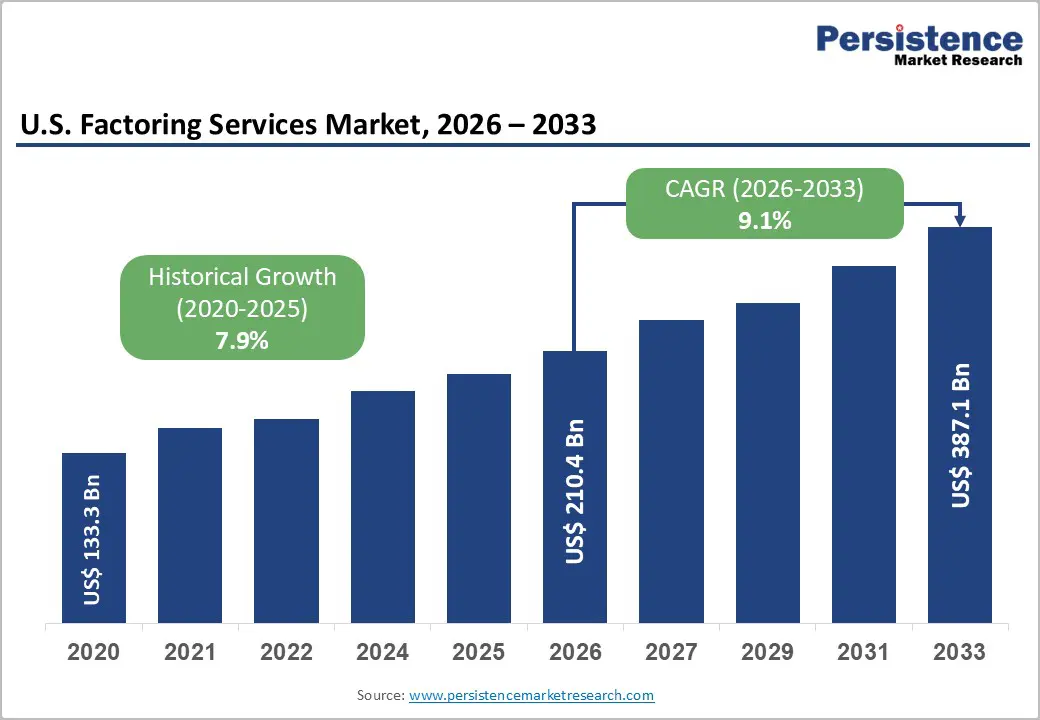

The U.S. factoring services market is entering a period of significant expansion as businesses increasingly seek flexible and accessible financing solutions. Valued at US$ 210.4 billion in 2026, the market is projected to reach US$ 387.1 billion by 2033, registering a CAGR of 9.1% during the forecast period. The industry's growth is being driven by rising demand for alternative working-capital solutions among small and medium-sized enterprises (SMEs), technological advancements in receivables financing, and the increasing complexity of domestic and international trade transactions.

Factoring services provide businesses with immediate cash by purchasing outstanding invoices at a discount, helping organizations improve liquidity without taking on traditional debt. As economic uncertainty, stricter bank lending standards, and cash flow challenges continue to impact businesses across sectors, factoring has emerged as a critical financial tool for maintaining operational continuity and supporting growth.

SMEs Drive Market Expansion Through Growing Demand for Alternative Financing

One of the most influential drivers of the U.S. factoring services market is the persistent financing gap faced by SMEs. Traditional lenders have tightened credit requirements in recent years, making it increasingly difficult for smaller businesses to secure working capital through conventional loans. Many companies struggle to meet collateral requirements or maintain the credit scores necessary for bank financing.

Factoring offers a practical alternative because financing decisions are primarily based on the creditworthiness of customers who owe the invoices rather than the financial profile of the borrowing business. This makes factoring especially attractive for startups, rapidly growing companies, and businesses operating in industries with long payment cycles.

