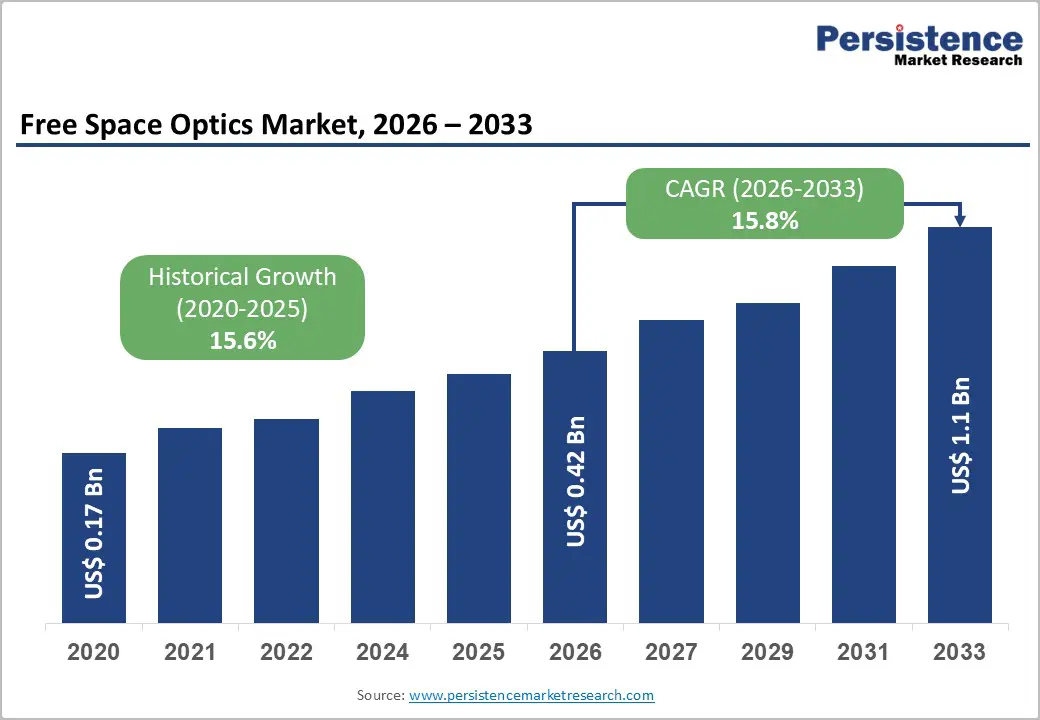

The global free space optics (FSO) market is entering a high-growth phase as telecom operators, defense agencies, and enterprise networks increasingly seek ultra-fast, flexible, and cost-efficient alternatives to traditional fiber deployments. In 2026, the market is estimated to be valued at US$0.42 billion, and it is projected to reach US$1.1 billion by 2033, expanding at a CAGR of 15.8% during the forecast period.

This strong growth trajectory is being driven by rising demand for high-capacity wireless optical communication systems, especially in environments where fiber installation is difficult, expensive, or time-consuming. The technology is also gaining traction as a complementary layer to fiber and RF networks, particularly in dense urban environments and remote regions where connectivity gaps remain a challenge.

Governments and industry bodies are further accelerating adoption through regulatory and infrastructure initiatives, including FCC 2025 broadband deployment updates and the ongoing development of ETSI optical wireless communication standards. These frameworks are helping establish interoperability, performance benchmarks, and deployment confidence for large-scale FSO integration.

Market Overview

Free space optics technology uses laser beams to transmit data through the atmosphere without requiring physical fiber cables. It delivers fiber-like speeds with extremely low latency, making it ideal for applications such as 5G backhaul, secure defense communication, and enterprise connectivity.

FSO systems are increasingly deployed as part of hybrid network architectures combining fiber, RF, and satellite links. This integrated approach ensures higher reliability and redundancy, especially in mission-critical environments.

The market is evolving from niche deployments to mainstream adoption, supported by improvements in adaptive optics, beam tracking systems, and weather-resilient modulation techniques that enhance performance in challenging environmental conditions.

Key Industry Highlights

North America is expected to lead the global market in 2026, accounting for approximately 35% share, driven by advanced telecom infrastructure, strong defense adoption, and early deployment in 5G networks. Meanwhile, Asia Pacific is projected to be the fastest-growing region, fueled by rapid urbanization, smart city initiatives, and massive digital infrastructure investments.

By range type, short-range FSO systems dominate the market with around 50% share, largely due to enterprise campus connectivity and urban last-mile communication needs. In terms of applications, mobile backhaul leads with over 60% share, reflecting its critical role in 5G small-cell deployments.

A major opportunity lies in the shift toward hybrid FSO-RF networks, which combine optical and radio frequency technologies to ensure uninterrupted connectivity across varying environmental conditions.

Market Drivers

Rising Bandwidth Demand from 5G and Smart Cities

One of the strongest drivers of the FSO market is the exponential growth in bandwidth demand driven by 5G rollout and smart city development. Telecom operators are under pressure to deploy dense small-cell networks that require fast and flexible backhaul solutions.

FSO technology provides fiber-like data speeds without the need for digging or laying physical cables. This makes it especially valuable in metropolitan areas where infrastructure deployment is costly or restricted.

Smart city ecosystems further amplify demand. Applications such as intelligent traffic systems, surveillance networks, and IoT-enabled public services require high-speed, uninterrupted communication between distributed nodes. FSO enables rapid deployment and scalable connectivity in such environments.

Market Restraints

Line-of-Sight Dependency and Environmental Sensitivity

Despite its advantages, FSO technology faces key limitations. The most significant is its strict reliance on line-of-sight communication, which restricts deployment flexibility. Any obstruction—such as buildings, vehicles, or terrain variations—can disrupt signal transmission.

