediaTek

- Skyworks

- Qorvo

Industry participants are increasingly investing in advanced packaging technologies, AI-integrated semiconductor solutions, and ultra-low-leakage logic architectures to maintain competitiveness within rapidly evolving consumer electronics ecosystems.

Conclusion

The global consumer standard logic IC market is positioned for sustained expansion as 5G connectivity, IoT proliferation, wearable electronics, and edge AI adoption continue reshaping the consumer technology landscape. Standard logic ICs remain essential enablers of signal management, voltage translation, and system interoperability across increasingly complex electronic architectures.

Asia Pacific is expected to maintain its leadership position through its strong semiconductor manufacturing ecosystem and aggressive investment in advanced-node fabrication. Meanwhile, innovations in CMOS technology, ultra-low-power architectures, and green electronics are creating new growth avenues for semiconductor vendors.

Although rising manufacturing costs and advanced-node complexity present challenges, the long-term outlook for the consumer standard logic IC market remains highly favorable. As connected consumer devices become more intelligent, compact, and energy efficient, demand for advanced logic semiconductor solutions is expected to continue accelerating through 2033.