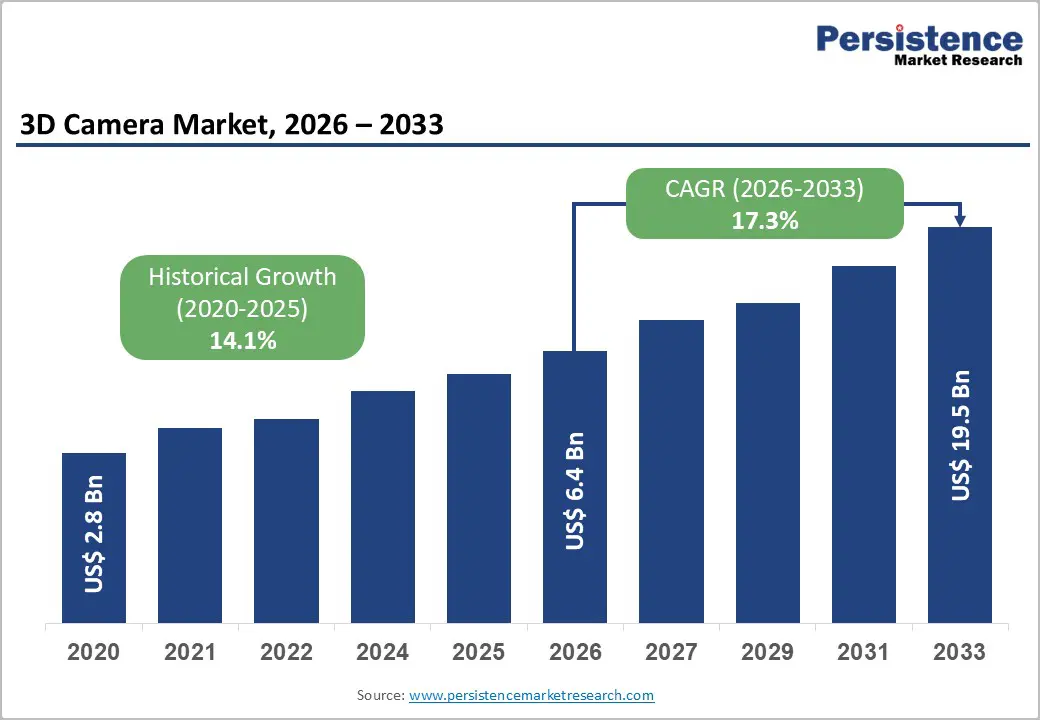

The global 3D camera market is entering a high-growth phase as industries increasingly adopt depth-sensing and spatial imaging technologies to improve automation, safety, and immersive digital experiences. The market is projected to grow from US$ 6.4 billion in 2026 to US$ 19.5 billion by 2033, registering a strong CAGR of 17.3% during the forecast period.

The growing need for accurate real-time depth perception across smartphones, autonomous vehicles, robotics, healthcare imaging, and industrial automation is transforming 3D cameras from a niche technology into a mainstream sensing solution. Unlike conventional 2D cameras, 3D cameras capture depth information alongside visual data, enabling machines and devices to understand spatial environments more intelligently.

The rise of augmented reality (AR), virtual reality (VR), mixed reality, facial recognition, digital twins, and AI-powered machine vision is accelerating demand for advanced 3D imaging systems worldwide. At the same time, continuous innovations in Time-of-Flight (ToF) sensors, stereo vision systems, AI chips, and edge computing are improving performance while reducing integration complexity and power consumption.

Understanding the Growing Importance of 3D Cameras

3D cameras are becoming essential in modern intelligent systems because they enable machines to perceive distance, movement, and object dimensions in real time. This capability is critical for applications where accurate environmental understanding is required.

In smartphones, 3D cameras support facial authentication, portrait photography, gesture recognition, and AR applications. In automotive systems, they enhance driver monitoring, collision avoidance, parking assistance, and autonomous navigation. In manufacturing and logistics, they enable robots and automated systems to detect obstacles, measure objects, and improve operational efficiency.

The technology is also gaining traction in healthcare, where 3D imaging assists in surgical planning, rehabilitation monitoring, prosthetic customization, and non-invasive diagnostics. As industries continue integrating AI and automation into operations, demand for high-precision spatial sensing technologies is expected to rise significantly.

Rising Consumer Demand for Immersive Experiences Driving Market Growth

One of the strongest drivers of the 3D camera market is the increasing consumer demand for immersive digital experiences. Consumers are rapidly adopting AR filters, VR gaming, spatial content creation, and interactive applications that rely heavily on depth-sensing technology.

