The global maritime industry is undergoing one of the most transformative periods in its history. Shipbuilders are increasingly moving away from traditional manufacturing practices toward digitally connected, automated, and data-driven shipyard ecosystems. This transition has given rise to the rapidly expanding global digital shipyard market.

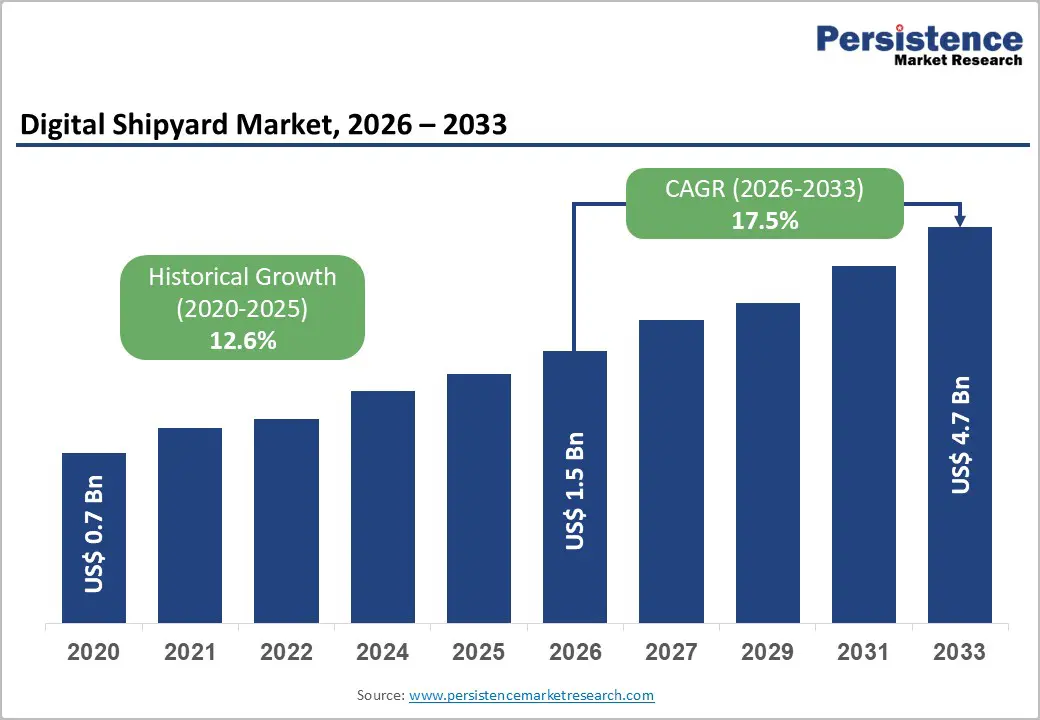

The global digital shipyard market size is expected to reach US$ 1.5 billion in 2026 and is projected to climb to US$ 4.7 billion by 2033, registering a robust CAGR of 17.5% between 2026 and 2033. This significant acceleration from the historical CAGR of 12.6% reflects the growing urgency for digital transformation across commercial and naval shipbuilding operations worldwide.

Digital shipyards are no longer viewed as optional modernization initiatives. Instead, they are becoming strategic infrastructure investments that help shipbuilders improve productivity, reduce operational risks, enhance design precision, and meet increasingly stringent environmental and defense requirements.

What is a Digital Shipyard?

A digital shipyard refers to a highly integrated shipbuilding environment that leverages advanced technologies such as:

- Digital twins

- Artificial intelligence (AI)

- Internet of Things (IoT)

- Cloud computing

- Robotics and automation

- Augmented reality (AR)

- Model-based systems engineering (MBSE)

- Predictive analytics

These technologies enable shipbuilders to digitally manage every stage of a vessel’s lifecycle—from conceptual design and engineering to manufacturing, maintenance, and decommissioning.

Unlike conventional shipyards that rely heavily on manual processes and fragmented workflows, digital shipyards create connected ecosystems where data flows seamlessly across departments, suppliers, and operational teams.

Key Factors Driving Digital Shipyard Market Growth

Rising Labour Shortages Across Shipbuilding Industry

One of the strongest drivers accelerating digital shipyard adoption is the growing shortage of skilled labor across global shipbuilding hubs.

Shipbuilding has traditionally depended on experienced welders, engineers, fabricators, and technicians. However, aging workforces and declining interest in maritime trades among younger generations are creating severe workforce constraints.

Digital shipyard technologies help bridge this gap through automation and workforce augmentation tools.