Environmental conditions also impact performance. Fog, heavy rain, dust storms, and atmospheric turbulence can weaken or scatter laser signals, reducing reliability and transmission range. These challenges often necessitate backup systems or hybrid integration with RF technologies to ensure continuity.

Market Opportunities

Hybrid FSO-RF Communication Systems

The emergence of hybrid FSO-RF systems presents one of the most promising opportunities in the market. These systems dynamically switch between optical and radio frequency links depending on environmental conditions, ensuring continuous connectivity.

In urban telecom networks, hybrid systems help maintain stable communication during adverse weather conditions. In defense applications, they provide resilient and jam-resistant communication channels that are difficult to intercept.

Smart cities and industrial IoT ecosystems are also increasingly adopting hybrid architectures to ensure high availability and redundancy in mission-critical operations.

Category-wise Market Analysis

Range Type Insights

The short-range segment is expected to dominate the market, accounting for about 50% of revenue in 2026. This segment is widely used in enterprise campuses, metro networks, and last-mile connectivity applications. It enables secure, high-speed communication between buildings without requiring underground fiber installation.

For example, corporate campuses use short-range FSO links to connect multiple office buildings, ensuring fast internal data exchange with minimal infrastructure costs.

On the other hand, the long-range segment is projected to be the fastest-growing category. It is increasingly used in satellite communications, defense operations, and inter-city connectivity where fiber deployment is not feasible. Satellite ground stations, for instance, rely on long-range FSO systems to achieve high-speed, low-latency communication with orbiting satellites.

Component Type Insights

The transmitter assembly segment is expected to lead the market, capturing approximately 55% share in 2026. These systems include lasers, modulators, and beam-forming optics that determine signal strength, stability, and transmission quality.

They are widely used in 5G small-cell backhaul systems, enabling high-speed data transfer between base stations without physical cabling.

Meanwhile, the receiver assembly segment is expected to grow rapidly due to increasing demand for long-distance, high-reliability communication. Advanced receivers use optical amplifiers and signal correction mechanisms to maintain performance under adverse atmospheric conditions, particularly in satellite-to-ground communication links.

Application Insights

Mobile backhaul is projected to dominate the market with around 60% share in 2026, driven by rapid 5G expansion and urban network densification. Telecom operators rely on FSO to connect rooftop small-cell towers in dense urban environments where fiber installation is impractical.

For example, in major cities, FSO links are used to connect base stations across buildings, enabling high-capacity data transfer for mobile users without requiring extensive trenching.

The defense segment is expected to grow at the fastest pace. Military organizations are increasingly adopting FSO for secure, high-speed communication in environments where RF systems are vulnerable to jamming or interception. Battlefield communication networks often rely on FSO links between command units and forward bases to ensure secure, real-time data exchange.

Regional Analysis

North America

North America leads the global FSO market with a projected 35% share in 2026. The United States dominates the region due to its advanced telecom infrastructure and strong defense sector adoption.

FSO technology is widely deployed in military communication systems, smart city infrastructure, and 5G backhaul networks. Canada contributes to growth through rural broadband expansion projects, while Mexico focuses on telecom modernization in urban centers.

Europe

Europe represents a significant market driven by demand for secure communication and smart infrastructure development. Germany leads adoption through industrial automation and defense modernization initiatives, while the U.K. focuses on telecom densification and data center interconnectivity.

France contributes through aerospace and defense applications, particularly in integrating optical wireless systems into next-generation communication networks.

Companies such as Mynaric AG are actively developing laser communication terminals for satellite and aerospace applications, strengthening Europe’s position in global FSO innovation.

Asia Pacific

Asia Pacific is expected to be the fastest-growing region, driven by rapid digital transformation and large-scale 5G deployment.

China leads regional adoption with government-backed infrastructure programs and widespread deployment in metro and industrial zones. India is expanding FSO use in rural broadband and last-mile connectivity under digital inclusion initiatives. Japan continues to invest in advanced satellite communication systems and defense modernization.

Companies like Cailabs are supporting optical communication deployments that enhance signal stability in challenging atmospheric conditions.

Competitive Landscape

The FSO market is moderately fragmented, with competition driven by innovation in laser communication, adaptive beam control, and hybrid networking systems. Key players include:

- Mynaric AG

- fSONA Networks

- Cailabs

- CBL Communication by Light

- EC System

- Wireless Excellence Limited

- Trimble Inc.

- CACI International Ltd

- ViaSat

- Mostcom JSC

These companies are focusing on product innovation, strategic partnerships with telecom operators, and expansion into satellite communication systems.

Key Industry Developments

- February 2026: Mostcom JSC expanded its FSO solutions for high-speed wireless data transmission, strengthening its position in laser communication systems.

- December 2025: Japan’s NICT demonstrated 2 Tbit/s FSO communication over a 7.4 km urban link in Tokyo using compact optical terminals, achieving stable performance despite atmospheric turbulence.

- August 2025: Aircision introduced second-generation FSO systems powered by integrated photonics to enhance scalability and performance.

Conclusion

The free space optics market is transitioning from a niche communication technology to a critical component of next-generation global connectivity infrastructure. With strong demand from 5G networks, smart cities, defense systems, and satellite communication, FSO is becoming a key enabler of ultra-fast and flexible data transmission.

While challenges such as line-of-sight dependency and weather sensitivity persist, ongoing innovations in hybrid FSO-RF systems, adaptive optics, and photonic integration are significantly improving reliability.

Between 2026 and 2033, the market is expected to witness sustained double-digit growth, positioning FSO as a vital complement to fiber and wireless communication networks in the global digital economy.