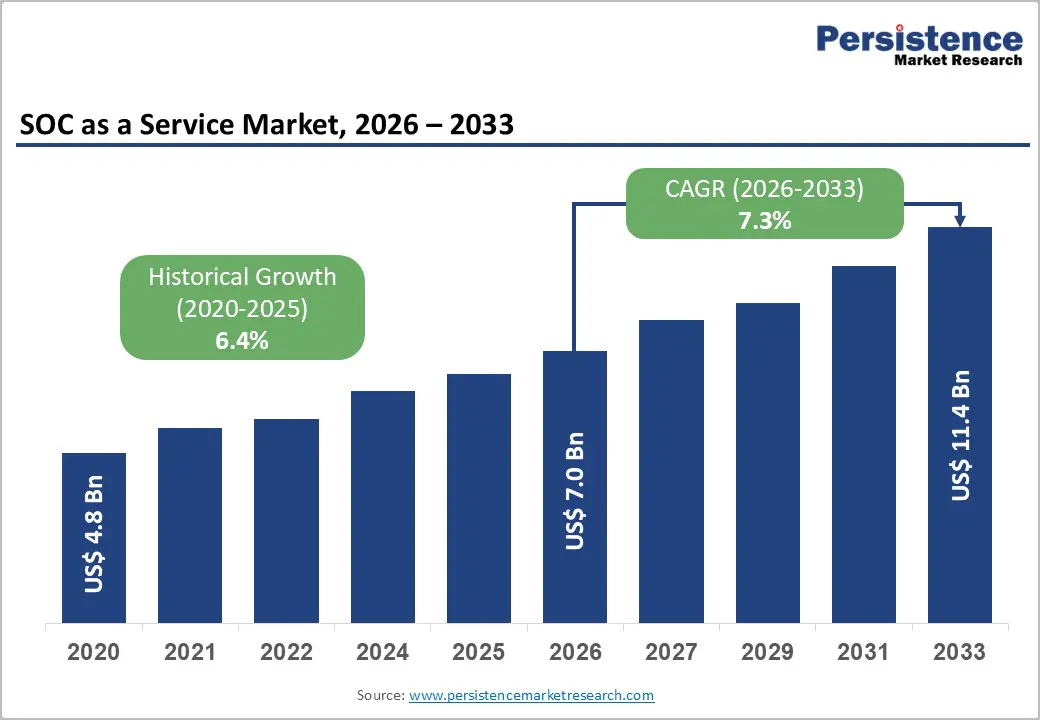

The global SOC-as-a-Service (SOCaaS) market is entering a transformative phase as enterprises increasingly prioritise real-time cybersecurity monitoring, rapid incident response, and regulatory compliance. The market is expected to reach US$ 7.0 billion in 2026 and further expand to US$ 11.4 billion by 2033, registering a CAGR of 7.3% between 2026 and 2033.

The growing sophistication of cyberattacks, rising ransomware incidents, and severe shortages of skilled cybersecurity professionals are accelerating demand for outsourced security operations solutions. Organisations across industries are recognising that traditional in-house security teams often struggle to provide 24/7 monitoring, proactive threat detection, and rapid response capabilities at scale. As a result, SOCaaS has evolved from an optional managed service into a mission-critical cybersecurity infrastructure model.

Today’s enterprises operate across hybrid environments consisting of cloud platforms, on-premises systems, remote workforces, mobile devices, and IoT ecosystems. This increasing complexity has dramatically expanded the attack surface, creating continuous demand for advanced detection and monitoring services. SOCaaS providers address these challenges through managed security operations powered by SIEM platforms, AI-driven analytics, behavioural monitoring, and expert-led incident response.

Rising Cybersecurity Skills Shortage Driving SOCaaS Adoption

One of the strongest growth drivers for the SOC as a Service market is the global shortage of cybersecurity talent. Organisations worldwide face difficulty recruiting and retaining experienced security analysts, incident responders, cloud security specialists, and threat hunters.

The cybersecurity workforce gap has widened substantially in recent years, leaving millions of security roles unfilled globally. Enterprises with understaffed security teams often experience delayed threat detection, longer attacker dwell times, and significantly higher breach costs.

SOCaaS providers help businesses overcome this challenge by delivering access to highly skilled security professionals without requiring organisations to build large internal SOC teams. Managed SOC services provide continuous monitoring, forensic analysis, compliance reporting, and threat intelligence through subscription-based models, making enterprise-grade cybersecurity more accessible.

