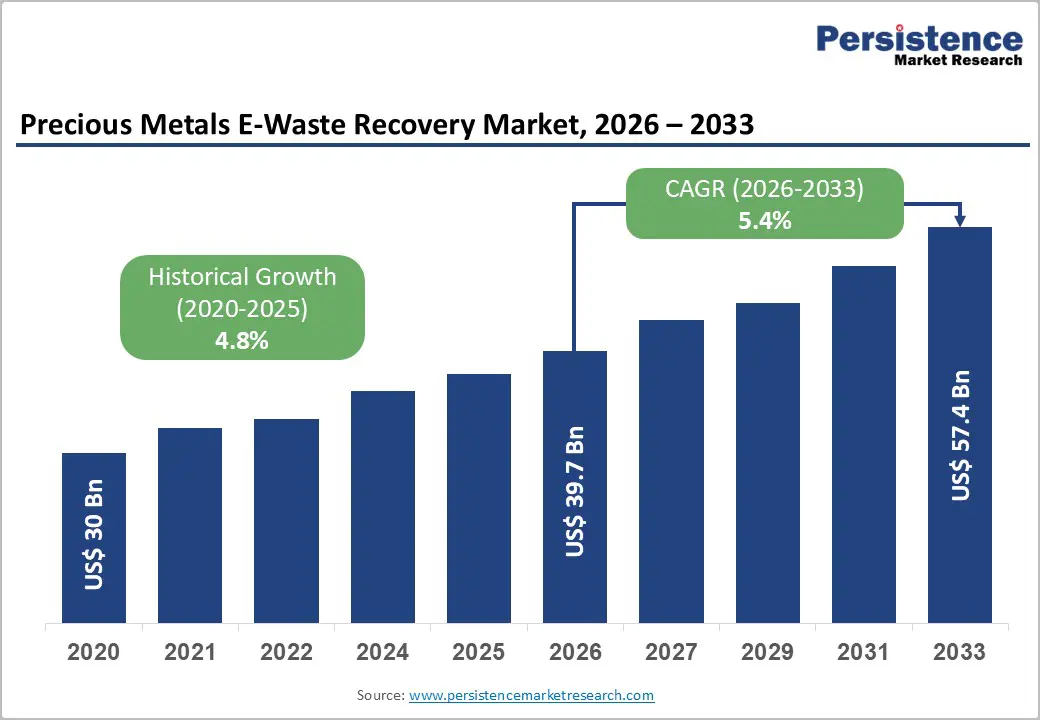

The global precious metals e-waste recovery market is entering a structurally important growth phase as electronic waste becomes one of the fastest-expanding waste streams worldwide and simultaneously one of the most valuable secondary sources of raw materials. Valued at US$ 39.7 billion in 2026, the market is projected to reach US$ 57.4 billion by 2033, expanding at a CAGR of 5.4% during the forecast period.

This steady growth is being driven by a powerful combination of rising e-waste volumes, increasing demand for critical metals such as gold, palladium, silver, and copper, and global policy shifts toward circular economy models. As industries such as electronics, automotive, telecommunications, and renewable energy expand, the embedded value of metals inside discarded devices is transforming waste into a strategic resource stream.

According to the Global E-waste Monitor 2024 (UNU), global e-waste reached approximately 62 million metric tonnes in 2022, yet only 22.3% was formally collected and recycled. This imbalance highlights both a major environmental challenge and a significant untapped economic opportunity for precious metals recovery.

Market Overview

Precious metals e-waste recovery refers to the extraction of high-value metals from discarded electrical and electronic equipment, including smartphones, laptops, servers, circuit boards, batteries, and industrial electronics. These devices contain concentrated amounts of gold, silver, palladium, platinum group metals (PGMs), and copper.

Unlike primary mining, where ore grades are declining globally, e-waste offers significantly higher metal concentration. For example, a metric tonne of mobile phones can contain up to 300 grams of gold, compared to just 5 grams per tonne of gold ore. This stark difference is one of the most important economic drivers of the urban mining industry.

