Integrated UPS Market Overview

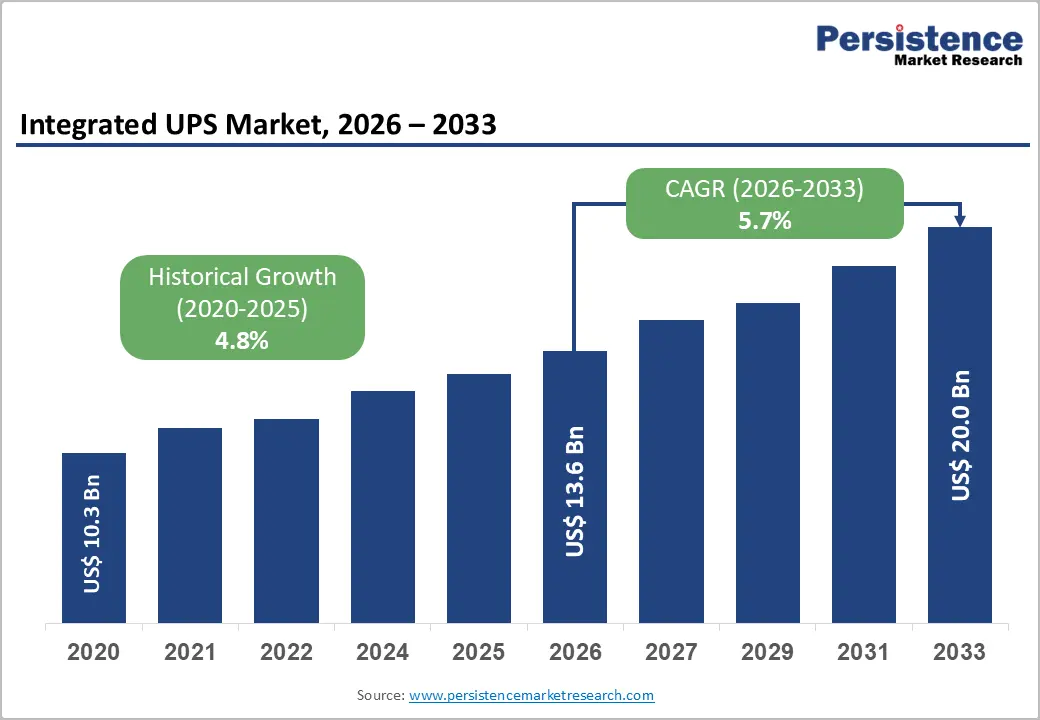

The global Integrated UPS market size is projected to reach US$ 13.6 billion in 2026 and is expected to expand to US$ 20.0 billion by 2033, registering a CAGR of 5.7% between 2026 and 2033. The market recorded a historical growth rate of approximately 4.8% CAGR from 2020 to 2025, reflecting steady adoption of uninterrupted power protection solutions across industries.

The increasing dependence on digital infrastructure, cloud computing, artificial intelligence (AI), and connected technologies has significantly increased the need for reliable power supply systems. Data centers, healthcare facilities, financial institutions, telecommunications networks, and industrial automation environments require continuous power availability to prevent downtime, data loss, and operational disruptions.

Integrated UPS systems have become a critical component of modern power management infrastructure by combining power conditioning, backup capabilities, monitoring systems, and intelligent energy management into a unified solution. As organizations prioritize operational resilience and energy efficiency, demand for advanced UPS technologies is expected to accelerate throughout the forecast period.

North America currently dominates the global Integrated UPS market, accounting for nearly 39% market share, supported by extensive data center development, stringent power reliability standards, and strong adoption across IT, BFSI, and healthcare sectors. Meanwhile, Asia Pacific represents the fastest-growing regional market, expanding at a CAGR of 7.1%, driven by rapid digital transformation, 5G deployment, and large-scale investments in data center infrastructure.

Key Market Drivers

Expansion of Data Center Infrastructure Accelerating UPS Adoption

The rapid growth of global data centers is one of the primary factors driving the Integrated UPS market. The increasing adoption of cloud computing, artificial intelligence workloads, enterprise digitization, and digital services has resulted in unprecedented demand for high-performance computing infrastructure.

According to energy industry assessments, global data centers consumed approximately 200–250 TWh of electricity in 2022, and consumption is expected to rise significantly by 2026 due to expanding AI applications and hyperscale facilities. Companies including Microsoft, Amazon Web Services, Google, and Meta are investing billions of dollars in new data center campuses across major markets.

Data centers require highly reliable power protection systems to maintain uptime and prevent service interruptions. Integrated UPS solutions provide essential protection against power failures, voltage fluctuations, frequency disturbances, and electrical noise. These capabilities are particularly important for Tier III and Tier IV data centers, where even short interruptions can result in significant financial losses.