This trend is particularly evident among mid-sized organisations that cannot afford the operational burden of maintaining in-house 24/7 security operations. Healthcare institutions, financial firms, government agencies, and manufacturing companies are increasingly outsourcing security operations to improve resilience while controlling operational costs.

Escalating Ransomware and Advanced Threat Activity

The modern ransomware landscape has become significantly more sophisticated. Threat actors are no longer relying solely on basic encryption attacks. Instead, attackers now deploy multi-stage campaigns involving data exfiltration, double extortion tactics, credential theft, and supply chain compromise strategies.

Ransomware groups are also adopting AI-assisted attack development, enabling faster malware customisation and more evasive attack patterns. These developments have raised the complexity of threat detection and response, making continuous security monitoring essential.

SOCaaS platforms play a critical role in defending against these evolving threats. Providers continuously analyse network traffic, monitor endpoint behaviour, correlate threat intelligence feeds, and automate detection workflows to identify suspicious activity before attacks escalate.

Managed SOC teams also provide coordinated incident response capabilities, including:

- Threat containment

- Malware eradication

- Digital forensics

- Evidence preservation

- Recovery support

- Compliance documentation

Industries such as BFSI, healthcare, telecom, and critical infrastructure are especially vulnerable to ransomware due to the operational and financial impact of downtime. This vulnerability continues to drive investments in outsourced security operations.

Regulatory Compliance Becoming a Major Market Catalyst

Global cybersecurity regulations are becoming stricter and more demanding. Governments and regulators increasingly require organisations to maintain robust incident detection, reporting, and response capabilities.

Regulations such as GDPR, NIS2, HIPAA, NYDFS cybersecurity requirements, and RBI cybersecurity frameworks are compelling organisations to establish continuous monitoring systems capable of rapid threat identification and breach reporting.

For example:

- GDPR requires breach notification within 72 hours.

- NIS2 mandates rapid incident reporting obligations.

- RBI requires Indian banks to report critical cybersecurity incidents within six hours.

- Financial regulators increasingly demand regular penetration testing and board-level cybersecurity reporting.

SOCaaS providers help organisations meet these obligations by delivering compliance-aligned monitoring, audit-ready reporting, and documented incident response workflows.

As cybersecurity governance becomes a board-level priority, managed SOC services are increasingly viewed as mandatory compliance infrastructure rather than discretionary IT spending.

AI and Automation Transforming Security Operations

Artificial intelligence and automation are reshaping the economics of security operations centres. Modern SOCaaS platforms increasingly rely on AI-powered analytics, machine learning algorithms, and automated response orchestration to reduce analyst workloads and improve detection accuracy.

AI-enabled SOC systems can process vast amounts of security telemetry in real time, helping organisations identify anomalies faster and reduce false positives. Automated triage workflows allow security teams to focus on high-priority threats rather than routine alerts.

Emerging AI-native SOC platforms are introducing advanced capabilities such as:

- Automated threat investigation

- Behavioural anomaly detection

- AI-assisted threat hunting

- Automated playbook execution

- Intelligent alert prioritisation

- Predictive threat modelling

These innovations significantly improve operational efficiency and help address the global cybersecurity talent shortage. AI-driven SOCaaS solutions are also lowering service delivery costs, making managed security operations increasingly viable for small and mid-sized businesses.

Cloud Migration Creating New Security Challenges

Rapid cloud adoption is another major factor driving the SOCaaS market. Organisations are increasingly migrating workloads to public cloud platforms while adopting multi-cloud and hybrid IT architectures.

Cloud-native environments introduce unique security challenges involving:

- Container security

- Serverless workloads

- Identity and access management

- Cloud misconfigurations

- API vulnerabilities

- Distributed infrastructure visibility

Traditional on-premises security tools often lack the visibility required to monitor modern cloud ecosystems effectively. SOCaaS providers address this challenge by integrating cloud-native monitoring, cloud workload protection, and centralised visibility across hybrid environments.

As enterprises continue expanding digital transformation initiatives, demand for cloud-focused SOC services is expected to rise substantially.

Detection Services Continue to Dominate

Detection services remain the largest segment within the SOC as a Service market, accounting for nearly 40% market share in 2026.

Organisations prioritise continuous threat visibility as the foundation of cybersecurity operations. Detection services typically include:

- SIEM management

- Threat monitoring

- Intrusion detection

- Endpoint detection

- Log analysis

- Behavioural analytics

- Threat intelligence integration

These capabilities enable businesses to rapidly identify malicious activity across complex IT ecosystems.