Smartphone manufacturers are integrating advanced 3D sensors into flagship devices to improve camera performance and enable sophisticated biometric security systems. Features such as facial recognition, portrait mode photography, gesture-based controls, and AR applications have become key differentiators in premium consumer devices.

The growing popularity of social media platforms and content creation ecosystems is further contributing to the adoption of 3D cameras. Users increasingly seek professional-grade visual experiences, driving smartphone brands and electronics manufacturers to integrate advanced imaging capabilities into everyday devices.

Additionally, the expansion of spatial computing technologies and wearable AR/VR headsets is expected to create substantial opportunities for compact, low-power 3D sensing modules over the next decade.

AI and Edge Computing Accelerating Real-Time Depth Processing

Rapid advancements in artificial intelligence and edge computing are significantly enhancing the capabilities of 3D cameras. AI algorithms can now process depth information in real time, enabling accurate scene understanding, object tracking, gesture detection, and environmental mapping.

The integration of machine learning with 3D imaging allows devices to interpret spatial data more efficiently, reducing latency and improving user experience. This advancement is particularly important in robotics, autonomous systems, and industrial automation where split-second decisions are required.

High-performance GPUs, TPUs, and AI accelerators are making it possible to deploy advanced depth-sensing applications in compact and power-constrained devices such as drones, wearables, and mobile devices. As computing power continues to improve, 3D cameras are expected to become more affordable and widely accessible across multiple industries.

Time-of-Flight Technology Leading the Market

Among various technologies, Time-of-Flight (ToF) cameras dominate the market with more than 41% market share in 2026, valued at over US$ 2.6 billion.

y=6.4(1+0.173)xy = 6.4(1+0.173)^{x}y=6.4(1+0.173)x

ToF technology works by measuring the time taken for emitted light to reflect from surrounding objects and return to the sensor. This enables fast and highly accurate depth measurement with lower computational complexity compared to some alternative technologies.

ToF cameras are widely adopted because they perform effectively in low-light conditions and provide real-time depth sensing for smartphones, robotics, automotive systems, and industrial automation. Their compact design also makes them suitable for integration into slim consumer devices.

As industries increasingly prioritize automation and intelligent sensing, ToF technology is expected to maintain strong demand due to its scalability, speed, and precision.

Stereo Vision Emerging as a Fast-Growing Segment

Stereo vision or stereoscopic imaging is also witnessing rapid growth due to its cost-efficiency and compatibility with AI-driven computer vision systems.

This technology uses dual-camera systems similar to human eyesight to estimate depth by comparing differences between two images. Unlike some active sensing technologies, stereo vision does not rely heavily on external light projection, making it energy efficient and suitable for autonomous systems and robotics.

Industries adopting AI-powered automation are increasingly favoring stereo vision for applications such as autonomous navigation, warehouse robotics, industrial inspection, and smart surveillance. Continuous improvements in AI image processing and edge computing are further improving the accuracy and reliability of stereo vision systems.

Consumer Electronics Remains the Largest End-user Segment

Consumer electronics continues to dominate the global 3D camera market, accounting for over 26% share in 2026 and generating more than US$ 1.7 billion in revenue.

The widespread integration of 3D cameras into smartphones, tablets, gaming consoles, and AR/VR headsets is the primary factor driving this dominance. Consumers increasingly expect advanced features such as secure facial authentication, immersive gaming experiences, enhanced photography, and gesture recognition.

The rapid product upgrade cycle in the smartphone industry further boosts demand for compact and high-performance depth-sensing modules. Manufacturers are continuously investing in advanced imaging technologies to improve user experience and differentiate products in highly competitive markets.

The growth of spatial computing ecosystems and wearable technologies is also expected to create new opportunities for 3D camera integration in consumer devices.

Healthcare Emerging as a High-Growth Opportunity

Healthcare is expected to become one of the fastest-growing end-user segments in the 3D camera market over the forecast period.

Hospitals and medical device companies are increasingly deploying 3D imaging technologies for surgical planning, robotic-assisted procedures, rehabilitation monitoring, and patient diagnostics. Accurate depth perception enables surgeons and healthcare professionals to visualize anatomical structures more effectively, improving treatment precision and patient outcomes.

The growing adoption of telemedicine and remote patient monitoring is also contributing to market expansion. 3D cameras enable accurate body scanning, motion tracking, posture analysis, and rehabilitation assessment without physical contact.

Additionally, rising demand for customized prosthetics and minimally invasive surgeries is creating strong demand for advanced 3D visualization technologies across healthcare environments.

Asia Pacific Leading the Global Market

Asia Pacific holds the largest share of the global 3D camera market, accounting for more than 38% share in 2026 with a market value of approximately US$ 2.4 billion.

