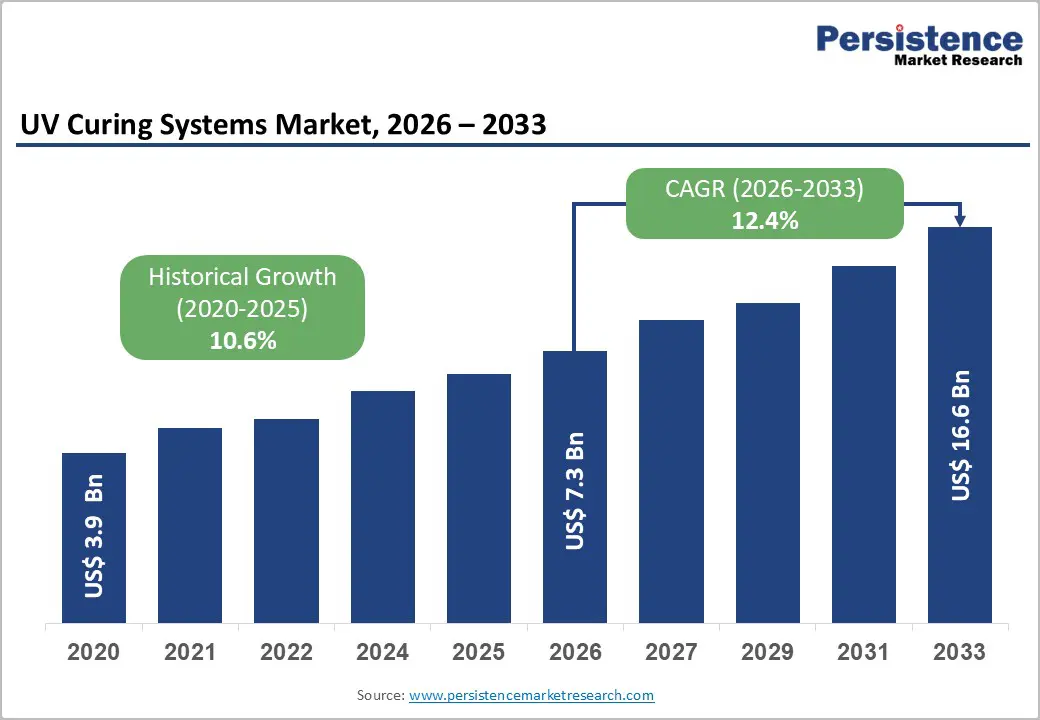

The global UV Curing Systems Market is poised for strong expansion, with its market size expected to increase from US$ 7.3 billion in 2026 to US$ 16.6 billion by 2033, registering a robust CAGR of 12.4% during the forecast period. The market has demonstrated remarkable momentum over the past decade, rising from US$ 3.9 billion in 2020, supported by increasing industrial automation, stricter environmental regulations, and the rapid adoption of UV LED technologies across manufacturing industries.

UV curing systems have become an integral part of modern production processes because they enable rapid curing of coatings, adhesives, inks, and sealants without the high energy consumption associated with conventional thermal curing. As manufacturers seek faster production cycles, improved product quality, and sustainable operations, UV curing technology is increasingly replacing traditional curing methods across electronics, automotive, medical devices, packaging, aerospace, and industrial manufacturing.

One of the strongest growth drivers is the commercial transition from mercury-based UV lamps to UV LED curing systems. UV LED technology offers significantly lower power consumption, longer operating life, minimal maintenance requirements, and mercury-free operation, making it the preferred solution for manufacturers seeking compliance with environmental regulations while reducing operating costs.

Market Dynamics

Driver: Rapid Adoption of UV LED Technology

The shift toward UV LED curing systems is fundamentally transforming the market landscape. Compared to conventional mercury lamps, UV LED systems consume approximately 20–50% less energy, while providing operational lifespans exceeding 20,000 hours. This substantially lowers maintenance costs and improves production uptime.

UV LEDs also deliver precise wavelength control between 365 nm and 405 nm, enabling manufacturers to optimize curing processes for sensitive materials used in semiconductor fabrication, printed circuit boards, optical components, and medical devices. The ability to reduce thermal damage makes LED curing particularly attractive for high-value manufacturing environments.

Today, more than 55% of newly installed UV curing systems worldwide are LED-based, reflecting a rapid technology transition that continues to accelerate across industrial sectors.

Driver: Environmental Regulations Supporting UV Adoption

Government regulations limiting hazardous materials and volatile organic compound (VOC) emissions have become major catalysts for UV curing system adoption.

