Managed Data Center Services Market Overview

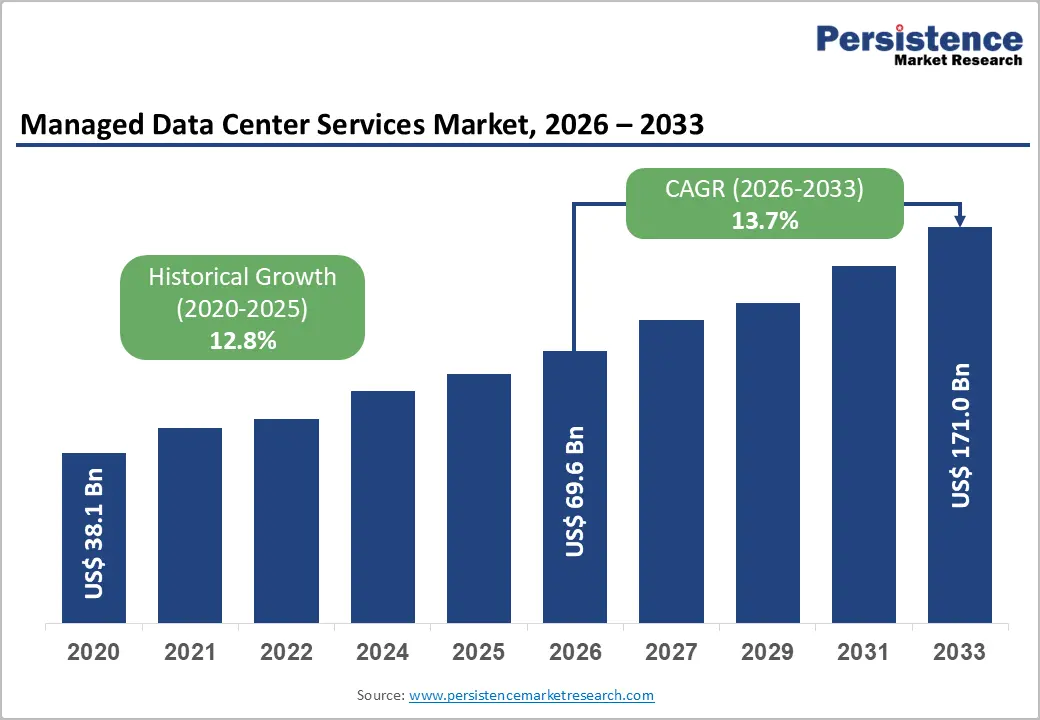

The global managed data center services market is entering a period of accelerated expansion as enterprises increasingly transition from traditional in-house infrastructure management toward outsourced, specialized service models. The market size is projected to reach US$69.6 billion in 2026 and is expected to grow to US$171.0 billion by 2033, expanding at a strong pace throughout the forecast period.

This growth is being fueled by several structural shifts across the enterprise technology landscape, including widespread cloud adoption, growing complexity of hybrid IT environments, increasing cybersecurity risks, and the rising need for scalable infrastructure management. Businesses are seeking reliable partners that can manage critical IT operations while improving performance, reducing costs, and ensuring compliance with evolving regulatory standards.

Managed data center service providers are increasingly moving beyond traditional hosting and infrastructure support. Modern providers offer integrated solutions covering infrastructure management, cloud operations, cybersecurity, automation, disaster recovery, workload optimization, and sustainability management. As organizations adopt artificial intelligence (AI), edge computing, and multi-cloud strategies, demand for specialized operational expertise continues to rise.

Key Market Highlights

- Market Size (2026): US$69.6 billion

- Forecast Value (2033): US$171.0 billion

- Leading Region: North America, accounting for approximately 34.1% market share in 2026

- Fastest-growing Region: Asia Pacific, driven by rapid digitalization and hyperscale infrastructure investments

- Dominant Service Segment: Managed IT Infrastructure, expected to hold 40.9% share in 2026

- Leading Deployment Model: Cloud deployment, projected to capture 61.4% market share in 2026

Investment activity across the industry is increasingly focused on AI-ready data centers, energy-efficient infrastructure, advanced cooling technologies, and hybrid cloud ecosystems. Hyperscale cloud providers and managed service companies are allocating significant capital toward high-density computing environments capable of supporting next-generation workloads.

Market Drivers

Rising Cloud Adoption and Workload Modernization Expand Market Opportunities

Cloud transformation has become one of the most significant drivers of managed data center services adoption. Enterprises across industries are increasingly migrating applications, databases, and business processes to cloud environments to improve flexibility, scalability, and operational efficiency.

Organizations are no longer relying solely on traditional data center models. Instead, they are adopting hybrid and multi-cloud architectures that combine private infrastructure with public cloud platforms. This shift has created demand for managed service providers capable of integrating diverse environments while maintaining security, availability, and performance.