The increasing deployment of edge computing facilities and colocation data centers is also creating additional demand for compact and modular UPS systems. As organizations move toward decentralized computing models, integrated UPS solutions are becoming essential for maintaining reliable power across distributed infrastructure networks.

Rising Power Grid Instability Supporting Market Growth

Increasing power disruptions and grid reliability challenges are encouraging organizations to invest in advanced UPS systems. Extreme weather events, aging electrical infrastructure, and rising electricity demand are contributing to more frequent power interruptions across several regions.

In developed economies, industries are increasingly focused on improving power quality and reducing downtime risks. In emerging markets, where grid stability remains a challenge in several locations, businesses are adopting UPS systems to ensure uninterrupted operations.

Industries such as banking, healthcare, manufacturing, and telecommunications depend heavily on continuous electricity availability. Integrated UPS systems enable these sectors to maintain operations during power failures while protecting sensitive electronic equipment.

As digital dependence increases globally, businesses are becoming less tolerant of downtime, creating sustained demand for reliable backup power solutions.

Market Restraints

High Initial Investment Costs Limiting Adoption

Despite strong demand, high upfront investment remains a significant challenge for Integrated UPS market expansion. Advanced UPS systems, particularly online double-conversion and industrial-scale solutions, require substantial capital expenditure.

Large-capacity UPS systems can cost from several thousand dollars to hundreds of thousands of dollars depending on configuration, power rating, battery technology, and installation requirements. Additional expenses associated with infrastructure modifications, maintenance, and commissioning further increase ownership costs.

Small and medium-sized enterprises often hesitate to invest in premium UPS solutions due to budget limitations. In price-sensitive markets, organizations may continue using conventional backup systems despite the operational advantages offered by integrated UPS technologies.

Battery replacement requirements also contribute to long-term costs, as traditional lead-acid batteries typically require replacement every three to five years.

Battery Management and Environmental Concerns

Battery lifecycle management remains another challenge affecting market development. Lead-acid batteries continue to represent a major portion of installed UPS systems but require proper recycling and disposal procedures due to environmental concerns.

Regulations such as the European Union Battery Regulation are increasing pressure on manufacturers and end users to adopt sustainable battery management practices.

Although lithium-ion batteries offer advantages such as higher energy density, longer lifespan, and reduced maintenance, their adoption is affected by higher costs and supply chain challenges related to lithium and cobalt availability.

The development of efficient recycling infrastructure and advancements in alternative battery technologies will play an important role in overcoming these challenges.

Emerging Opportunities

Modular UPS Systems Supporting Edge Computing and 5G Growth

The expansion of edge computing and 5G networks is creating significant opportunities for modular Integrated UPS systems. Unlike traditional centralized UPS systems, modular solutions provide scalability, flexibility, and easier capacity expansion.

As telecom operators deploy thousands of 5G base stations and edge nodes, compact and intelligent power backup solutions are becoming increasingly important.

According to industry projections, global 5G connections are expected to exceed 5 billion by 2030, creating demand for distributed infrastructure requiring reliable power protection.

Leading companies including Schneider Electric and Eaton are developing modular UPS solutions designed specifically for telecom networks, micro data centers, and edge computing environments.

These systems allow organizations to increase power capacity gradually based on demand, reducing initial investment requirements while improving operational efficiency.

Healthcare Digitalization Creating New Demand Opportunities

Healthcare digital transformation represents a major growth opportunity for the Integrated UPS market. Hospitals, diagnostic centers, research facilities, and telemedicine platforms increasingly rely on digital systems that require uninterrupted power availability.

Medical imaging equipment, electronic health records, laboratory systems, and critical monitoring devices cannot tolerate power interruptions. Integrated UPS systems help healthcare organizations maintain continuous operations while protecting sensitive medical equipment.

Global healthcare IT spending is projected to surpass US$ 390 billion by 2026, supporting increased investment in smart hospital infrastructure.

Regulatory requirements from organizations such as the World Health Organization (WHO) and healthcare accreditation bodies further emphasize the importance of reliable backup power systems.

Segment Analysis

Online Integrated UPS Systems Lead Product Segment

Online Integrated UPS systems represent the leading product category, accounting for approximately 45% of the market share.

These systems utilize double-conversion technology to provide continuous power protection by converting incoming AC power into DC and then back into clean AC output. This process eliminates voltage fluctuations, frequency variations, and electrical disturbances.

Online UPS systems are widely adopted in mission-critical applications including:

- Data centers

- Financial institutions

- Healthcare facilities

- Industrial automation environments

- Telecommunications networks

Their ability to provide zero transfer time during power failures makes them the preferred choice for applications requiring maximum reliability.