Meanwhile, incident response services are emerging as the fastest-growing segment due to the increasing severity of ransomware attacks and regulatory expectations regarding breach response quality.

Organisations increasingly seek managed providers capable of delivering both detection and response under unified security operations frameworks.

BFSI Sector Leads SOCaaS Adoption

The Banking, Financial Services, and Insurance (BFSI) sector remains the largest end-use industry in the SOCaaS market, accounting for approximately 35% market share in 2026.

Financial institutions face persistent cyber threats involving:

- Financial fraud

- Credential theft

- Data breaches

- Ransomware attacks

- Payment system compromise

- Insider threats

Additionally, financial organisations operate under strict regulatory oversight, making continuous security monitoring essential.

The rapid expansion of digital banking, fintech platforms, mobile payments, and online financial services has further increased cybersecurity risks. Consequently, banks and insurance firms are investing heavily in outsourced SOC services to maintain operational resilience and regulatory compliance.

The IT and telecom sector is also witnessing strong SOCaaS adoption due to growing dependence on uninterrupted network availability, expanding 5G infrastructure, and increasingly distributed digital ecosystems.

North America Maintains Market Leadership

North America continues to dominate the global SOC as a Service market with approximately 39% market share.

The region benefits from:

- High cybersecurity maturity

- Strong regulatory enforcement

- Early adoption of managed security services

- Large enterprise IT spending

- Advanced cloud adoption

The United States remains the largest regional contributor due to widespread cybersecurity investments across financial services, healthcare, retail, and critical infrastructure sectors.

Major cybersecurity vendors and managed security providers continue expanding SOC capabilities through acquisitions, AI integration, and cloud-native security innovation.

East Asia Emerges as the Fastest-Growing Region

East Asia represents one of the fastest-growing markets for SOCaaS, supported by rapid digitalisation and increasing cybersecurity awareness across China, Japan, and South Korea.

Several factors are contributing to regional growth:

- Expanding cloud adoption

- Rising cyberattack frequency

- Tightening cybersecurity regulations

- Growing enterprise digitisation

- Increased internet penetration

China’s rapidly expanding digital ecosystem has created substantial demand for advanced threat monitoring and compliance-focused security operations.

Regional governments are also strengthening cybersecurity governance frameworks, further accelerating adoption of managed SOC services.

Europe Shows Strong Compliance-Driven Demand

Europe holds a significant share of the global SOCaaS market, supported by strict data protection and cybersecurity regulations.

The region’s adoption is heavily influenced by:

- GDPR compliance requirements

- NIS2 Directive implementation

- Financial sector cybersecurity mandates

- Data sovereignty concerns

European organisations increasingly require regionally hosted SOC infrastructure to comply with local data protection standards. This has encouraged managed security providers to expand localised SOC capabilities across major European markets.

Competitive Landscape Remains Dynamic

The global SOC as a Service market remains moderately consolidated, with intense competition among established cybersecurity firms and specialised managed security providers.

Leading companies are focusing on:

- AI-powered SOC platforms

- Cloud-native security operations

- Managed detection and response (MDR)

- Threat intelligence integration

- Automated incident response

- Strategic partnerships and acquisitions

Major players operating in the market include:

- IBM Corporation

- Fortinet, Inc.

- Cloudflare, Inc.

- Verizon Communications Inc.

- Thales Group

- Arctic Wolf Networks, Inc.

- AT&T Inc.

- Nippon Telegraph and Telephone Corporation

Recent developments highlight the industry’s transition toward AI-native SOC models capable of automating large portions of the security operations lifecycle.

Future Outlook

The future of the SOC as a Service market appears highly promising as cybersecurity threats continue evolving in scale and sophistication. Organisations increasingly recognise that continuous monitoring, rapid detection, and expert-led response capabilities are essential for maintaining operational resilience.

Several long-term trends are expected to shape market growth through 2033:

- Increasing adoption of AI-powered SOC automation

- Expansion of cloud-native security operations

- Growing demand for MDR services

- Rising regulatory compliance requirements

- Continued ransomware escalation

- Broader SOCaaS adoption among mid-sized enterprises

As enterprises continue modernising digital infrastructure, SOCaaS providers that combine advanced analytics, automation, compliance expertise, and scalable cloud-native architectures will be best positioned for long-term success.

The market’s steady growth trajectory reflects the broader transformation of cybersecurity from a reactive IT function into a strategic business resilience priority.