For example:

- Automated robotic welding reduces dependency on manual labor

- AR-guided assembly systems improve worker efficiency

- AI-driven quality inspection minimizes human error

- Predictive analytics optimize workforce scheduling

These technologies allow shipyards to maintain productivity despite labor shortages while simultaneously improving precision and reducing rework costs.

Digital Twins are Revolutionizing Shipbuilding

Digital twin technology has emerged as one of the most important innovations in modern shipbuilding.

A digital twin is a virtual replica of a physical vessel, ship component, or entire production process. Shipyards use digital twins to simulate vessel behavior, detect engineering conflicts, and optimize manufacturing before actual construction begins.

Many shipbuilders report measurable productivity improvements after implementing digital twin systems. Benefits include:

- Faster design cycles

- Lower material waste

- Improved structural accuracy

- Reduced production delays

- Better lifecycle maintenance planning

Digital twins also help shipbuilders manage increasingly complex vessel designs involving LNG propulsion systems, hybrid energy technologies, and autonomous navigation platforms.

Growing Defense Modernization Programs Fueling Demand

Defense modernization has become another major catalyst driving the digital shipyard market.

Governments worldwide are significantly increasing naval spending amid rising geopolitical tensions and maritime security concerns. Modern naval programs now require advanced digital engineering infrastructure as part of procurement standards.

Military shipbuilding projects increasingly mandate:

- Digital continuity across vessel lifecycles

- Secure collaborative engineering platforms

- MBSE integration

- Advanced simulation environments

- Real-time manufacturing visibility

Countries across Europe, North America, and Asia-Pacific are investing heavily in digitally enabled naval shipyards to accelerate warship production and improve fleet readiness.

Programs such as Europe’s EDINAF initiative are establishing unified digital architectures for future naval vessels, further strengthening long-term demand for digital shipyard platforms.

Environmental Regulations are Accelerating Transformation

The maritime industry is also facing intense pressure to reduce emissions and improve sustainability.

The International Maritime Organization (IMO) has introduced aggressive decarbonization goals targeting net-zero emissions by 2050. This transition is pushing shipbuilders toward alternative-fuel vessel designs powered by:

- LNG

- Hydrogen

- Ammonia

- Biofuels

- Hybrid-electric propulsion systems

Designing these advanced vessels requires integration of highly complex engineering systems across multiple disciplines.

Digital shipyard platforms enable engineers to optimize propulsion systems, energy management, structural efficiency, and emissions performance simultaneously.

As a result, digital transformation is becoming essential for shipyards seeking to remain competitive in the era of sustainable shipping.

Commercial Vessels Dominate the Market

Commercial vessels currently account for the largest share of the digital shipyard market, representing approximately 40% of global revenue.

This dominance reflects the massive scale of global commercial shipbuilding activities involving:

- Container ships

- LNG carriers

- Tankers

- Bulk carriers

- Offshore support vessels

Commercial shipbuilders operate under intense cost pressure and highly competitive market conditions. Digital shipyard solutions help improve:

- Production scheduling

- Material utilization

- Labor productivity

- Construction accuracy

- Delivery timelines

Large shipbuilders in South Korea and China are aggressively investing in advanced digital infrastructure to maintain leadership in global commercial vessel production.

Naval Vessel Segment Emerging as Fastest-Growing

While commercial ships currently dominate overall market share, naval vessels are projected to become the fastest-growing segment during the forecast period.

Military shipbuilding projects involve exceptionally high levels of complexity, customization, and cybersecurity requirements. Digital shipyards provide critical capabilities for:

- Complex systems integration

- Lifecycle management

- Mission simulation

- Secure digital collaboration

- Advanced maintenance planning

As governments prioritize naval modernization programs, demand for digitally enabled shipbuilding environments is expected to accelerate significantly.

Ship Design and Engineering Lead Market Applications

Among all application segments, ship design and engineering currently hold the largest market share.

Advanced digital engineering platforms help shipyards dramatically reduce vessel design timelines while improving manufacturability and performance optimization.

Modern ship design systems incorporate:

- 3D parametric modeling

- Hydrodynamic simulation

- Structural analysis

- Clash detection

- Integrated cost estimation

- AI-assisted optimization

These capabilities reduce downstream manufacturing risks and improve coordination between engineering and production teams.

Software platforms from leading technology providers are enabling even mid-sized shipyards to access sophisticated design capabilities previously limited to major global shipbuilders.

Construction Planning and Manufacturing are Expanding Rapidly

Construction management and manufacturing planning applications are also witnessing strong growth.

Digital manufacturing execution systems help shipyards achieve greater visibility into workshop operations, production bottlenecks, and supply chain coordination.

