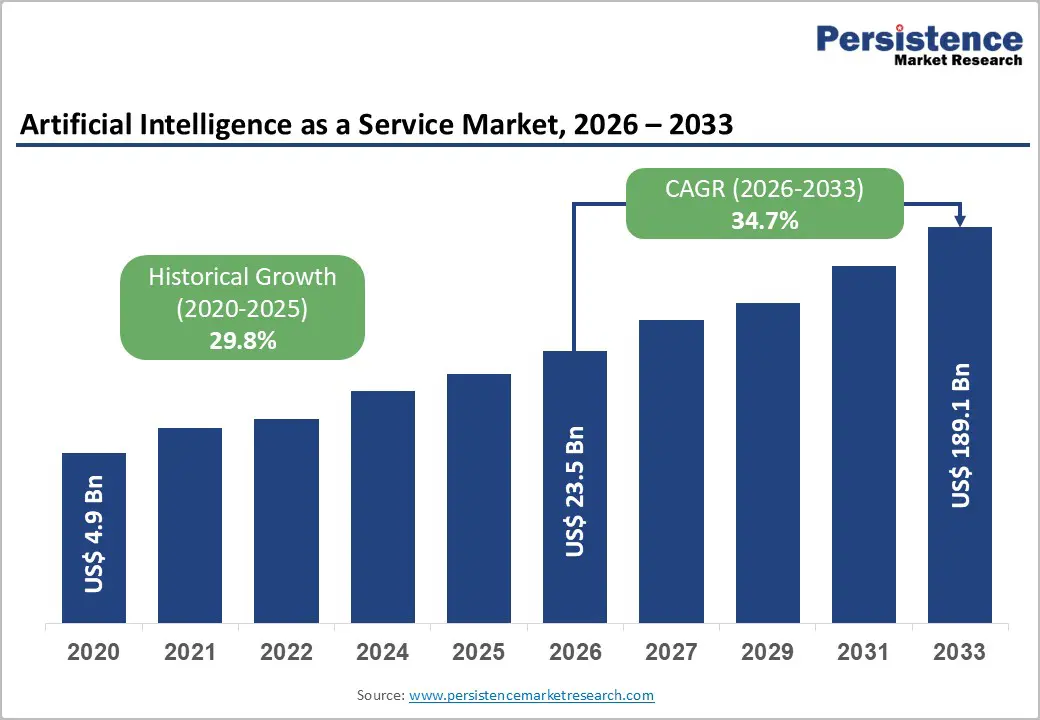

The global Artificial Intelligence as a Service (AIaaS) market is entering a phase of accelerated transformation, driven by the convergence of cloud computing, generative AI, and enterprise digitalization. Valued at approximately US$23.5 billion in 2026, the market is projected to surge to US$189.1 billion by 2033, expanding at a remarkable CAGR of 34.7% during the forecast period.

This strong growth reflects a fundamental shift in how organizations consume artificial intelligence. Rather than building expensive in-house AI infrastructure, enterprises are increasingly adopting AI delivered through cloud-based, subscription-driven platforms. These platforms provide scalable access to machine learning models, APIs, and AI tools that support automation, decision-making, customer engagement, and predictive analytics across industries.

As data volumes grow exponentially and businesses demand faster innovation cycles, AIaaS is becoming a core enabler of enterprise intelligence and operational efficiency.

Market Overview and Structural Transformation

The AIaaS market is being shaped by a transition from traditional software delivery to AI-driven service ecosystems. Enterprises are no longer treating AI as a standalone capability but as a continuously evolving service embedded within cloud platforms.

Cloud hyperscalers such as AWS, Microsoft Azure, and Google Cloud are leading this shift by offering end-to-end AI stacks that include pre-trained models, data pipelines, and deployment tools. These platforms allow businesses to integrate AI into workflows without deep technical expertise.

The growing adoption of APIs, low-code AI tools, and managed machine learning services is lowering entry barriers, making AI accessible even to small and mid-sized enterprises. As a result, AIaaS is becoming a foundational layer for digital transformation strategies across sectors.