The European Union's Restriction of Hazardous Substances (RoHS) directive continues to tighten restrictions on mercury-containing equipment, encouraging manufacturers to replace conventional mercury lamps with environmentally friendly LED alternatives.

Similarly, the U.S. Environmental Protection Agency (EPA) has implemented increasingly stringent VOC emission standards for coatings and adhesives. UV-curable materials, which are often 100% solids or water-based formulations, produce negligible VOC emissions, making UV curing systems an ideal solution for manufacturers seeking regulatory compliance.

Many manufacturers also benefit from government sustainability incentives, tax credits, and energy-efficiency rebates when investing in advanced UV LED equipment.

Driver: Electronics and Semiconductor Manufacturing Expansion

The global electronics industry continues to create substantial demand for UV curing systems.

UV curing plays a vital role in numerous manufacturing processes, including:

- PCB fabrication

- Component bonding

- Conformal coating

- Display manufacturing

- Semiconductor packaging

- Optical assembly

Global semiconductor sales reached approximately US$ 75.3 billion during November 2025, reflecting strong demand generated by AI infrastructure, automotive electronics, and advanced computing.

India is also emerging as a significant manufacturing hub. The country's electronics production increased from US$ 29 billion in FY2015 to US$ 101 billion in FY2023, supported by nearly US$ 17 billion under Production Linked Incentive (PLI) programs. These investments are creating new opportunities for UV curing equipment suppliers serving PCB manufacturing and semiconductor production facilities.

Market Restraints

High Initial Investment Costs

Despite favorable long-term economics, UV LED curing systems require significantly higher initial capital investment than conventional mercury-based equipment.

Small and medium-sized manufacturers often face budget constraints that delay equipment replacement despite recognizing long-term operational savings.

Furthermore, integrating UV curing systems into existing production lines frequently requires:

- Process redesign

- Equipment modification

- Material qualification

- Operator training

- Engineering support

These additional costs can extend return-on-investment periods for many organizations.

Supply Chain Challenges

The UV curing industry relies on a relatively concentrated supplier base for:

- UV LED chips

- Quartz components

- Photoinitiators

- Specialty optical materials

Many critical suppliers are located in Japan, South Korea, and Germany, exposing manufacturers to geopolitical risks and supply chain disruptions. Shortages of high-power UV LED arrays or specialty materials can delay equipment production and increase system costs.

Emerging Opportunities

Aerospace and Defense Manufacturing

The aerospace and defense industry represents one of the most promising high-value growth opportunities for UV curing systems.

Aircraft manufacturers increasingly utilize UV curing for:

- Composite bonding

- Avionics assembly

- Precision coatings

- Lightweight structural components

- Sensor encapsulation

The U.S. aerospace and defense industry generated nearly US$ 995 billion in economic activity during 2024, while European aerospace companies reported revenues exceeding €325 billion.

Growing investments in lightweight aircraft materials and advanced defense electronics are expected to further strengthen demand for precision UV curing technologies.

Electric Vehicle Production

The rapid expansion of electric vehicle manufacturing is creating entirely new application areas for UV curing systems.

UV curing technologies are increasingly used in:

- Battery assembly

- Power electronics

- Inverter manufacturing

- Camera modules

- ADAS sensors

- Battery management systems

Unlike conventional automobiles, electric vehicles require significantly greater use of electronic components and specialized adhesives, increasing demand for precision curing technologies.

Global vehicle registrations reached approximately 74.6 million units during 2024, with China remaining the world's largest automotive manufacturing hub.

Industrialization Across Emerging Markets

Rapid manufacturing growth across India, Vietnam, Thailand, and Indonesia continues to generate new demand for UV curing systems.

Government initiatives supporting electronics, semiconductor, automotive, and industrial manufacturing are encouraging installation of advanced production lines equipped with modern curing technologies.

As global manufacturers diversify supply chains beyond China, Southeast Asia is expected to become a significant regional market for UV curing equipment over the coming decade.

Technology Insights

UV LED Curing Systems Lead Market Growth

UV LED curing systems account for approximately 44% of the global market, making them the dominant technology segment.

Their popularity stems from several advantages:

- Lower energy consumption

- Mercury-free operation

- Longer service life

- Minimal maintenance

- Faster startup

- Better wavelength precision

- Reduced heat generation

These advantages make UV LED systems particularly suitable for electronics manufacturing, medical devices, digital printing, and advanced industrial applications.

Mercury Lamp Systems Continue Serving Legacy Installations

Although market share continues shifting toward LEDs, mercury lamp UV systems remain widely installed across existing manufacturing facilities.

