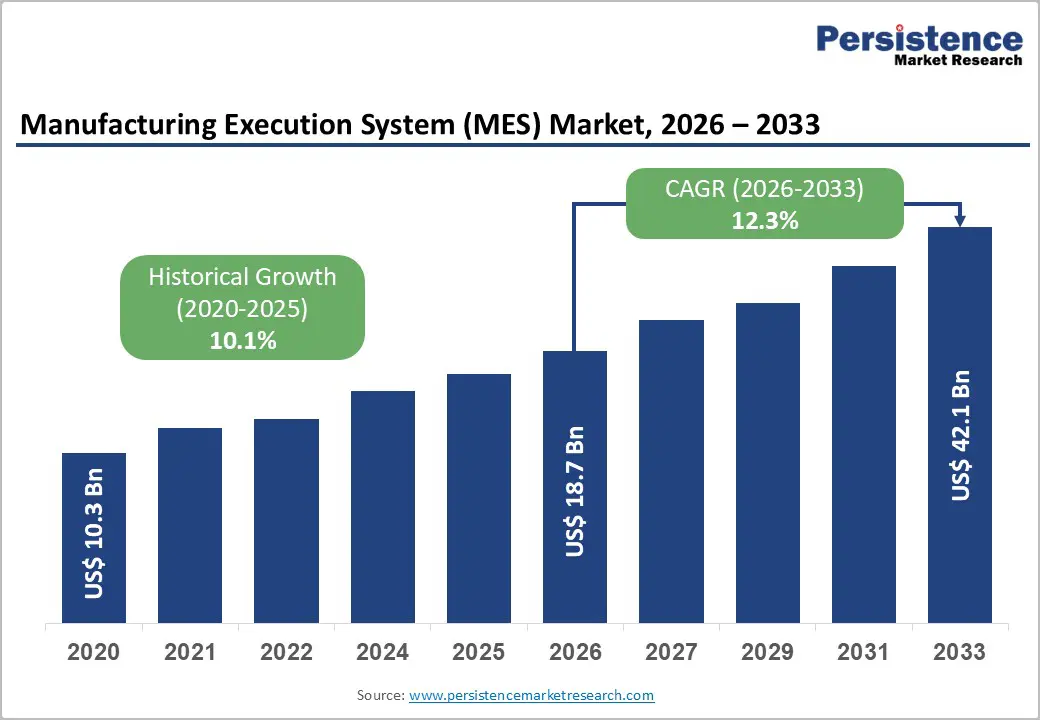

The global Manufacturing Execution System (MES) market is entering a strong growth phase as manufacturers accelerate digital transformation and transition toward smart factory ecosystems. Valued at US$18.7 billion in 2026, the market is projected to reach US$42.1 billion by 2033, expanding at a CAGR of 12.3% during the forecast period. This growth reflects the rising demand for real-time production monitoring, operational efficiency, and integrated manufacturing intelligence across industries.

As Industry 4.0 adoption deepens, MES platforms have become a foundational layer connecting enterprise planning systems with shop-floor operations. They enable manufacturers to achieve greater visibility, control, and optimization of production processes while ensuring compliance with increasingly strict quality and regulatory standards.

Market Overview

Manufacturing Execution Systems serve as the digital backbone of modern manufacturing environments. By bridging the gap between ERP (Enterprise Resource Planning) systems and industrial automation tools such as SCADA and PLCs, MES solutions provide real-time insights into production performance, resource utilization, and quality metrics.

Global manufacturing output continues to expand across automotive, electronics, pharmaceuticals, and food & beverage sectors. This sustained industrial growth, combined with increasing complexity in supply chains, has made MES adoption a strategic necessity rather than an optional upgrade.

Manufacturers are increasingly prioritizing:

- Real-time production visibility

- Reduced downtime and waste

- Predictive maintenance capabilities

- End-to-end traceability

- Compliance with regulatory frameworks

Key Market Highlights

The MES market is characterized by strong segmentation across components, deployment models, industries, and regions.

- Software Dominance: Accounts for over 65% share in 2026, valued at more than US$12.2 billion, driven by real-time analytics, process optimization, and ERP/PLM integration.

- Services Growth: Fastest-growing segment due to rising implementation complexity, customization needs, and lifecycle support requirements.

- On-Premises Deployment: Holds over 48% share (US$9.0 billion) due to security, compliance, and deep customization needs.

- Cloud/SaaS Growth: Rapid expansion driven by scalability, lower upfront costs, and seamless AI/IoT integration.

- Automotive Leadership: Largest industry segment with over 26% share (US$4.9 billion).

- Healthcare Expansion: Fastest-growing segment with a CAGR of 15.4%.

- North America Leadership: Holds over 36% share (US$6.7 billion).

- Asia Pacific Growth: Fastest-growing region with a CAGR of 16.9%.

Market Dynamics

Key Driver: Demand for Operational Efficiency

Manufacturers are under continuous pressure to reduce costs while improving productivity and product quality. MES solutions help streamline operations by minimizing errors, optimizing resource allocation, and improving production planning.

Studies indicate that digital transformation in manufacturing can improve productivity by 20–30%, making MES adoption a high-return investment. Integration with ERP and supply chain systems enables synchronized planning and execution, reducing inefficiencies across production lines.

This is especially critical in industries such as automotive and electronics, where even minor inefficiencies can lead to substantial financial losses.

Key Driver: Regulatory Compliance and Traceability

Industries such as pharmaceuticals, aerospace, food & beverage, and medical devices are subject to stringent regulatory requirements. MES platforms provide:

- Electronic batch records

- Audit trails

- Deviation management

- End-to-end product traceability

Regulatory frameworks such as FDA 21 CFR Part 11 and EU GMP Annex 11 require manufacturers to maintain accurate, tamper-proof production records. MES systems directly address these requirements, making them indispensable in regulated environments.