The United States is home to more than 33 million SMEs, representing a substantial portion of economic activity and employment. These businesses routinely face payment terms ranging from 30 to 90 days, creating ongoing liquidity challenges. Factoring enables them to convert accounts receivable into immediate cash, helping cover payroll, inventory purchases, equipment maintenance, and expansion initiatives.

As awareness of alternative financing options continues to grow, factoring providers are increasingly targeting underserved SME segments through specialized products, digital platforms, and faster approval processes.

Digital Transformation Reshaping the Factoring Industry

Technology is fundamentally transforming how factoring services are delivered across the United States. Artificial Intelligence (AI), Machine Learning (ML), Natural Language Processing (NLP), and blockchain-enabled Distributed Ledger Technology (DLT) are streamlining operations and improving risk management.

Traditionally, invoice verification, credit checks, and funding approvals could take several days. Modern AI-powered systems can analyze invoices, assess risk, detect fraud, and approve funding requests within hours. This dramatic improvement in processing speed is enhancing customer experiences and expanding market accessibility.

Blockchain technology is also gaining traction as a tool for improving transparency and security within receivables financing. By creating immutable transaction records, blockchain solutions help reduce invoice duplication, fraud risks, and reconciliation errors. Large enterprises and financial institutions are increasingly exploring DLT-based systems to strengthen trust and efficiency throughout supply chains.

The growing integration of factoring services into cloud-based accounting platforms and enterprise resource planning (ERP) systems is another important development. Embedded finance solutions now allow businesses to access factoring directly from the software they use daily, creating a seamless financing experience and reducing administrative burdens.

Rising Cross-Border Trade Creates New Opportunities

Globalization continues to create significant opportunities for U.S. factoring providers. International trade increasingly relies on open-account payment terms, which expose exporters and importers to extended payment cycles and credit risks. Factoring services help businesses mitigate these challenges by providing immediate liquidity and managing collection processes.

As global supply chains evolve and manufacturing activity shifts across regions, demand for international factoring solutions is expected to accelerate. U.S.-based companies engaging in cross-border transactions require financing partners capable of managing multi-currency settlements, foreign debtor risks, and international regulatory compliance.

Digital-first factoring platforms are particularly well positioned to capitalize on this trend. Advanced technologies enable faster onboarding, real-time transaction monitoring, and streamlined documentation processes, making international factoring more efficient and accessible than ever before.

The growing adoption of global factoring networks further strengthens opportunities by facilitating cooperation among factors across multiple countries and improving support for exporters and importers engaged in international trade.

High Costs Remain a Challenge for Market Adoption

Despite its advantages, factoring remains a relatively expensive financing option compared to traditional bank loans and credit lines. Factoring fees typically range from 1.5% to 5% of invoice value per month, depending on industry, debtor quality, transaction volume, and service structure.

For businesses operating with narrow profit margins, these costs can significantly impact profitability. Micro-enterprises, in particular, may find factoring fees difficult to justify unless cash flow challenges are severe enough to outweigh the expense.

Cost concerns are especially prominent in industries such as retail, hospitality, and food services, where margins are often limited and financing needs fluctuate seasonally. As a result, many smaller firms continue to rely on internal funding sources or delay seeking external capital.

To address these challenges, providers are increasingly leveraging automation and digital workflows to reduce operational costs and offer more competitive pricing structures.

Regulatory Complexity Continues to Influence Market Development

Another factor affecting market growth is the fragmented regulatory environment governing factoring transactions in the United States. Unlike banking activities, which are regulated through centralized federal frameworks, factoring operates under various state-level regulations and Uniform Commercial Code (UCC) provisions.

This regulatory diversity creates compliance challenges for providers operating across multiple jurisdictions. International factoring transactions often involve additional legal and administrative complexities, increasing operational costs and extending transaction timelines.

The absence of a unified national regulatory framework can discourage standardization and limit scalability for some providers. However, industry participants continue to advocate for greater harmonization and modernization of receivables financing regulations to support broader market development.