Many organizations continue maintaining legacy systems where high-intensity broadband UV output remains technically advantageous.

However, tightening environmental regulations and the gradual expiration of regulatory exemptions are expected to accelerate replacement with LED technologies over the coming years.

System Type Analysis

Conveyor and Inline Systems Dominate

Conveyor and inline UV curing systems represent nearly 38% of global demand.

These systems are widely adopted because they integrate seamlessly into automated manufacturing lines while providing:

- Continuous production

- High throughput

- Consistent curing quality

- Reduced labor costs

- Improved manufacturing efficiency

Electronics manufacturing, automotive coating, packaging, and printing industries remain the largest users of inline UV curing equipment.

Spot Curing Systems Show Fastest Growth

Spot curing systems are emerging as one of the fastest-growing product categories.

Their compact size and precision make them ideal for:

- Medical device assembly

- Semiconductor packaging

- Fiber optics

- Microelectronics

- Precision adhesive bonding

Advancements in compact UV LED spot heads have significantly improved portability while reducing thermal impact on delicate components.

Industry Analysis

Electronics and Semiconductor Industry Leads

The electronics and semiconductor industry represents approximately 32% of total UV curing system demand.

Applications include:

- PCB assembly

- Semiconductor packaging

- Display manufacturing

- Optical sensors

- Wearable electronics

- Consumer electronics

The continued expansion of AI computing, cloud infrastructure, and automotive electronics is expected to sustain strong investment in UV curing equipment.

Industrial Manufacturing Records Fastest Growth

Industrial manufacturing is becoming the fastest-growing application segment.

Manufacturers increasingly replace conventional thermal curing processes with UV curing in:

- Wood finishing

- Metal coatings

- Plastic bonding

- Industrial adhesives

- Protective coatings

- Machinery manufacturing

UV curing improves productivity while reducing energy consumption and production cycle times.

Regional Analysis

Asia Pacific

Asia Pacific remains the largest regional market, accounting for approximately 42% of global revenue.

China continues to dominate due to its leadership in:

- Consumer electronics

- Automotive manufacturing

- PCB production

- Semiconductor assembly

South Korea and Japan maintain strong positions through advanced semiconductor manufacturing and display technologies.

India represents one of the fastest-growing markets, supported by government investments in electronics manufacturing, semiconductor production, and industrial automation.

North America

North America holds approximately 28% of global market share.

The United States benefits from:

- CHIPS Act investments totaling US$ 52.7 billion

- Strong aerospace manufacturing

- Advanced medical device production

- High-value electronics manufacturing

Environmental regulations encouraging low-VOC manufacturing continue supporting UV curing system adoption throughout the region.

Europe

Europe accounts for approximately 23% of global market revenue.

Major markets include:

- Germany

- France

- United Kingdom

- Italy

European manufacturers continue upgrading production facilities to comply with RoHS regulations while investing heavily in UV LED technologies that improve sustainability and energy efficiency.

Competitive Landscape

The UV curing systems market is moderately consolidated, with major manufacturers collectively accounting for nearly half of global revenue.

Leading companies include:

- Excelitas Technologies Corp.

- Nordson Corporation

- IST Metz GmbH

- GEW Limited

- Dymax Corporation

- Dr. Hönle AG

- Miltec UV Corporation

- Phoseon Technology

- American Ultraviolet Corporation

- Heraeus Noblelight GmbH

- Panasonic Holdings Corporation

- Baldwin Technology Company Inc.

- Panacol-Elosol GmbH

- UVitron International Inc.

Market leaders continue focusing on:

- UV LED innovation

- Modular upgrade solutions

- Energy-efficient designs

- Smart manufacturing integration

- Geographic expansion into emerging markets

- Strategic OEM partnerships

Recent product launches emphasize higher irradiance, lower power consumption, compact equipment footprints, and mercury-free operation to meet evolving customer requirements.

Future Outlook

The outlook for the global UV Curing Systems Market remains highly positive as manufacturers across industries prioritize sustainability, automation, and production efficiency. Continuous technological advancements in UV LED systems, coupled with stringent environmental regulations and growing investments in semiconductor fabrication, electric vehicles, aerospace, and industrial manufacturing, will sustain long-term demand.

While high initial equipment costs and supply chain constraints may temporarily limit adoption among smaller manufacturers, the long-term operational savings, improved product quality, and regulatory compliance offered by UV curing technologies provide compelling economic advantages. As UV LED technology continues to mature and costs decline, adoption is expected to accelerate across both developed and emerging markets, positioning UV curing systems as a cornerstone of next-generation industrial manufacturing.