E-waste generated in 2022 contained approximately:

- 31 billion kg of metals

- 17 billion kg of plastics

- 14 billion kg of other materials

This composition highlights the scale of recoverable value embedded in discarded electronics.

Key Market Highlights

Several structural trends are shaping the global precious metals e-waste recovery landscape:

- Rapid E-waste Growth: Global e-waste is expected to reach 82 million tonnes by 2030, significantly increasing feedstock availability.

- High Metal Value Concentration: Gold dominates value recovery, accounting for nearly 38% of market share.

- Strong Policy Support: Over 81 countries now have e-waste regulations, with 67 implementing EPR frameworks.

- Rising Commodity Prices: Gold and palladium prices frequently exceeding US$1,800–2,400/oz improve recycling economics.

- Technology Advancement: Hydrometallurgy and bioleaching technologies enable recovery rates above 98%.

- Leading Technology Segment: Pyrometallurgy holds 42% market share due to scalability and efficiency.

- Leading Application: IT and telecom equipment contributes approximately 35% of total revenue.

Market Dynamics

Drivers

- Rapid Increase in Global E-Waste Generation

The exponential growth of consumer electronics is the most significant driver of this market. Short device replacement cycles—especially for smartphones and laptops—are continuously increasing waste volumes.

The ITU projects 82 million tonnes of e-waste annually by 2030, ensuring a consistent and expanding feedstock base for recyclers. Governments are responding with mandatory collection targets, strengthening formal recycling channels and improving material recovery rates.

- High Economic Value of Precious Metals

Precious metals embedded in electronics are significantly more concentrated than in natural ores. Rising prices of gold, silver, and palladium have strengthened the business case for urban mining.

Palladium has traded above US$2,000 per ounce in recent years, while gold has remained above US$1,800 per ounce, occasionally exceeding US$2,400 per ounce. These price levels make even low-yield recovery processes economically viable.

- Expansion of Electronics and Automotive Industries

The growing use of electronics in electric vehicles, renewable energy systems, and industrial automation is increasing demand for precious metals. As these devices reach end-of-life, they create a secondary supply chain feeding the recovery market.

Restraints

- Informal Recycling Ecosystem

A major challenge is the dominance of informal recycling networks in developing economies. Around 77.7% of global e-waste is not processed through formal systems.

Informal recycling methods such as open burning and acid leaching:

- Recover metals inefficiently

- Cause environmental damage

- Reduce feedstock availability for formal recyclers

This fragmentation limits the scalability of organized recovery systems.

- Regulatory and Cross-Border Barriers

International regulations such as the Basel Convention restrict transboundary movement of e-waste. While environmentally necessary, these rules increase logistics complexity and reduce global optimization of recycling infrastructure.

Compliance with multiple regulatory frameworks such as the EU WEEE Directive, U.S. state laws, and national EPR systems increases operational costs for recyclers.

Opportunities

- Advanced Recovery Technologies

Technological innovation is transforming recovery efficiency and environmental performance. Key advancements include:

- Hydrometallurgy: Uses aqueous solutions for selective metal recovery with low energy consumption.

- Bioleaching: Uses microorganisms to extract metals in an eco-friendly manner.

- Non-cyanide leaching systems: Improve safety and environmental compliance.

Companies such as EnviroLeach Technologies have demonstrated gold recovery rates exceeding 98%, marking a significant leap in efficiency.

- Circular Economy Regulations

Governments are increasingly promoting domestic recycling of critical raw materials:

- EU Critical Raw Materials Act: Targets 25% of strategic materials from recycling by 2030.

- U.S. Inflation Reduction Act (IRA): Supports domestic mineral recovery through tax incentives.

- Japan’s Urban Mining Strategy: Treats e-waste as a national resource reserve.