Healthcare Emerges as a High-Growth Vertical

Healthcare is expected to become one of the fastest-growing segments within the U.S. factoring services market. Hospitals, physician practices, home healthcare providers, and medical staffing agencies frequently encounter lengthy reimbursement cycles associated with insurance claims, Medicare, and Medicaid payments.

These delays can create significant cash flow challenges, particularly for smaller healthcare organizations managing labor-intensive operations. Factoring services provide a valuable solution by converting outstanding receivables into immediate working capital.

Non-recourse factoring is especially attractive within healthcare because it transfers credit risk from the provider to the factoring company. This arrangement offers greater financial security and predictability, helping healthcare organizations focus on patient care rather than payment collection.

The increasing complexity of healthcare reimbursement systems further supports demand for specialized factoring solutions incorporating advanced analytics, denial management tools, and automated claims monitoring capabilities.

Domestic Factoring Dominates Market Activity

Domestic factoring remains the largest category within the U.S. market, accounting for approximately 77% of total industry activity. This dominance reflects the country's well-developed financial infrastructure, strong legal framework, and widespread adoption of electronic invoicing systems.

Industries such as transportation, manufacturing, staffing, and wholesale distribution generate substantial volumes of domestic receivables that are well suited for factoring. Improved visibility into invoice ownership and debtor information further supports efficient transaction processing.

As digital technologies continue to reduce onboarding costs and enhance operational efficiency, domestic factoring providers are expected to expand their reach among SMEs and mid-sized businesses throughout the forecast period.

Recourse Factoring Maintains Market Leadership

Recourse factoring continues to represent the majority of market revenues, accounting for approximately 77% of total activity. Under this structure, businesses retain responsibility for unpaid invoices if customers fail to make payments.

Because the factor assumes lower risk, recourse arrangements generally offer lower fees than non-recourse alternatives. This pricing advantage makes them particularly appealing to companies with established customer bases and predictable payment histories.

Industries such as transportation, manufacturing, and staffing frequently utilize recourse factoring due to the relatively stable credit profiles of their customers. While recourse factoring remains dominant, non-recourse offerings are experiencing faster growth as businesses seek greater protection against credit risk and economic uncertainty.

Transportation and Logistics Lead Industry Demand

Transportation and logistics represent the largest end-use sector for factoring services, accounting for roughly one-third of total market demand. The industry's business model naturally creates a need for rapid access to working capital.

Trucking companies, freight carriers, and logistics providers often experience payment delays of 30 to 90 days while simultaneously managing immediate operating expenses, including fuel costs, driver wages, insurance premiums, and equipment maintenance.

Factoring bridges this cash flow gap by providing same-day funding against approved invoices. Specialized transportation factors have developed industry-specific services, including fuel advances, freight payment solutions, and collections support, creating comprehensive ecosystems that strengthen customer relationships.

As freight volumes continue to grow and supply chains become increasingly complex, transportation is expected to remain a cornerstone of factoring market demand.

Competitive Landscape and Future Outlook

The U.S. factoring services market features a mix of large bank-owned factors, independent specialists, and rapidly emerging fintech companies. Major financial institutions benefit from extensive capital resources, broad customer networks, and integrated treasury management capabilities.

Meanwhile, independent factors differentiate themselves through sector expertise, customized service offerings, and flexible underwriting approaches. Fintech entrants are disrupting traditional business models through AI-powered risk assessment, automated onboarding, and embedded finance solutions.

Strategic acquisitions, technology partnerships, and platform integrations are becoming increasingly common as providers seek scale, efficiency, and competitive differentiation. The adoption of blockchain, AI-driven credit analytics, and real-time payment technologies is expected to further transform the market over the coming years.

Looking ahead, the U.S. factoring services market is positioned for sustained growth through 2033. Expanding SME financing needs, increasing digitalization, healthcare receivables opportunities, and rising cross-border trade activity will continue to support market expansion. Providers that successfully combine technological innovation with industry-specific expertise are likely to emerge as long-term leaders in this evolving financial services landscape.