Rack-Mounted UPS Systems Dominate Configuration Segment

Rack-mounted Integrated UPS systems account for approximately 38% market share due to increasing demand from server rooms, enterprise data centers, and edge computing facilities.

These systems are designed to fit standardized IT racks, enabling efficient space utilization and simplified installation.

The adoption of technologies such as:

- Hyper-converged infrastructure (HCI)

- Software-defined networking (SDN)

- High-density computing platforms

is further increasing demand for compact UPS solutions.

Companies including APC by Schneider Electric and Eaton continue expanding rack-mounted UPS portfolios to address growing enterprise infrastructure requirements.

Double Conversion Technology Remains Market Leader

Double conversion technology represents around 42% of total technology revenue in the Integrated UPS market.

This technology provides complete electrical isolation from grid disturbances, ensuring consistent and high-quality power delivery.

Advancements in semiconductor technologies, including improved IGBT systems, have increased UPS efficiency levels beyond 96%, reducing energy losses and operational costs.

Double conversion UPS systems remain highly preferred in:

- Financial trading centers

- Pharmaceutical manufacturing

- High-performance computing facilities

- Large-scale data centers

Regional Market Insights

North America Leads Global Market

North America holds the largest share of the Integrated UPS market, representing nearly 39% of global revenue.

The United States remains the primary contributor due to its extensive data center ecosystem and strong presence of cloud service providers.

Growing AI infrastructure investments are increasing electricity demand from data centers, further supporting UPS adoption.

Regulations including:

- NFPA 110

- NEC Article 700

encourage organizations to maintain reliable emergency power systems.

Companies such as Vertiv, Eaton, and Schneider Electric continue investing in advanced UPS technologies across the region.

Asia Pacific Emerges as Fastest-Growing Market

Asia Pacific is expected to record the fastest growth during 2026–2033, expanding at a 7.1% CAGR.

Growth is driven by:

- China's East Data West Computing initiative

- India's Digital India program

- ASEAN data center expansion

- Rising cloud adoption

India has become a major investment destination, with annual digital infrastructure investments exceeding US$ 4 billion.

China, Japan, Singapore, Malaysia, and Indonesia are also witnessing rapid growth in data center capacity, telecom infrastructure, and smart manufacturing.

Europe Focuses on Energy Efficiency and Sustainability

Europe represents a significant Integrated UPS market supported by industrial automation, financial services, and data center expansion.

Countries including Germany, the UK, and France are driving regional demand.

The European Union’s energy efficiency regulations are encouraging replacement of older UPS systems with modern, energy-efficient solutions.

The increasing adoption of lithium-ion UPS technology aligns with sustainability goals under the European Green Deal.

Competitive Landscape

The global Integrated UPS market is moderately consolidated, with major players competing through technological innovation, product development, and strategic partnerships.

Leading companies include:

- Schneider Electric SE

- Eaton Corporation plc

- Vertiv Holdings Co.

- ABB Ltd.

- Emerson Electric Co.

- Siemens AG

- Delta Electronics, Inc.

- Huawei Technologies Co., Ltd.

- Mitsubishi Electric Corporation

- Toshiba Corporation

Companies are focusing on:

- Lithium-ion battery integration

- IoT-enabled monitoring

- Cloud-based energy management

- Higher efficiency UPS platforms

- Modular product development

Sustainability and intelligent power management are becoming key competitive factors as organizations seek energy-efficient infrastructure solutions.

Recent Industry Developments

March 2025: Schneider Electric launched the APC Smart-UPS Ultra series featuring integrated lithium-ion batteries and EcoStruxure IT cloud monitoring capabilities for enterprise and hyperscale data centers.

November 2024: Vertiv expanded its Liebert EXL S1 modular UPS portfolio with higher-capacity configurations targeting large-scale data center deployments.

January 2024: Eaton introduced an upgraded 9PX Gen 2 UPS series featuring lithium-ion battery options and cybersecurity enhancements for critical infrastructure applications.

Integrated UPS Market Outlook 2026–2033

The Integrated UPS market is expected to experience steady expansion as organizations increasingly prioritize uptime, operational resilience, and energy efficiency. The continued growth of cloud computing, AI infrastructure, smart healthcare facilities, and 5G networks will remain the primary catalysts for market development.

While high installation costs and battery management challenges may restrict adoption among smaller organizations, advancements in modular UPS architecture, lithium-ion technology, and intelligent monitoring systems are expected to create new growth opportunities.

With increasing dependence on digital infrastructure worldwide, Integrated UPS systems will continue to play a vital role in ensuring reliable, secure, and uninterrupted power delivery across critical industries.