These policies are accelerating infrastructure investment and improving market stability.

Segment Analysis

By Metal Type

Gold

Gold dominates the market due to its high value and extensive use in PCBs, connectors, and semiconductor components. It accounts for approximately 77% of revenue share in value terms.

Despite low physical volume, gold remains the primary economic driver. One tonne of circuit boards can yield up to 0.45 kg of gold, making electronic scrap significantly richer than natural ore.

Copper

Copper is the second-largest segment, valued at approximately US$3.1 billion (2025). It is essential for electrical conductivity and infrastructure applications. Recovery technologies increasingly integrate AI and advanced separation techniques to enhance copper yield.

By Technology

Pyrometallurgy

Pyrometallurgy leads the market with 42% share due to:

- High throughput capability

- Ability to process mixed waste streams

- Mature industrial infrastructure

Facilities such as Umicore’s Hoboken refinery and Aurubis’ Hamburg plant demonstrate recovery efficiencies exceeding 95% for key metals.

Hydrometallurgy

Hydrometallurgy is gaining traction due to:

- Lower emissions

- Higher selectivity

- Improved metal purity

- Energy efficiency

This segment is expected to expand rapidly as sustainability requirements tighten.

By Source

IT & Telecommunications Equipment

This segment leads the market with 35% revenue share, driven by:

- High metal density in PCBs and chips

- Rapid device turnover cycles

- Large-scale enterprise hardware replacement

The transition to 5G and cloud infrastructure is further accelerating e-waste generation from telecom equipment.

Regional Analysis

North America

North America benefits from strong regulatory frameworks and advanced recycling infrastructure. The U.S. EPA and Department of Energy actively support critical mineral recovery initiatives.

Companies such as Electronic Recyclers International (ERI) and Sims Limited are expanding processing capacity, supported by corporate ESG commitments from major technology firms.

Europe

Europe is the most advanced regulatory region, driven by the WEEE Directive and Circular Economy Action Plan. Countries like Germany, the UK, and France have established highly efficient collection systems.

Companies such as Umicore and Aurubis lead globally in integrated metal recovery operations, supported by harmonized EU regulations.

Asia Pacific

Asia Pacific dominates global e-waste generation and is rapidly scaling formal recycling systems.

- China: Largest generator and increasingly regulated recycling ecosystem

- Japan: Global leader in urban mining innovation

- India: Emerging high-growth market, expected to generate over 3,230 kilotonnes annually by 2025

- ASEAN: Growing processing hubs like Singapore and Malaysia attracting investment

Competitive Landscape

The market is moderately consolidated with major players focusing on vertical integration, capacity expansion, and technological innovation.

Key Players Include:

- Umicore

- Aurubis AG

- Boliden Group

- Sims Limited

- Veolia

- Stena Recycling

- DOWA Holdings

- Johnson Matthey

- Heraeus Holding GmbH

- EnviroLeach Technologies

- TES-AMM

- Metallix Refining Inc.

Strategic Trends:

- Expansion of refining capacity

- Adoption of AI-based sorting systems

- Investment in low-emission technologies

- Partnerships with OEMs for closed-loop recycling

- Certification under R2 and e-Stewards standards

Recent developments such as TOMRA’s AI-enabled sorting systems and Umicore’s capacity expansion highlight the industry’s technological evolution.

Conclusion

The precious metals e-waste recovery market is evolving into a critical pillar of the global circular economy. Driven by accelerating e-waste generation, rising metal prices, and tightening environmental regulations, the sector is shifting from a niche recycling activity to a strategically important resource industry.

While challenges such as informal recycling and regulatory complexity persist, advancements in hydrometallurgical and bioleaching technologies, combined with strong policy support, are expected to significantly improve recovery rates and economic viability.

By 2033, as the market approaches US$ 57.4 billion, precious metals recovery from e-waste will play an increasingly central role in global supply chains, reducing dependence on primary mining while supporting sustainable industrial growth.