Market Restraint: High Implementation Complexity

Despite strong demand, MES deployment remains complex and capital-intensive. Costs include software licensing, infrastructure upgrades, customization, and workforce training.

Integration challenges with legacy systems such as SCADA, ERP, and PLC networks further increase deployment time and risk. Many manufacturers find that off-the-shelf solutions meet only 70–90% of requirements, necessitating expensive customization.

These barriers limit adoption, particularly among small and mid-sized enterprises.

Market Restraint: Cybersecurity Risks

As manufacturing systems become increasingly connected through IoT and cloud platforms, cybersecurity risks are rising significantly. Manufacturing is among the most targeted sectors for cyberattacks globally.

Reports suggest the sector could face losses of up to USD 9 billion annually due to cyber incidents. Over 85% of manufacturers report experiencing at least one cybersecurity breach per year.

This growing threat landscape increases investment in security infrastructure, slowing down MES adoption in cost-sensitive environments.

Market Opportunities

Artificial Intelligence and Predictive Analytics

AI integration is transforming MES platforms into intelligent production systems capable of predictive maintenance, quality forecasting, and workflow optimization.

Key benefits include:

- Up to 25% reduction in maintenance costs

- Nearly 30% reduction in unplanned downtime

- Improved product quality and defect detection

AI-powered MES solutions are particularly valuable in aerospace, semiconductor, and precision manufacturing sectors.

Digital Twin Integration

Digital twin technology enables virtual replication of manufacturing systems for simulation and optimization. When combined with MES, it allows manufacturers to:

- Test production scenarios virtually

- Optimize workflows in real time

- Reduce operational risks

- Improve efficiency and throughput

Industries such as automotive and industrial machinery are increasingly adopting digital twin-integrated MES platforms to enhance performance and profitability.

Segment Analysis

By Component

Software Segment:

The dominant category, accounting for over 65% of the market. MES software enables real-time production tracking, analytics, and integration with enterprise systems. Its scalability and ability to standardize operations across global facilities make it indispensable.

Services Segment:

The fastest-growing segment, driven by demand for consulting, integration, training, and maintenance. As MES platforms become more complex, organizations rely on external expertise for successful implementation and optimization.

By Deployment

On-Premises MES:

Holds the largest share due to high security requirements, regulatory compliance, and control over production data. Large manufacturers prefer this model for stability and customization.

Cloud/SaaS MES:

Experiencing rapid growth due to scalability, lower capital investment, and faster deployment. Cloud-based MES is particularly popular among SMEs and multi-site manufacturers.

By Industry

Automotive:

Largest segment with over 26% share. MES supports assembly line coordination, EV production, and quality assurance across complex supply chains.

Healthcare:

Fastest-growing segment with a CAGR of 15.4%, driven by regulatory requirements, personalized medicine, and the need for precise production tracking.

Other important sectors include electronics, aerospace, and food & beverage manufacturing.

Regional Analysis

North America

North America leads the global MES market with over 36% share. The U.S. remains the key driver, supported by advanced manufacturing infrastructure and early adoption of smart factory technologies.

Strict regulatory standards such as FDA compliance and AS9100 certifications reinforce MES adoption across industries including pharmaceuticals, aerospace, and electronics.

Asia Pacific

Asia Pacific is the fastest-growing region with a CAGR of 16.9%. Growth is driven by rapid industrialization and government initiatives such as:

- China’s Made in China 2025

- India’s Production Linked Incentive (PLI) scheme

- Expansion of SME manufacturing ecosystems

Countries like Japan, Vietnam, and South Korea are also accelerating MES adoption through automation and digital transformation.

Europe

Europe holds over 27% market share, led by Germany, France, and the UK. The Industrie 4.0 initiative continues to drive digital manufacturing adoption.

Sustainability regulations and carbon reporting requirements are further pushing manufacturers to adopt MES platforms for energy tracking and environmental compliance.

Competitive Landscape

The MES market is moderately consolidated, dominated by global technology leaders such as Siemens, Rockwell Automation, SAP, Honeywell, Schneider Electric, and Oracle.

Key competitive strategies include:

- Cloud-native MES platforms

- AI-driven analytics integration

- Low-code customization tools

- Ecosystem-based integration with ERP and PLM systems

Companies are increasingly offering subscription-based SaaS models to expand into SMEs and emerging markets.

Recent Developments

- December 2025: Rockwell Automation launched a cloud-native MES platform integrating AI analytics and OT-IT convergence capabilities.

- June 2025: Tieto introduced its SaaS-based TIPS MES on Microsoft Azure for process industries like pulp and paper, improving efficiency and reducing IT overhead.

Key Companies Covered

- Siemens AG

- Rockwell Automation

- SAP SE

- Dassault Systèmes

- ABB Ltd.

- Honeywell International Inc.

- Schneider Electric

- Oracle Corporation

- Emerson Electric Co.

- GE Vernova

- AVEVA Group plc

- Yokogawa Electric Corporation

- Körber AG

- Aspen Technology

Conclusion

The global Manufacturing Execution System (MES) market is poised for strong and sustained growth through 2033, driven by rapid industrial digitization, increasing regulatory pressure, and the rise of smart factories.

With the market expected to nearly double from US$18.7 billion in 2026 to US$42.1 billion in 2033, MES platforms are becoming essential infrastructure for modern manufacturing ecosystems. The integration of AI, cloud computing, and digital twin technologies will further redefine production efficiency, enabling manufacturers to achieve higher productivity, lower costs, and improved compliance in an increasingly competitive global landscape.