Silicon Anode Battery Market Overview

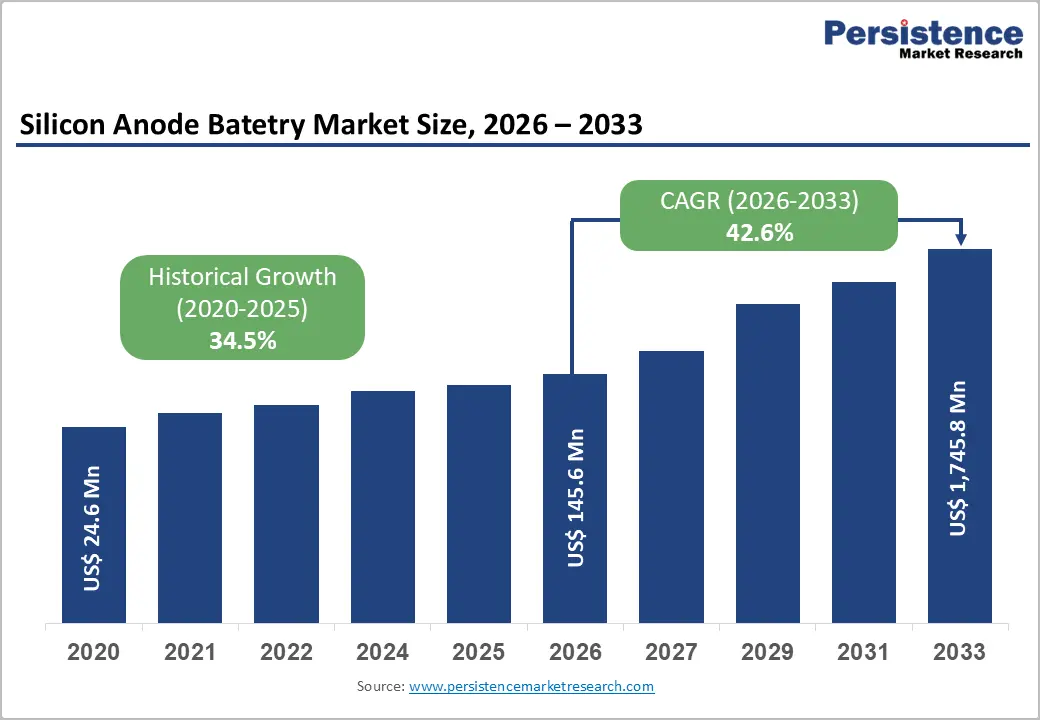

The global silicon anode battery market is entering a high-growth phase as demand accelerates for next-generation energy storage solutions capable of delivering higher energy density, faster charging, and improved performance compared with traditional lithium-ion batteries. The market size is expected to reach US$145.6 million in 2026 and is projected to expand to US$1,745.8 million by 2033, growing at an impressive CAGR of 42.6% between 2026 and 2033.

The rapid expansion of electric vehicles (EVs), advanced consumer electronics, renewable energy storage systems, and unmanned aerial systems is driving the adoption of silicon-based anode technologies. Conventional lithium-ion batteries rely heavily on graphite anodes, which have reached practical limitations in energy storage capacity. Silicon anodes provide a transformative alternative due to their ability to store significantly more lithium ions, offering nearly 10 times higher theoretical capacity than graphite.

With increasing pressure from automotive manufacturers, technology companies, and governments to improve battery performance while reducing charging times and carbon emissions, silicon anode batteries are becoming a critical technology for the future of electrification.

Silicon Anode Battery Market Size and Forecast

The silicon anode battery market is witnessing rapid commercialization as battery manufacturers transition from laboratory-scale innovations toward mass production. The market is expected to generate an incremental opportunity of approximately US$1.6 billion between 2026 and 2033, supported by investments in advanced battery materials and manufacturing infrastructure.

The global electric vehicle industry remains the largest demand generator. According to the International Energy Agency (IEA), global electric car sales surpassed 20 million units in 2025, representing more than one-fifth of worldwide vehicle sales. This rapid EV adoption is increasing demand for batteries that provide longer driving ranges, reduced charging times, and improved efficiency.

Silicon anode technology addresses these requirements by enabling higher energy density battery cells without significantly increasing battery pack size. As automakers continue developing long-range electric vehicles and high-performance models, silicon-enhanced lithium-ion batteries are expected to become increasingly integrated into future vehicle platforms.

Key Market Highlights

Asia Pacific Leads the Global Market

Asia Pacific dominates the silicon anode battery market, accounting for approximately 44% market share in 2025. The region benefits from its strong battery manufacturing ecosystem, large-scale electric vehicle adoption, and significant investments from leading battery producers.

China remains the largest contributor due to its position as the world’s leading EV market. The country recorded approximately 11 million electric vehicle sales in 2024, supported by government incentives, domestic battery production capacity, and aggressive electrification strategies.

Major battery companies in China, Japan, and South Korea are investing heavily in silicon-carbon anode materials to strengthen their position in the next generation of battery technologies.

North America Emerges as the Fastest-Growing Region

North America is projected to experience the fastest growth through 2033, supported by government incentives, domestic battery manufacturing initiatives, and increasing commercialization of silicon anode technologies.

The United States has become a major innovation hub, with companies including:

- Sila Nanotechnologies

- Group14 Technologies

- Amprius Technologies

- Enovix Corporation

- NanoGraf Corporation

playing significant roles in advancing silicon battery development.

