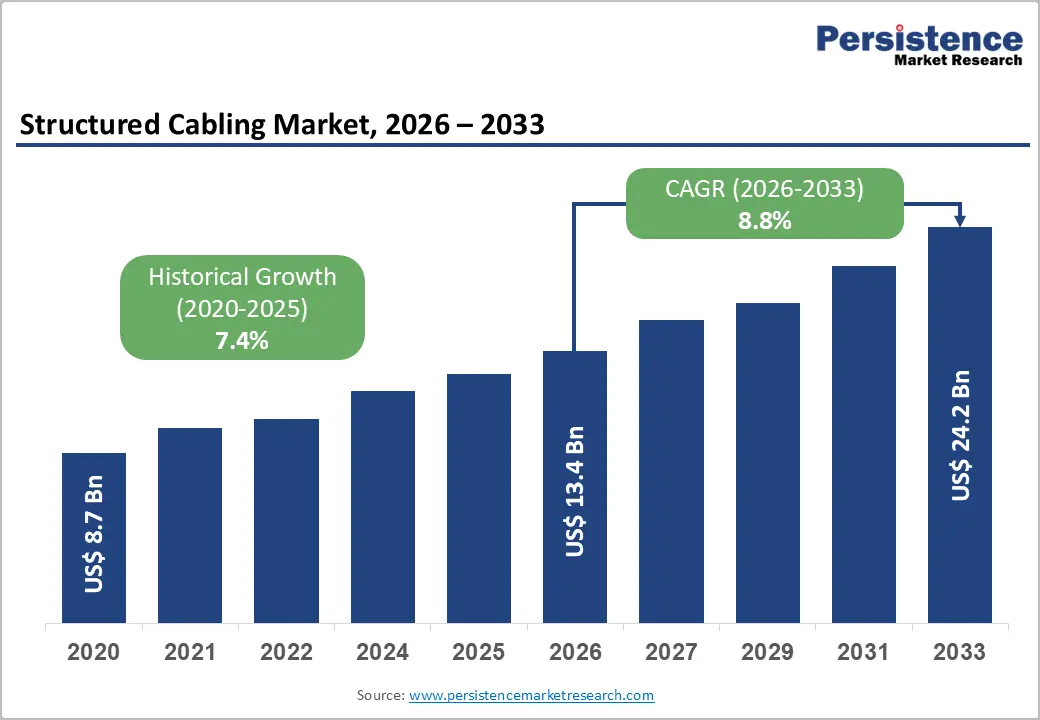

The global structured cabling market is undergoing a significant transformation, driven by rapid digital infrastructure expansion, accelerating data consumption, and the growing complexity of enterprise networks. Valued at US$ 13.4 billion in 2026, the market is projected to reach US$ 24.2 billion by 2033, expanding at a CAGR of 8.8% during the forecast period. This robust growth trajectory reflects the increasing dependence of modern economies on high-speed, reliable, and scalable network infrastructure that supports data centers, cloud computing, 5G networks, and IoT ecosystems.

Structured cabling serves as the foundational physical layer of modern communication systems. It enables seamless data transmission across enterprise buildings, campuses, data centers, and telecom networks. As digital transformation accelerates across industries such as IT & telecommunications, healthcare, BFSI, manufacturing, and government, structured cabling has become an indispensable enabler of connectivity and operational efficiency.

Market Overview and Growth Drivers

The structured cabling market is primarily being propelled by three major global forces: exponential data center expansion, widespread 5G deployment, and the rapid adoption of cloud computing and IoT technologies.

Hyperscale data centers are expanding at an unprecedented pace as global cloud service providers increase investments to meet rising demand for storage, computing, and AI-driven workloads. According to industry estimates, global data center construction spending exceeded US$ 400 billion between 2021 and 2024, reflecting the scale of infrastructure development underway. This expansion directly fuels demand for both fiber-optic and copper structured cabling systems that support high-density, low-latency connectivity.

The increasing adoption of artificial intelligence is further reshaping infrastructure requirements. AI-driven workloads require significantly higher bandwidth and interconnect density. Research indicates that AI-optimized data centers may require 10 times more fiber cabling compared to traditional facilities. This shift is accelerating the transition toward high-density fiber-optic structured cabling solutions capable of supporting 800G and future 1.6T network speeds.

Meanwhile, the global rollout of 5G networks is driving a parallel wave of infrastructure upgrades. With more than 40 countries having deployed commercial 5G services, telecom operators are investing heavily in small cell densification, edge computing nodes, and high-capacity backhaul networks. These developments are significantly increasing demand for structured cabling systems that ensure reliable and high-speed data transmission across distributed network architectures.

Additionally, the proliferation of smart buildings and Industry 4.0 environments is creating long-term structural demand. Modern buildings require integrated cabling systems that support not only IT networks but also security systems, HVAC automation, surveillance, and energy management solutions.

Market Restraints and Challenges

Despite strong growth prospects, the structured cabling market faces several constraints that may limit adoption, particularly among small and medium-sized enterprises.

One of the primary barriers is the high initial installation cost. Structured cabling systems require significant capital investment in materials, design, installation, and certification. In enterprise environments, costs can range between US$ 1,000 and US$ 5,000 per rack unit, depending on the complexity and performance requirements. This makes adoption challenging for budget-constrained organizations.