Key Market Highlights

Several structural trends define the AIaaS market landscape in 2026:

- Leading Offering: Machine Learning dominates with over 30% market share, valued above US$7.1 billion, driven by predictive analytics, fraud detection, and enterprise automation use cases.

- Leading Deployment: Public cloud leads with over 51% share, valued at more than US$12 billion, due to scalability and cost efficiency.

- Leading Enterprise Size: Large enterprises account for over 64% share, valued above US$15 billion, driven by complex data ecosystems and advanced AI integration needs.

- Leading End-user Industry: IT & Telecom holds more than 20% share, valued at over US$4.7 billion, supported by network optimization and customer service automation.

- Leading Region: North America dominates with over 40% share, valued at US$9.4 billion, while Asia Pacific emerges as the fastest-growing region with a CAGR of 41.5%.

These indicators highlight a market that is both mature in developed economies and rapidly expanding in emerging digital ecosystems.

Market Drivers

Explosion of Enterprise Data Generation

One of the most significant growth drivers is the unprecedented rise in global data generation. By 2026, worldwide data creation is expected to exceed 220–240 zettabytes, fueled by IoT devices, social media platforms, digital enterprises, and connected systems.

Traditional IT infrastructure is no longer sufficient to handle this scale of data processing. AIaaS platforms provide elastic compute resources and advanced analytics tools that enable organizations to process massive datasets in real time. Cloud providers like AWS and Google Cloud offer integrated machine learning environments that simplify large-scale data analysis.

This shift is fundamentally redefining enterprise data strategies, pushing organizations toward cloud-native AI adoption.

Rising Demand for Personalized Customer Experience

Enterprises are increasingly focusing on hyper-personalization to improve customer engagement and retention. AI-powered recommendation engines, sentiment analysis tools, and predictive behavioral models are now widely used in retail, e-commerce, banking, and media industries.

Research indicates that over 80% of customers are more likely to purchase from brands offering personalized experiences. AIaaS platforms allow companies to deploy such capabilities without building complex AI systems internally.

Companies like Salesforce and Adobe are embedding AI-driven personalization features directly into their cloud ecosystems, enabling real-time customer insights and adaptive marketing strategies.

Market Restraints

Dependence on Cloud Infrastructure and Connectivity

Despite strong growth, AIaaS adoption is constrained by reliance on robust cloud infrastructure and high-speed connectivity. In regions with limited digital infrastructure, latency and bandwidth limitations hinder real-time AI applications such as autonomous systems and fraud detection.

Additionally, enterprises face vendor lock-in risks when heavily dependent on single-cloud ecosystems. These challenges limit adoption in developing economies and create concerns around operational flexibility.

Data Privacy and Regulatory Complexity

Data governance remains a critical barrier to AIaaS expansion. Regulations such as the EU General Data Protection Regulation (GDPR) and the EU AI Act (2024) impose strict requirements on data usage, transparency, and accountability in AI systems.

Non-compliance penalties can reach up to €35 million or 7% of global annual turnover, making regulatory adherence a top priority for enterprises. These frameworks increase operational costs and slow down deployment cycles, particularly for multinational organizations operating across multiple jurisdictions.

Market Opportunities

Emergence of Agentic AI

A major opportunity lies in the rise of Agentic AI systems, which go beyond content generation to autonomous decision-making and task execution. These AI agents can coordinate across enterprise tools, APIs, and workflows to complete complex processes such as procurement, customer support resolution, and financial reconciliation.

This evolution is transforming AIaaS from “tools-as-a-service” into autonomous workflow-as-a-service. Enterprises benefit from reduced operational costs, improved efficiency, and continuous process optimization.

AIaaS providers are increasingly integrating orchestration layers, memory systems, and multi-agent frameworks, creating new revenue streams and redefining enterprise automation.

Expansion of Edge AI and Real-Time Intelligence

Another key opportunity is the integration of AIaaS with edge computing environments. As industries adopt IoT devices and smart systems, there is growing demand for low-latency AI processing closer to data sources.

By 2030, global IoT devices are expected to exceed 40 billion units, significantly increasing the need for edge-based intelligence. Industries such as manufacturing, automotive, and logistics are deploying edge AI for predictive maintenance, autonomous operations, and real-time monitoring.

