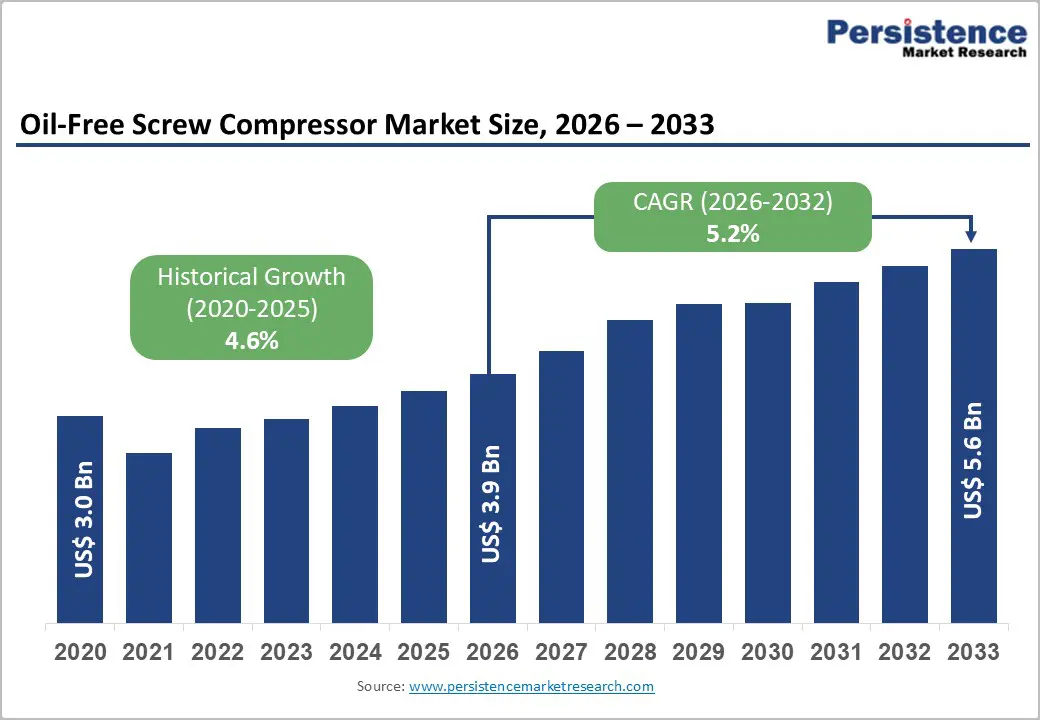

The global oil-free screw compressor market is entering a strong growth phase as industries increasingly prioritize contamination-free air systems, energy efficiency, and compliance with strict global quality standards. Valued at approximately US$ 3.9 billion in 2026, the market is projected to reach US$ 5.6 billion by 2033, expanding at a CAGR of 5.2% during the forecast period.

This steady expansion is driven by tightening regulatory frameworks such as ISO 8573-1 Class 0 certification, rising demand from high-purity manufacturing industries, and accelerating adoption of smart, energy-optimized compressor systems aligned with Industry 4.0 transformation.

Market Overview

Oil-free screw compressors are increasingly becoming essential in industries where even minimal contamination can lead to major operational failures or product recalls. Unlike oil-injected systems, oil-free compressors eliminate the risk of oil contamination in compressed air, making them indispensable in:

- Pharmaceuticals

- Food and beverage processing

- Semiconductor manufacturing

- Electronics and precision engineering

- Medical device production

The market is further strengthened by the global shift toward sustainable manufacturing practices, energy-efficient industrial equipment, and digitalized production environments.

Key Market Drivers

- Strict Regulatory Standards and Zero-Contamination Requirements

One of the most powerful growth drivers is the global enforcement of ISO 8573-1 Class 0 standards, which mandate zero oil content in compressed air for critical applications. Industries such as pharmaceuticals and food processing now operate under non-negotiable compliance frameworks where contamination risk is unacceptable.

Pharmaceutical manufacturers require ultra-clean air for drug formulation and sterile production environments, while food and beverage companies depend on oil-free systems to ensure hygiene and consumer safety.

Similarly, semiconductor fabrication facilities—where microscopic contamination can disrupt entire production batches—are heavily reliant on oil-free screw compressors to maintain air purity standards.

Additionally, environmental and workplace safety regulations driven by agencies like OSHA and the European Union’s environmental directives further reinforce adoption across developed economies.

- Energy Efficiency and Smart Manufacturing Integration

Modern oil-free screw compressors offer 15–20% higher energy efficiency compared to traditional systems. With rising global energy costs, this efficiency advantage significantly reduces operational expenditure.

A key innovation accelerating adoption is Variable Speed Drive (VSD) technology, which can reduce energy consumption by up to 35% by adjusting motor speed according to real-time demand.

Manufacturers such as Atlas Copco AB and Ingersoll Rand Inc. are integrating IoT-enabled monitoring systems that allow predictive maintenance, remote diagnostics, and performance optimization.

These smart systems align with Industry 4.0 strategies by integrating compressors into digital manufacturing ecosystems, reducing downtime and improving asset lifecycle management.

- Expansion of High-Purity Industrial Applications

Rapid industrialization in emerging economies, especially in Asia Pacific, is driving demand across:

- Chemical processing plants

- Oil and gas refining

- Power generation

- Electronics manufacturing

The need for uninterrupted, contamination-free compressed air in continuous production environments ensures strong long-term adoption of oil-free systems.

