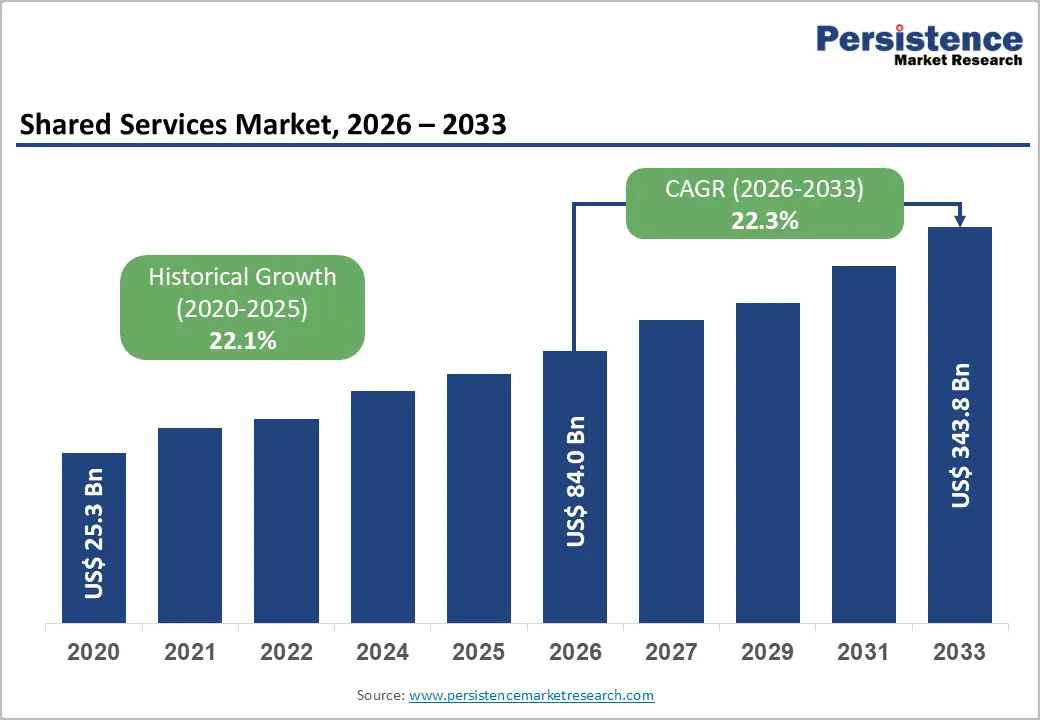

The global shared services market is entering a phase of rapid structural transformation as enterprises accelerate digital adoption, centralize business operations, and transition toward Global Business Services (GBS) models. Valued at US$84.0 billion in 2026, the market is projected to surge to US$343.8 billion by 2033, expanding at a strong CAGR of 22.3% during the forecast period. This remarkable growth reflects the increasing strategic importance of shared services as organizations move beyond cost optimization toward value creation, agility, and enterprise-wide digital transformation.

Traditionally viewed as back-office cost centers, shared services functions are now evolving into intelligent, technology-driven operating hubs. By leveraging cloud computing, robotic process automation (RPA), artificial intelligence (AI), and advanced analytics, enterprises are transforming finance, HR, procurement, and IT operations into integrated service ecosystems. These capabilities are enabling real-time decision-making, standardized global operations, and enhanced business resilience.

Industries such as BFSI, manufacturing, IT & telecom, and healthcare are leading adoption, while small and mid-sized enterprises are increasingly shifting toward outsourced and cloud-based shared service models. This democratization of shared services is expanding the addressable market and reinforcing its role as a core enabler of enterprise transformation.

Key Industry Highlights

The shared services market is shaped by several defining structural trends:

North America is expected to lead the global market with a 30% share in 2026, supported by the presence of multinational corporations, mature outsourcing ecosystems, and advanced digital infrastructure. Meanwhile, Asia Pacific is emerging as the fastest-growing region, driven by Global Capability Center (GCC) expansion, cost advantages, and a large skilled workforce.

In terms of deployment, cloud-based shared services are projected to dominate with a 60% revenue share in 2026, reflecting strong enterprise preference for scalability, flexibility, and reduced infrastructure costs. Application-wise, Finance & Accounting (F&A) remains the leading segment, accounting for over 35% of total revenue, driven by its standardized and high-volume transactional nature.

A key opportunity lies in the transformation of traditional shared services into AI-powered, analytics-driven digital platforms that deliver end-to-end enterprise value rather than isolated functional support.

Market Dynamics (DRO Analysis)

Driver: Digitalization and Automation of Back-Office Functions

A major growth catalyst for the shared services market is the increasing digitalization of core business functions. Enterprises are consolidating finance, HR, procurement, and IT operations into centralized shared service centers powered by cloud platforms, RPA, and AI-based systems.

These technologies significantly reduce manual workloads, minimize errors, and improve process efficiency. More importantly, they enable organizations to scale operations across geographies without proportionally increasing costs.

Intelligent automation is also reshaping the role of shared services from transactional processing units to strategic intelligence hubs. Real-time data analytics, predictive modeling, and AI-enabled workflows are improving decision-making speed and accuracy. As a result, shared services centers are increasingly becoming critical contributors to enterprise innovation and competitiveness.

Restraint: Organizational Resistance and Change-Management Challenges

Despite strong adoption momentum, organizational resistance remains a significant barrier. Many enterprises face internal pushback due to concerns over job displacement, reduced autonomy, and structural realignment.