Key benefits include:

- Improved schedule adherence

- Better resource allocation

- Real-time production monitoring

- Enhanced quality control

- Lower operational downtime

IoT sensors and AI analytics allow supervisors to identify inefficiencies early and optimize workflow performance across shipyard operations.

East Asia Leads the Global Market

East Asia currently dominates the global digital shipyard market with approximately 30% market share.

The region’s leadership is driven primarily by South Korea and China, which collectively account for a substantial portion of global commercial shipbuilding activity.

Major South Korean shipbuilders such as:

- Samsung Heavy Industries

- HD Hyundai Heavy Industries

- Daewoo Shipbuilding & Marine Engineering

are heavily investing in digital shipyard ecosystems that integrate automation, robotics, AI, and digital twin technologies.

China is also accelerating digital transformation efforts through state-backed industrial modernization initiatives focused on advanced manufacturing and smart shipbuilding infrastructure.

North America Expanding Through Naval Investments

North America accounts for approximately 27% of the global market, largely supported by strong U.S. naval modernization spending.

Major shipbuilding programs involving submarines, aircraft carriers, and destroyers are incorporating advanced digital infrastructure requirements.

Leading U.S. defense shipbuilders such as:

- Huntington Ingalls Industries

- General Dynamics

- Austal

are modernizing facilities with advanced automation and digital engineering systems.

Commercial shipyard modernization is also gaining momentum as U.S. operators seek to improve competitiveness against Asian shipbuilding giants.

Europe Focused on Naval and Specialized Vessels

Europe represents roughly 23% of the digital shipyard market.

Unlike Asia’s commercial shipbuilding focus, Europe’s market is centered heavily around naval vessels and specialized maritime applications.

The European Union’s growing defense investments and strategic autonomy initiatives are supporting strong adoption of digital shipyard technologies.

Programs such as the EDINAF project are helping establish interoperable digital standards for future European naval fleets.

European shipbuilders are also leveraging digital engineering to maintain competitiveness in high-value vessel categories such as:

- Cruise ships

- Offshore energy vessels

- Research ships

- Defense platforms

Challenges Limiting Market Expansion

Despite strong growth prospects, several barriers continue to affect market adoption.

High Capital Investment Requirements

Implementing enterprise-scale digital shipyard systems requires substantial investment in:

- Software platforms

- Cybersecurity systems

- Automation infrastructure

- IoT networks

- Workforce retraining

For large shipyards, implementation costs can exceed tens of millions of dollars.

Integration Complexity

Many shipyards still operate with legacy infrastructure and fragmented IT systems.

Integrating modern digital platforms with older manufacturing equipment and ERP systems creates technical challenges that can delay deployment and increase project costs.

Long Return on Investment Timelines

Shipbuilding remains a cyclical industry influenced by global trade conditions and economic fluctuations.

As a result, some shipyards remain cautious about committing to large-scale digital transformation projects with long ROI timelines.

Autonomous Vessel Development Creating New Opportunities

Autonomous and unmanned vessel technologies are opening new growth avenues for digital shipyards.

Future autonomous cargo ships and unmanned naval vessels will require advanced simulation environments, AI-driven navigation systems, and digital lifecycle management capabilities.

Digital shipyards provide the infrastructure needed to:

- Test autonomous navigation algorithms

- Simulate vessel behavior

- Train remote operators

- Optimize sensor integration

Countries such as India are already investing in autonomous vessel development initiatives, creating new opportunities for shipbuilding technology providers.

Competitive Landscape

The global digital shipyard market remains moderately consolidated, with a limited number of major technology providers dominating the software ecosystem.

Key companies operating in the market include:

- Siemens

- Dassault Systèmes

- Accenture

- SAP

- AVEVA Group

- IFS

- Navantia

- Wärtsilä

Strategic partnerships between shipbuilders, software vendors, and automation companies are becoming increasingly important as the industry moves toward fully integrated smart shipyard ecosystems.

Future Outlook

The future of the digital shipyard market appears exceptionally strong as global shipbuilding enters a new era defined by automation, sustainability, and defense modernization.

Shipyards are rapidly transitioning from labor-intensive industrial facilities into intelligent manufacturing ecosystems powered by AI, digital twins, robotics, and connected engineering platforms.

As shipping companies demand cleaner vessels, governments prioritize naval modernization, and autonomous maritime systems continue to evolve, digital shipyards will become essential infrastructure for the future global maritime economy.

Over the next decade, digital transformation is expected to fundamentally redefine how ships are designed, built, operated, and maintained across commercial and defense sectors alike.