Market Restraints

High Capital Investment

Oil-free screw compressors require significantly higher upfront investment compared to oil-injected systems. Advanced technologies such as VSD drives, IoT sensors, and precision components increase total installation costs.

This creates a barrier for small and medium-sized enterprises (SMEs), especially in developing economies where capital expenditure decisions are highly cost-sensitive.

Technical Complexity and Maintenance Needs

Despite long-term efficiency benefits, oil-free systems require specialized technical expertise for installation and maintenance. In regions with limited skilled workforce availability, this can slow adoption rates.

Supply Chain Volatility

Global disruptions in raw material supply chains and component manufacturing have also affected production timelines and increased equipment costs in recent years.

Key Market Opportunities

Hydrogen Economy and Renewable Energy Expansion

One of the most promising opportunities lies in the global transition toward clean energy. Hydrogen production—especially via electrolysis—requires ultra-clean, oil-free compressed air systems.

Asia Pacific hydrogen capacity is expected to grow nearly fivefold by 2030, creating substantial demand for oil-free compressors as foundational infrastructure.

Companies such as Mitsubishi Heavy Industries are already deploying oil-free compressor systems in hydrogen and energy transition projects, validating commercial viability in this emerging sector.

Smart Factory and Industry 4.0 Expansion

The rise of smart factories is creating demand for connected compressor systems integrated with:

- AI-based predictive maintenance

- Cloud-based monitoring platforms

- ERP and MES integration

Manufacturers like Kaeser Kompressoren and Boge Compressors are focusing on digitalization strategies to enhance operational intelligence and customer value.

Market Segmentation Analysis

By Product Type

Stationary oil-free screw compressors dominate the market with nearly 70% installation share, driven by their reliability and suitability for continuous industrial operations.

These systems are widely used in large-scale facilities such as manufacturing plants, pharmaceutical units, and food processing industries.

By Stage Type

Single-stage compressors account for approximately 60% of the market, primarily due to their lower cost, simpler design, and ease of maintenance.

They are widely adopted in SMEs and applications requiring moderate pressure levels.

By Power Rating

- Below 15 kW systems dominate SME applications and account for over 50% of installations

- 55–160 kW systems represent the fastest-growing segment with a 10.5% CAGR, driven by heavy industrial applications

This growth is strongly supported by petrochemical, refining, and power generation industries requiring high-capacity air systems.

By End-Use Industry

Food & Beverage

The food and beverage sector remains the largest end-user, driven by stringent hygiene regulations and rising packaged food consumption. Oil-free air is essential in bottling, packaging, and processing operations.

Pharmaceuticals

The pharmaceutical sector accounts for nearly 35.8% of demand in 2026, as sterile manufacturing environments require contamination-free compressed air systems.

Electronics & Semiconductors

Precision manufacturing in semiconductor fabrication is another key driver, especially in Asia Pacific and North America.

Regional Analysis

Asia Pacific – Market Leader

Asia Pacific holds over 52% global market share, driven by manufacturing dominance in China and rapid pharmaceutical expansion in India.

China contributes nearly 40.5% of regional demand, supported by its semiconductor and industrial manufacturing base. Meanwhile, India is emerging as a high-growth hub due to pharmaceutical production leadership and government initiatives like “Make in India.”

North America – Fastest Growing Region

North America is expected to grow at a 7.1% CAGR, supported by strict occupational safety standards and advanced semiconductor manufacturing ecosystems.

The U.S. leads regional demand due to strong adoption of energy-efficient industrial systems and advanced automation technologies.

Europe – Technology-Driven Market

Europe remains a mature but innovation-focused market. Germany leads regional development through advanced engineering companies and strong regulatory compliance frameworks.

Companies such as CompAir and Sullair LLC contribute significantly to technological advancement in oil-free compressor systems.

Competitive Landscape

The global oil-free screw compressor market is moderately consolidated, with major players focusing on innovation, energy efficiency, and digital integration.

Key players include:

- Atlas Copco AB

- Ingersoll Rand Inc.

- Gardner Denver Holdings

- Kaeser Kompressors

- Hitachi Industrial Equipment Systems

- Mitsubishi Heavy Industries

- Kobelco Compressors

- Anest Iwata

These companies compete primarily through:

- Energy-efficient compressor design

- IoT-enabled predictive maintenance systems

- Expansion into hydrogen and renewable energy applications

- Strategic mergers and global distribution expansion

Recent innovations include next-generation oil-free scroll and rotary screw compressors optimized for semiconductor, pharmaceutical, and clean energy sectors.

Recent Industry Developments

- New oil-free scroll compressors launched for semiconductor applications with improved efficiency and reliability

- Advanced VSD-based screw compressors introduced to reduce lifecycle energy costs

- Expansion of double-stage oil-free systems certified for ISO Class 0 compliance

These developments highlight the industry’s strong focus on sustainability and precision engineering.

Conclusion

The oil-free screw compressor market is undergoing a structural transformation driven by strict regulatory standards, rising demand for contamination-free industrial processes, and rapid technological advancements in energy-efficient and smart manufacturing systems.

With increasing adoption across pharmaceuticals, food processing, semiconductors, and emerging hydrogen energy infrastructure, the market is expected to maintain stable and sustainable growth through 2033.

As industries continue shifting toward clean, automated, and digitally connected production environments, oil-free screw compressors will remain a critical enabler of industrial reliability, safety, and efficiency.