Managed data center providers support enterprises throughout the cloud lifecycle, including migration planning, infrastructure deployment, monitoring, optimization, and ongoing management. Businesses are increasingly seeking unified operating models that provide visibility across legacy systems, private clouds, and public cloud platforms.

For example, enterprises operating complex ERP systems, customer platforms, and analytics environments require continuous optimization to maintain performance. Managed service providers help organizations automate infrastructure management, improve resource utilization, and reduce operational complexity.

As digital transformation initiatives continue across industries such as banking, healthcare, retail, manufacturing, and telecommunications, managed data center services are becoming a strategic component of enterprise IT strategies.

AI Adoption and Rising Energy Requirements Increase Demand for Expertise

Artificial intelligence is reshaping the data center industry by introducing highly intensive computing requirements. AI workloads require advanced processors, high-performance networking, greater storage capacity, and specialized cooling systems.

The rapid expansion of AI applications is increasing pressure on organizations to operate more efficient and resilient infrastructure. Traditional data center management approaches are often insufficient for handling AI-driven workloads, creating opportunities for managed service providers with specialized capabilities.

AI-enabled data centers require advanced monitoring, predictive maintenance, workload balancing, and energy optimization. Managed providers are increasingly using automation and artificial intelligence tools to improve operational efficiency and reduce downtime.

Energy consumption has also become a major concern. Data centers represent a growing portion of global electricity demand, leading governments and regulators to introduce stricter sustainability requirements. Enterprises are increasingly seeking providers that can demonstrate energy efficiency, carbon reduction strategies, and regulatory compliance.

Managed service providers are addressing these challenges through:

- AI-powered infrastructure monitoring

- Advanced cooling management

- Predictive maintenance systems

- Renewable energy integration

- Sustainability reporting solutions

As AI adoption accelerates, managed data center services are evolving from basic infrastructure support into strategic technology enablement platforms.

Market Restraints

Cost Pressures, Vendor Lock-In, and Infrastructure Complexity Challenge Adoption

Despite strong growth opportunities, several factors may limit market expansion. One major challenge is the significant investment required to establish and maintain advanced data center infrastructure.

Organizations adopting managed services must consider costs associated with servers, networking equipment, storage systems, cooling infrastructure, and continuous technology upgrades. For smaller enterprises, these expenses can create barriers to adoption.

Vendor lock-in is another important concern. Long-term contracts, proprietary platforms, and limited interoperability can reduce flexibility and make it difficult for enterprises to switch providers. Migration between service providers can involve significant costs, operational disruption, and data transfer challenges.

Additionally, managing complex hybrid environments requires careful coordination between internal IT teams and external service providers. Enterprises must evaluate providers based on security capabilities, scalability, compliance support, and integration expertise.

Although managed services reduce operational burdens, organizations need effective vendor management strategies to maximize long-term value.

Market Opportunities

Security-Focused Managed Services Create High-Growth Potential

Cybersecurity concerns are becoming a major catalyst for managed data center service adoption. The increasing frequency of ransomware attacks, identity-related threats, and AI-powered cyber risks has encouraged organizations to outsource security operations.

Modern enterprises require continuous monitoring and rapid threat response capabilities. Managed security service providers offer solutions such as:

- Security operations center (SOC) management

- Threat intelligence

- Identity and access management

- Incident response

- Compliance monitoring

Hybrid cloud environments have expanded the attack surface for organizations, making security management more complex. Businesses are increasingly adopting integrated solutions that combine infrastructure management, cloud security, and data protection.

Financial institutions, healthcare organizations, and government agencies are particularly investing in managed security services due to strict data protection requirements.

The growing demand for comprehensive cybersecurity solutions is expected to make security-focused managed services one of the fastest-growing areas within the market.

Sustainability and Regulatory Compliance Create New Growth Areas

Data center sustainability has become a critical business priority. Governments worldwide are introducing regulations focused on energy consumption, carbon emissions, and environmental transparency.

Organizations are increasingly required to measure and report their environmental impact while maintaining operational efficiency. Managed service providers are responding by offering solutions focused on:

- Energy monitoring

- Carbon tracking

- Infrastructure optimization

- Regulatory reporting

- Sustainable cooling systems

Enterprises are increasingly selecting providers that can deliver both operational reliability and measurable sustainability outcomes. This trend is creating new opportunities for managed service companies to differentiate through environmentally responsible solutions.

Segment Analysis

Managed IT Infrastructure Leads Service Type Segment

Managed IT infrastructure is expected to remain the dominant service category, accounting for approximately 40.9% market share in 2026.

This segment includes:

- Server management

- Storage administration

- Network management

- Virtualization

- Patch management

- Capacity planning

Enterprises outsource infrastructure management because maintaining complex IT environments requires specialized skills and continuous monitoring.

Large organizations in industries such as banking and telecommunications rely heavily on managed infrastructure providers to ensure high availability and uninterrupted operations.

Managed IT infrastructure also acts as a foundation for additional services. Organizations often expand contracts to include cloud management, disaster recovery, application support, and cybersecurity solutions.

