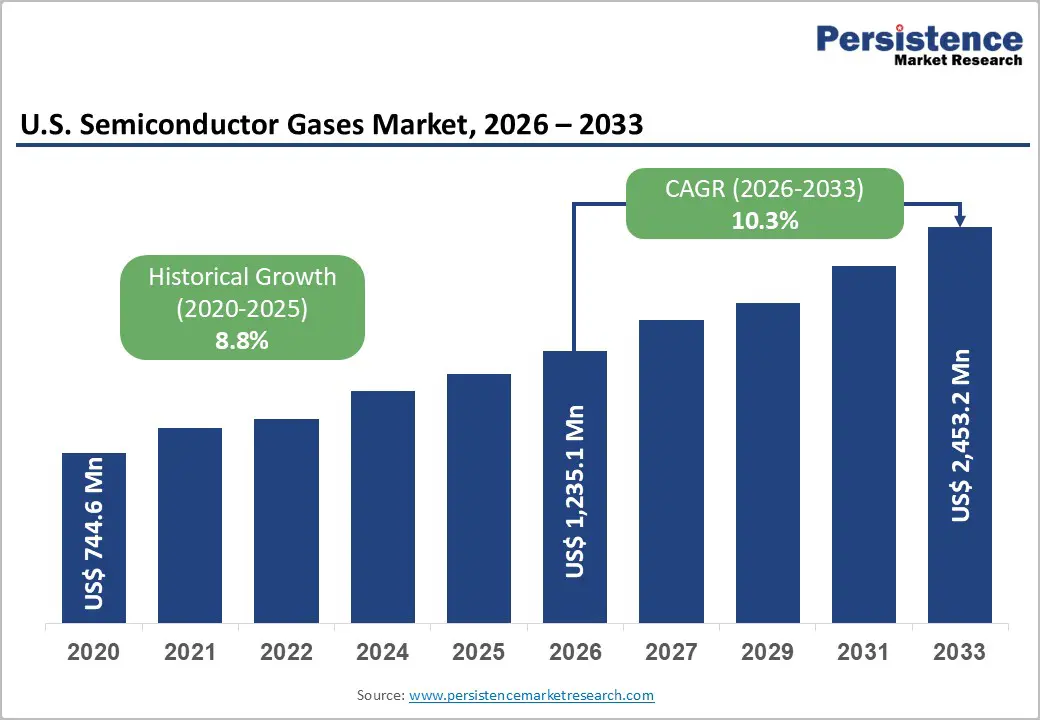

The U.S. semiconductor gases market is entering a structurally transformative growth phase, underpinned by large-scale federal incentives, rapid expansion of domestic chip fabrication capacity, and accelerating demand from AI-driven semiconductor production. Valued at US$ 1,235.1 million in 2026, the market is projected to reach US$ 2,453.2 million by 2033, expanding at a strong CAGR of 10.3% during the forecast period.

This growth is not cyclical—it is structural. The combination of the CHIPS and Science Act, advanced node migration (3nm, 2nm, and below), and the increasing gas intensity of semiconductor manufacturing is fundamentally reshaping demand for both bulk gases and electronic specialty gases (ESGs) across the United States.

Market Overview: A Critical Enabler of Semiconductor Manufacturing

Semiconductor gases are essential inputs used throughout wafer fabrication, including deposition, etching, cleaning, doping, and chamber maintenance processes. These gases—ranging from high-volume nitrogen and argon to ultra-high-purity fluorinated compounds—are indispensable for achieving nanoscale precision in modern chip manufacturing.

As semiconductor architectures become more complex (FinFET to Gate-All-Around and 3D NAND scaling beyond 200 layers), gas consumption per wafer increases significantly. Advanced fabs today can use 10–15 times more specialty gases per wafer pass compared to mature-node facilities.

This structural intensity is a key driver of long-term demand growth across U.S. semiconductor manufacturing hubs.

Key Growth Drivers

- CHIPS and Science Act: Reshoring Semiconductor Manufacturing

The CHIPS and Science Act of 2022, which allocates US$ 52.7 billion in federal support, has triggered the largest semiconductor manufacturing expansion in U.S. history. Major investments include fabs by TSMC, Intel, Samsung, and Micron across Arizona, Ohio, Texas, and New York.

Each new fabrication facility represents a multi-decade gas demand center. Advanced fabs require continuous supply of ultra-high-purity nitrogen, hydrogen, oxygen, and argon, along with specialty gases for lithography, etching, and deposition processes.

Companies such as Air Products and Chemicals Inc. have already secured long-term on-site gas supply contracts with leading CHIPS Act beneficiaries, reinforcing the direct link between federal policy and industrial gas demand growth.

- AI Chip Boom and Advanced Node Transition

The rapid global expansion of artificial intelligence infrastructure is accelerating demand for advanced semiconductor chips manufactured at sub-5nm nodes. GPUs such as NVIDIA’s H100 and B200 series, along with AMD’s MI300 accelerators, require extremely complex fabrication processes.

These advanced nodes rely heavily on Electronic Special Gases (ESGs) such as silane, ammonia, nitrogen trifluoride, and fluorocarbon compounds. These gases are used in atomic layer deposition (ALD), chemical vapor deposition (CVD), and plasma etching processes.

As a result, ESG consumption per wafer continues to rise sharply, making this the fastest-growing segment of the semiconductor gases market.

- Rising Complexity of Semiconductor Manufacturing

The transition toward Gate-All-Around (GAA) transistors and 3D NAND memory scaling beyond 200 layers has significantly increased process complexity. Each wafer now undergoes over 100 deposition-etch cycles, each requiring highly specialized gas chemistries.