Transitioning from decentralized to centralized shared services models requires substantial change management efforts. Organizations must harmonize diverse workflows, integrate legacy systems, and standardize processes across multiple regions. This complexity often leads to delays, inefficiencies, and increased implementation costs.

Cultural resistance is another key challenge, as employees may be reluctant to adopt new digital tools or automated workflows. Without strong leadership and structured transformation strategies, organizations risk service disruption and suboptimal outcomes during transition phases.

Opportunity: AI- and Analytics-Driven Shared Services Platforms

The integration of AI and advanced analytics represents one of the most significant growth opportunities in the market. AI-powered shared services platforms can process vast datasets to generate actionable insights, enhance forecasting accuracy, and optimize operational performance.

Machine learning, natural language processing (NLP), and intelligent virtual assistants are being widely adopted across finance, HR, and IT service functions. These technologies enable faster query resolution, automated reporting, and proactive issue detection.

Moreover, analytics-driven dashboards allow enterprises to monitor performance in real time, identify inefficiencies, and continuously optimize workflows. As organizations increasingly prioritize digital intelligence and operational agility, AI-enabled shared services are expected to become a cornerstone of enterprise transformation strategies.

Category-wise Analysis

Deployment Type Insights

Cloud-based deployment dominates the shared services market, accounting for approximately 60% of total revenue in 2026. Organizations are rapidly migrating from legacy on-premises systems to cloud environments to enhance flexibility, scalability, and integration capabilities.

Cloud platforms enable seamless standardization of processes across global business units while supporting real-time data access and cross-functional collaboration. Leading providers such as SAP and Oracle have significantly expanded their cloud-based shared services offerings to support enterprise transformation initiatives.

Cloud is also expected to be the fastest-growing segment due to rising demand for digital transformation, remote operations, and real-time analytics. Enterprises increasingly prefer cloud-based shared services for their ability to support hybrid work models and global operations with minimal infrastructure constraints.

Application Insights

Finance & Accounting (F&A) continues to dominate the application landscape, holding around 35% market share in 2026. This dominance is attributed to the highly structured, compliance-driven, and transaction-heavy nature of financial processes such as accounts payable, payroll, and financial reporting.

Organizations are centralizing these functions to improve accuracy, reduce operational costs, and ensure regulatory compliance. Companies like Genpact play a key role in delivering end-to-end finance transformation services to global enterprises.

Meanwhile, the IT services segment is emerging as the fastest-growing application area. Increasing reliance on digital infrastructure, cloud platforms, and cybersecurity systems is driving demand for centralized IT shared services. Platforms like ServiceNow are enabling enterprises to automate IT service management, improve response times, and enhance system reliability.

Regional Insights

North America

North America leads the global shared services market with a 30% share in 2026, driven by strong enterprise digitalization and advanced outsourcing ecosystems. The United States accounts for nearly 70% of regional adoption, supported by a dense concentration of multinational corporations and mature cloud infrastructure.

Canada is expanding steadily through nearshore shared service hubs, while Mexico is emerging as a cost-efficient destination under nearshoring trends. Companies such as Infosys and Cognizant are expanding delivery centers across the region to support digital transformation initiatives and enhance service delivery efficiency.

Europe

Europe remains a key shared services market, growing at a CAGR of approximately 16.9%. The United Kingdom leads with around 35% regional share, driven by strong financial services infrastructure and multinational headquarters.

Germany follows closely, supported by its robust manufacturing sector and ongoing digital modernization efforts. France is also witnessing steady growth through government-led digital transformation initiatives. Major players such as Capgemini continue to play a critical role in delivering integrated shared services across the region.

Asia Pacific

Asia Pacific is the fastest-growing regional market, driven by rapid digital transformation and expanding GCC ecosystems. China accounts for approximately 40% of regional demand, supported by government-backed digitalization initiatives and expansion of service-sector capabilities.

India contributes around 30%, fueled by the growth of IT outsourcing, GCC expansion, and strong talent availability. Japan is also modernizing legacy systems to improve operational efficiency and competitiveness.

The region is expected to remain a global hub for shared services delivery due to its cost advantages, scalability, and strong digital talent pool.

Competitive Landscape

The shared services market is moderately fragmented, with strong participation from global IT service providers, consulting firms, and outsourcing specialists. Competition is increasingly defined by digital capability rather than cost arbitrage alone.

Key players such as Accenture, IBM, Capgemini, Genpact, Cognizant, Infosys, and Deloitte are focusing on AI-driven platforms, cloud-native architectures, and end-to-end enterprise service integration. Strategic acquisitions, partnerships, and platform-based service models are becoming central to competitive differentiation.

The market is also witnessing increased investment in automation and AI factories, enabling enterprises to deploy scalable, secure, and intelligent business services.

Key Industry Developments

In March 2026, Cognizant launched its AI Factory, a cloud-based platform designed to accelerate enterprise AI deployment and enhance automation across business functions.

In October 2025, Infosys partnered with Telenor Shared Services to modernize HR operations through a cloud-based Human Capital Management platform, improving process standardization and employee experience.

In August 2025, Maersk established a shared service center in Warsaw to streamline European operations and strengthen centralized business functions.

Conclusion

The global shared services market is undergoing a fundamental transformation from cost-driven operational centers to AI-enabled strategic ecosystems. With rapid advancements in cloud computing, automation, and analytics, shared services are becoming central to enterprise agility, scalability, and innovation.

As organizations continue to prioritize digital transformation, the market is expected to witness sustained high growth through 2033. The convergence of technology, process centralization, and global delivery models will redefine how enterprises manage core business functions, making shared services a critical pillar of the modern digital economy.