Another major challenge is the shortage of skilled professionals. Structured cabling installation requires certified technicians with expertise in standards such as ANSI/TIA-568.2-E. However, the industry continues to face a global labor gap. Studies suggest that nearly 70% of network failures are linked to physical layer issues, often resulting from improper installation practices.

This skills shortage is particularly acute in emerging markets, where rapid digital infrastructure expansion is not matched by workforce development. As a result, project delays, increased rework costs, and inconsistent installation quality continue to hinder market efficiency.

Key Market Opportunities

One of the most significant opportunities in the structured cabling market is the shift toward AI-ready and next-generation data centers. As hyperscale operators transition toward 800G and 1.6T optical networks, demand for high-density fiber solutions is accelerating rapidly.

Companies such as Corning and other leading manufacturers are developing pre-terminated fiber systems and modular cabling solutions designed specifically for AI data centers. These systems reduce installation time, improve scalability, and optimize space utilization within high-density server environments.

Another major opportunity lies in smart city and government-led infrastructure programs. In the United States alone, more than US$ 65 billion has been allocated toward broadband and telecommunications infrastructure under the Infrastructure Investment and Jobs Act. Similar initiatives in Europe and Asia Pacific are driving large-scale modernization of public buildings, transportation hubs, and municipal networks.

In emerging economies, government-led programs such as India’s BharatNet and China’s New Infrastructure initiative are significantly expanding broadband access and digital connectivity. These programs create sustained demand for structured cabling solutions across rural and urban infrastructure projects.

Market Segmentation Analysis

By Product Type

Copper cabling remains the dominant segment, accounting for approximately 49% of global market share. Its continued dominance is attributed to its cost-effectiveness and widespread adoption in enterprise LAN environments. Cat6A and Cat8 copper cables are widely used for short-to-medium range connections, particularly in office buildings and campuses.

Fiber-optic cabling, however, is rapidly gaining traction, especially in data center and backbone applications. While more expensive than copper, fiber offers significantly higher bandwidth, lower latency, and better scalability for future network requirements.

By Application

The Local Area Network (LAN) segment dominates the market, contributing nearly 81% of total demand. LAN infrastructure is essential in commercial buildings, educational institutions, healthcare facilities, and enterprise campuses.

The increasing adoption of Wi-Fi 6 and Wi-Fi 6E technologies is also reinforcing LAN demand, as these wireless systems require high-performance copper cabling for efficient backhaul connectivity.

By Vertical

The IT & telecommunications sector is the leading end-user, accounting for approximately 32% of the market share. This dominance is driven by large-scale data center expansion, telecom network upgrades, and enterprise IT modernization initiatives.

This segment is also expected to grow at the fastest CAGR of 9.7%, fueled by continuous investment in cloud infrastructure, 5G core networks, and hybrid IT environments.

Regional Analysis

North America

North America leads the global structured cabling market with approximately 34% market share. The region benefits from a dense concentration of hyperscale data centers, advanced enterprise IT infrastructure, and strong government support for broadband expansion.

The United States remains the dominant country, driven by major data center hubs such as Northern Virginia, Phoenix, and Silicon Valley. Continuous enterprise modernization and smart building initiatives further contribute to demand growth.

Asia Pacific

Asia Pacific is the fastest-growing region, accounting for nearly 40% of new global data center deployments. China leads the region with its New Infrastructure initiative, while India is witnessing rapid growth through BharatNet and expanding IT services sectors.

Countries such as Singapore, Indonesia, and Vietnam are emerging as major data center investment destinations, further strengthening regional demand for structured cabling systems.

Europe

Europe represents the second-largest market, driven by the EU’s Digital Decade 2030 strategy. Countries such as Germany, the UK, and France are investing heavily in digital infrastructure modernization.

Standardization under EN 50173 and sustainability initiatives aimed at energy-efficient data centers are also shaping market dynamics across the region.

Competitive Landscape

The structured cabling market is moderately consolidated, with major global players dominating the competitive environment. Key companies include CommScope, Corning Incorporated, Belden Inc., Legrand SA, Nexans, Schneider Electric, Siemens AG, TE Connectivity, ABB Ltd., and Furukawa Electric.

These companies compete through innovation in fiber-optic solutions, expansion of global distribution networks, and integration of intelligent infrastructure management systems. Strategic mergers and acquisitions are also reshaping the competitive landscape, particularly in the fiber-optic segment.

Recent developments include Amphenol’s acquisition of CommScope’s Connectivity and Cable Solutions business, strengthening its position in data center fiber infrastructure. Similarly, companies are increasingly focusing on sustainable cabling solutions and BIM-integrated design tools to enhance installation efficiency.

Conclusion

The structured cabling market is entering a transformative growth phase driven by global digitalization, AI adoption, 5G expansion, and cloud infrastructure development. With the market projected to nearly double from US$ 13.4 billion in 2026 to US$ 24.2 billion by 2033, structured cabling remains a critical backbone of modern digital ecosystems.

While challenges such as high installation costs and skilled labor shortages persist, the long-term outlook remains highly positive. Emerging opportunities in AI data centers, smart cities, and government-backed broadband programs are expected to redefine market dynamics and create sustained demand for advanced cabling solutions.

As global connectivity requirements continue to intensify, structured cabling will remain an essential enabler of the next generation of digital infrastructure.