Managed Security Services Experience Rapid Growth

Managed security services are expected to witness significant growth due to increasing cybersecurity threats and regulatory requirements.

Organizations are increasingly relying on external security experts to monitor infrastructure, identify threats, and respond to incidents.

For example, financial institutions use managed SOC services to detect fraudulent activity, while healthcare providers rely on managed security solutions to protect sensitive patient information.

As hybrid cloud adoption increases, security management becomes more complex, creating strong demand for specialized providers.

Deployment Model Analysis

Cloud Deployment Dominates Market Growth

Cloud deployment is expected to lead the managed data center services market, capturing approximately 61.4% share in 2026.

Cloud-based managed services offer several advantages:

- Flexible resource allocation

- Lower infrastructure costs

- Faster deployment

- Scalability

- Improved operational efficiency

Businesses with fluctuating workloads increasingly rely on managed cloud platforms to adjust computing resources based on demand.

For example, e-commerce companies use managed cloud infrastructure to scale operations during high-demand periods without investing in permanent infrastructure.

Enterprises migrating legacy systems to cloud platforms also depend on managed service providers for application migration, performance optimization, and ongoing management.

Hybrid and On-Premise Models Maintain Importance

While cloud deployment dominates, on-premise and hybrid models continue to serve organizations with specific security, compliance, and latency requirements.

Government organizations, defense companies, and highly regulated industries often maintain private infrastructure to retain control over sensitive data.

Hybrid environments are becoming increasingly common, allowing enterprises to combine private infrastructure with public cloud resources.

Managed service providers play a crucial role in managing these complex environments by ensuring seamless integration, security, and performance.

Regional Analysis

North America Managed Data Center Services Market

North America is expected to maintain market leadership, accounting for 34.1% share in 2026.

The region benefits from:

- Advanced digital infrastructure

- Strong cloud adoption

- Presence of major technology companies

- High enterprise demand

Companies such as IBM, Microsoft, Amazon Web Services, and Google Cloud continue investing heavily in AI-ready infrastructure.

The U.S. remains the primary growth contributor due to large-scale investments in artificial intelligence, cloud computing, and high-performance data centers.

Companies including Digital Realty and Equinix are expanding high-density facilities to support AI workloads and hybrid cloud connectivity.

Increasing focus on energy efficiency and regulatory compliance is further strengthening demand for managed services.

Europe Market Trends

Europe represents a significant market driven by regulatory compliance and data sovereignty requirements.

The implementation of frameworks such as GDPR has increased demand for secure and compliant managed infrastructure solutions.

Countries including Germany, the U.K., France, and Spain are leading adoption due to strong digital transformation initiatives.

Providers such as OVHcloud, Capgemini, and Atos are expanding their managed service offerings to support sovereign cloud and enterprise modernization strategies.

Asia Pacific Market Trends

Asia Pacific is projected to be the fastest-growing region, supported by a CAGR of approximately 15.1%.

Growth drivers include:

- Rapid digital transformation

- Expanding cloud adoption

- Rising internet penetration

- Large-scale infrastructure investments

Countries including China, India, Japan, and Southeast Asian markets are witnessing strong demand for managed services.

Hyperscalers such as Amazon Web Services, Microsoft Azure, and Google Cloud are expanding regional data center capacity, creating opportunities for managed infrastructure providers.

The increasing need for local data residency, cybersecurity, and scalable infrastructure is expected to accelerate market growth across the region.

Competitive Landscape

The managed data center services market is moderately fragmented, with global technology companies, infrastructure specialists, and regional providers competing through innovation, service quality, and geographic expansion.

Companies are increasingly focusing on:

- AI-driven automation

- Hybrid cloud management

- Security integration

- Sustainability solutions

- Global infrastructure expansion

Recent industry developments highlight increasing consolidation and partnerships aimed at strengthening hybrid cloud capabilities.

In February 2025, IBM completed its acquisition of HashiCorp to enhance hybrid cloud automation and infrastructure management capabilities.

In June 2025, Equinix expanded its Southeast Asian presence through the acquisition of three data centers in Manila, strengthening regional digital infrastructure capabilities.

Key Companies Covered

- IBM

- Kyndryl

- DXC Technology

- NTT DATA

- Accenture

- Capgemini

- Hewlett Packard Enterprise

- Dell Technologies

- Cisco

- Rackspace Technology

- Equinix

- Digital Realty

- Oracle

- Schneider Electric

- Fujitsu

- Tata Consultancy Services

Future Outlook

The managed data center services market is expected to experience sustained growth through 2033 as enterprises increasingly prioritize scalability, security, automation, and operational efficiency.

The combination of AI adoption, cloud transformation, cybersecurity requirements, and sustainability regulations will continue reshaping the industry. Service providers that can deliver integrated, intelligent, and environmentally efficient solutions will gain a competitive advantage.

As organizations move toward complex hybrid and multi-cloud environments, managed data center services will become increasingly essential for maintaining reliable, secure, and optimized digital infrastructure.