The region’s leadership is primarily driven by its strong electronics manufacturing ecosystem, large-scale smartphone production, and expanding semiconductor capabilities. Countries such as China, Japan, South Korea, and India are playing crucial roles in regional growth.

China remains a major manufacturing hub for 3D sensors, VCSEL components, and imaging modules, supported by government initiatives aimed at strengthening domestic semiconductor production. Japan contributes significantly through innovations in optics and imaging technologies, while South Korea continues advancing consumer-focused 3D imaging applications.

India’s rapidly expanding smartphone user base and growing digital economy are also accelerating demand for embedded 3D camera modules in mobile devices and smart applications.

North America Driving Innovation in Computer Vision

North America is expected to witness significant growth due to strong investments in AI, computer vision, semiconductor innovation, and autonomous systems.

The United States leads regional development with major technology companies investing heavily in depth-sensing technologies for automotive automation, robotics, spatial computing, and industrial AI applications. Government initiatives supporting autonomous vehicle infrastructure and smart manufacturing are further boosting adoption.

The region also benefits from advanced R&D ecosystems, strong venture capital funding, and increasing deployment of AI-powered automation across industries. As enterprises continue integrating intelligent sensing into operations, demand for advanced 3D imaging systems is expected to remain robust.

Europe Strengthening Industrial and Automotive Adoption

Europe continues to play a major role in the global 3D camera market due to its strong automotive and industrial automation sectors.

Countries such as Germany are leading adoption through advanced manufacturing facilities and automotive innovation programs. Automakers increasingly rely on 3D vision systems for robotic assembly lines, vehicle perception, and autonomous driving technologies.

The European Union’s strong focus on AI research, smart infrastructure, and industrial digitization is further supporting market expansion. Regulatory frameworks emphasizing privacy-centric biometric technologies are also encouraging the adoption of secure 3D sensing solutions across public and commercial applications.

Challenges Limiting Wider Adoption

Despite strong growth potential, several challenges continue to affect the broader adoption of 3D camera technologies.

One major barrier is the high system cost associated with advanced 3D sensing solutions. Components such as specialized sensors, optics, illumination modules, and processors increase manufacturing costs, particularly for small and mid-sized OEMs.

Integration complexity also remains a challenge. Technologies such as structured light and ToF require careful calibration to maintain depth accuracy and performance reliability. Many lower-cost devices still rely on software-based depth estimation using conventional 2D cameras due to budget constraints.

Environmental limitations also affect performance. Stereo vision systems can struggle with low-texture surfaces, while structured light technologies may perform poorly in strong ambient lighting conditions. These constraints make it necessary for manufacturers to carefully match technologies with specific use cases.

Competitive Landscape and Industry Developments

The global 3D camera market is moderately consolidated, with leading electronics and semiconductor companies investing heavily in innovation and product development.

Major companies are focusing on sensor miniaturization, improved depth accuracy, AI integration, and low-power processing technologies to strengthen market positioning. Emerging business models centered around digital twins, spatial mapping, and AI-driven imaging platforms are also creating new revenue opportunities.

Key companies operating in the market include:

- Sony Group Corporation

- Samsung Electronics Co., Ltd.

- Intel Corporation

- Panasonic Holdings Corporation

- Canon Inc.

- Fujifilm Holdings Corporation

- Ricoh Company Ltd.

- Nikon Corporation

- LG Corporation

- GoPro Inc.

- Matterport Inc.

- Texas Instruments

Recent developments further highlight the market’s innovation momentum. In June 2025, Sony Semiconductor Solutions introduced the IMX479 stacked direct Time-of-Flight SPAD depth sensor for automotive LiDAR systems, enabling high-resolution depth measurement for ADAS and autonomous driving applications.

In February 2025, CoStar Group completed the acquisition of Matterport to strengthen AI-powered property visualization and digital twin capabilities, signaling the growing importance of spatial imaging technologies in commercial real estate and enterprise applications.

Future Outlook

The future of the 3D camera market looks highly promising as industries increasingly transition toward intelligent automation, immersive digital experiences, and AI-driven machine interaction.

The convergence of AI, edge computing, robotics, AR/VR, spatial computing, and autonomous systems will continue driving demand for real-time depth sensing technologies. As sensor costs decline and processing efficiency improves, 3D cameras are expected to become standard components across consumer electronics, industrial systems, healthcare devices, and smart infrastructure.

With rapid innovation and expanding cross-industry applications, 3D cameras are poised to become one of the foundational technologies powering the next generation of intelligent digital ecosystems.