AIaaS providers are responding by extending cloud AI models to hybrid cloud-edge architectures, unlocking new commercial opportunities.

Segment Analysis

By Offering: Machine Learning Dominance

Machine learning remains the dominant segment, accounting for over 30% of market share. It is widely used for forecasting, fraud detection, and decision intelligence. Its ability to continuously learn from new data makes it indispensable across industries.

Chatbots and virtual assistants represent another fast-growing segment, driven by demand for automated customer service and conversational AI solutions. These tools provide 24/7 support, multilingual capabilities, and scalable engagement models.

By Deployment: Public Cloud Leadership

Public cloud deployment dominates due to its scalability, cost efficiency, and ease of access. Enterprises benefit from eliminating heavy upfront infrastructure investments while gaining access to advanced AI tools.

Meanwhile, hybrid cloud models are gaining traction as organizations seek to balance data security with computational flexibility, particularly in regulated sectors like healthcare and banking.

By Enterprise Size: Large Enterprises Lead, SMEs Accelerate

Large enterprises dominate the market due to their ability to manage complex datasets and invest in AI transformation initiatives. They use AIaaS for supply chain optimization, risk management, and customer experience enhancement.

However, small and medium enterprises (SMEs) are growing rapidly at over 40% CAGR, driven by affordable cloud-based AI tools that eliminate the need for in-house AI expertise.

By End User: IT & Telecom Leads

The IT & telecom sector holds a significant share due to its reliance on AI for network optimization, predictive maintenance, and automated customer support. AI helps telecom providers manage bandwidth allocation and reduce operational inefficiencies.

Retail and e-commerce are also emerging as high-growth sectors, leveraging AIaaS for personalized recommendations, demand forecasting, and pricing optimization.

Regional Analysis

North America

North America leads the global AIaaS market with over 40% share, supported by strong hyperscaler ecosystems and government-backed AI initiatives. The United States plays a central role through federal programs and defense-related AI investments, driving large-scale enterprise adoption.

Asia Pacific

Asia Pacific is the fastest-growing region with a CAGR of 41.5%, fueled by rapid digital transformation and national AI strategies in China, India, and Japan. Major cloud providers such as Alibaba Cloud and Tencent Cloud are expanding AIaaS offerings across industries.

India’s AI initiatives, including the IndiaAI Mission, are also accelerating AI infrastructure development and adoption.

Europe

Europe accounts for over 23% market share, supported by strong regulatory frameworks and industrial AI adoption. The EU AI Act is encouraging enterprises to adopt compliant, transparent AI systems.

Germany leads industrial AI integration, while the UK is investing heavily in sovereign AI infrastructure and compute capacity expansion.

Competitive Landscape

The AIaaS market is moderately consolidated, dominated by global technology giants and cloud service providers. Key players are focusing on expanding AI portfolios through acquisitions, partnerships, and innovation in generative and agentic AI.

Strategic differentiation is increasingly based on model performance, scalability, security features, and integration capabilities. Subscription-based and API-driven business models are becoming standard across the industry.

Key Developments

Recent developments highlight rapid innovation:

- In April 2026, Avid partnered with Google Cloud to integrate agentic AI into media production workflows using Vertex AI and Gemini models.

- In May 2025, Microsoft launched Azure AI Foundry Agent Service, enabling enterprises to build and deploy AI agents within a managed cloud environment.

These developments signal a clear shift toward autonomous AI systems integrated directly into enterprise workflows.

Conclusion

The Artificial Intelligence as a Service market is transitioning from early-stage cloud AI adoption to a mature ecosystem powered by automation, autonomy, and real-time intelligence. With a projected rise to US$189.1 billion by 2033, the sector is poised to become one of the most critical pillars of enterprise digital infrastructure.

Growth will be driven by exploding data volumes, demand for personalization, and the rapid rise of agentic AI systems. However, challenges related to regulation, infrastructure dependency, and data governance will continue shaping market evolution.

Ultimately, AIaaS is not just a technology trend—it is becoming the default operating model for intelligent enterprises worldwide.