This complexity directly translates into higher consumption of both bulk gases and ESGs, reinforcing long-term demand growth.

Market Restraints

- Helium Supply Constraints

One of the most critical challenges facing the industry is helium scarcity. Helium is essential for cooling systems, carrier gas applications, and analytical equipment in fabs. However, global supply is highly concentrated in regions such as Qatar, Russia, and the United States.

Geopolitical disruptions—such as supply constraints linked to Russia—have already caused price volatility in helium markets. The partial restructuring of the U.S. Federal Helium Reserve has further added uncertainty to long-term supply stability.

- Ultra-High Purity Requirements and Supply Rigidity

Semiconductor manufacturing requires gases with purity levels of 99.9999% (6N) or higher, often with impurity thresholds measured in parts per trillion.

These stringent requirements result in long qualification cycles (6–18 months) for any new gas supplier. Once qualified, switching suppliers becomes extremely difficult, creating structural rigidity in the supply chain and limiting competitive flexibility.

Organizations such as Solvay and Electronic Fluorocarbons LLC operate in this high-barrier ESG segment, where precision manufacturing and traceability are critical.

Market Opportunities

- On-Site Gas Generation Models

One of the most significant opportunities lies in on-site gas production facilities integrated directly into semiconductor fabs. Instead of transporting gases over long distances, suppliers build dedicated gas plants adjacent to fabrication sites.

This model ensures uninterrupted supply, reduces logistics complexity, and creates long-term contractual revenue streams (typically 10–20 years).

Companies such as Messer SE and Co. KGaA and Taiyo Nippon Sanso JFP Corporation are actively expanding their on-site gas infrastructure capabilities to serve CHIPS Act-funded fabs.

- Next-Generation Electronic Specialty Gas Development

As chip geometries shrink further, traditional gas chemistries are reaching performance limits. This creates opportunities for next-generation ESG formulations tailored for:

- GAA transistor architectures

- Advanced EUV lithography processes

- High-aspect-ratio etching in 3D NAND

- Ultra-selective deposition processes

Specialty materials companies such as Sumitomo Seika Chemicals Company Ltd. and REC Silicon ASA are investing heavily in advanced gas chemistry innovation to meet these evolving requirements.

- Green Hydrogen and Clean Energy Integration

A growing opportunity is the integration of semiconductor gas production with green hydrogen infrastructure. On-site hydrogen generation not only supports semiconductor processes but also aligns with broader decarbonization goals.

This creates a dual-revenue opportunity for gas suppliers serving both industrial and energy transition markets.

Market Segmentation Insights

By Gas Type

- Bulk gases (dominant segment, ~62% share):

Includes nitrogen, argon, oxygen, hydrogen, and helium. Nitrogen alone accounts for massive daily consumption in advanced fabs, often exceeding 50–100 tons per day. - Electronic Specialty Gases (fastest-growing, ~38% share):

Includes fluorocarbons, nitrogen trifluoride, silane, and ammonia. Demand is rising rapidly due to advanced node manufacturing complexity.

By Process

- Etching (largest segment, ~30% share):

The most gas-intensive process, requiring multiple fluorinated gases for plasma etching. - Deposition (~25% share):

Driven by CVD and ALD processes essential for advanced chip layering.

Etching and deposition together form the backbone of semiconductor gas consumption.

Regional Analysis

West United States (Market Leader)

The West U.S., including Arizona, California, and Oregon, dominates the semiconductor gases market. This region is anchored by:

- TSMC’s Arizona fabs

- Intel’s Oregon manufacturing complex

- Micron’s existing fabrication footprint

Arizona, in particular, has emerged as the most important new semiconductor manufacturing hub in the country.

Midwest United States (Fastest Growing)

The Midwest, led by Ohio, is witnessing unprecedented growth due to Intel’s massive investment in its New Albany semiconductor campus. This project alone represents up to US$ 100 billion in long-term investment, creating one of the world’s largest emerging chip manufacturing clusters.

Southwest United States

Texas and surrounding states are becoming critical semiconductor manufacturing zones, driven by Samsung’s Taylor fab and Texas Instruments’ expanding production footprint. This region is rapidly evolving into a secondary semiconductor hub alongside Arizona.

Competitive Landscape

The U.S. semiconductor gases market is moderately consolidated at the top, with a few global leaders dominating supply.

Key players include:

- Air Products and Chemicals Inc.

- Messer SE and Co. KGaA

- Taiyo Nippon Sanso JFP Corporation

- Solvay

- REC Silicon ASA

- Electronic Fluorocarbons LLC

Competition is primarily based on:

- On-site gas infrastructure capability

- Purity and traceability standards

- Long-term supply agreements

- Engineering support at fab level

- CHIPS Act compliance and supply chain localization

Recent Industry Developments

- Expansion of on-site gas supply agreements linked to TSMC Arizona’s next-phase fabs

- Restart and expansion of domestic silane production to support supply chain independence

- Capacity expansions in specialty fluorocarbon production to support advanced etching processes

- Increased investment in digital gas monitoring and purity traceability systems

Conclusion

The U.S. semiconductor gases market is evolving into a strategically critical infrastructure segment at the heart of America’s semiconductor renaissance. With demand rising from US$ 1.23 billion in 2026 to US$ 2.45 billion by 2033, the industry is being reshaped by three powerful forces: federal industrial policy, AI-driven chip demand, and the transition to extreme-scale semiconductor manufacturing.

As fabs become larger, more complex, and more gas-intensive, semiconductor gases are no longer just industrial inputs—they are becoming mission-critical enablers of national technological competitiveness.