Government programs such as the Inflation Reduction Act (IRA) and Department of Energy battery initiatives are encouraging domestic battery production and reducing dependence on overseas supply chains.

Sila Nanotechnologies’ Moses Lake facility represents a major milestone, targeting large-scale silicon anode material production capacity to support automotive and electronics applications.

Market Drivers

Rising Electric Vehicle Adoption Accelerating Silicon Anode Demand

The rapid expansion of electric mobility is the strongest growth driver for silicon anode batteries. Automakers worldwide are seeking battery technologies that can increase vehicle range while reducing weight and improving charging speed.

Traditional graphite anodes limit battery improvements because of their lower lithium storage capacity. Silicon anodes provide a theoretical capacity of approximately 3,600 mAh/g compared with graphite’s 372 mAh/g, enabling substantially higher energy storage potential.

This advantage allows manufacturers to:

- Increase EV driving range

- Reduce battery pack size

- Improve charging performance

- Lower vehicle weight

- Enhance overall efficiency

Leading automotive companies are increasingly partnering with silicon battery developers to secure future battery supply. Companies such as Mercedes-Benz and other global OEMs have invested in advanced silicon anode partnerships to support next-generation electric vehicles.

Advancements in Silicon-Carbon Composite Technologies

Historically, silicon anode adoption was limited by technical challenges, particularly silicon’s tendency to expand by up to 300% during charging cycles. This expansion creates mechanical stress, electrode cracking, and reduced battery lifespan.

Recent innovations in silicon-carbon composite materials are helping overcome these challenges.

Companies such as:

- Group14 Technologies

- Sila Nanotechnologies

- Nexeon

- Amprius Technologies

have developed advanced silicon architectures designed to improve cycle stability and commercial viability.

Modern silicon-carbon composites provide:

- Higher energy density

- Improved cycle life

- Better structural stability

- Faster charging capability

In 2025, BASF and Group14 Technologies introduced a silicon-carbon composite solution capable of achieving 80% state of charge in less than five minutes, demonstrating the technology’s growing commercial readiness.

Market Restraints

High Production Costs Limiting Mass Adoption

Despite strong technological advantages, silicon anode batteries currently face cost challenges compared with conventional graphite-based batteries.

Manufacturing advanced silicon materials requires:

- Complex production processes

- Specialized equipment

- Strict quality control

- Higher raw material investments

Battery costs remain a critical factor for EV manufacturers because battery packs represent approximately 30–40% of vehicle production costs.

Until manufacturers achieve higher production volumes and economies of scale, silicon anode batteries are likely to remain concentrated in premium EVs, aerospace applications, and high-performance electronics.

Technical Challenges Related to Battery Longevity

Silicon expansion remains one of the biggest technical barriers affecting widespread adoption.

Repeated expansion and contraction during charging cycles can lead to:

- Electrode degradation

- Reduced capacity retention

- Shortened battery lifespan

Automotive manufacturers require batteries capable of maintaining performance for 8–10 years or 100,000–150,000 miles, making durability a critical qualification factor.

Although composite materials have significantly improved performance, extensive real-world testing is still required before silicon anode batteries achieve widespread adoption across mass-market vehicles.

Emerging Market Opportunities

Unmanned Aerial Systems and Defense Applications

The unmanned aerial systems (UAS) sector represents a promising high-value opportunity for silicon anode battery manufacturers.

Drones and defense systems require extremely high energy density because every additional gram affects flight duration and operational efficiency.

Silicon anode batteries provide advantages including:

- Higher energy-to-weight ratio

- Longer flight times

- Improved operational capability

Companies such as Amprius Technologies have developed silicon nanowire batteries delivering energy densities exceeding 300 Wh/kg, making them suitable for aerospace applications.

Defense organizations are also supporting silicon battery development. NanoGraf Corporation received funding from the U.S. Department of Defense to develop advanced portable battery solutions.

Household Energy Storage Growth

Residential energy storage is another emerging opportunity for silicon anode batteries.

The expansion of renewable energy installations, particularly solar power, is increasing demand for compact and efficient energy storage systems.

Silicon anode batteries can enable:

- Smaller residential storage units

- Higher storage capacity

- Improved installation flexibility

As electricity grids increasingly integrate renewable sources, advanced battery technologies will become essential for energy independence and grid stability.

Segment Analysis

Cylindrical Cells Lead Battery Cell Type Segment

Cylindrical cells represent the leading segment, accounting for approximately 42% market share in 2025.

Their dominance is supported by:

- Established manufacturing infrastructure

- Mechanical strength

- Better resistance against silicon expansion

- Compatibility with automotive battery production

Companies such as Panasonic and Amprius Technologies are actively developing silicon anode cylindrical cells for automotive and aerospace applications.

Pouch cells are expected to experience faster growth due to increasing demand from smartphones, wearable devices, and flexible battery designs.

Less Than 2,000 mAh Batteries Dominate Capacity Segment

The less than 2,000 mAh segment accounted for approximately 47% market share in 2025.

Demand is driven by:

- Wearable devices

- Wireless earbuds

- Medical electronics

- Compact consumer devices

Silicon anodes provide significant advantages in small devices where manufacturers need longer battery life without increasing product size.

The 2,000–5,000 mAh segment is expected to grow rapidly due to adoption in smartphones, power tools, and electric mobility applications.

End-User Analysis

Electric Vehicles Remain the Largest Application Segment

Electric vehicles represent the leading end-user category, contributing approximately 46% market share in 2025.

The demand is fueled by:

- Consumer expectations for longer range

- Faster charging requirements

- Government electrification policies

- Automotive battery innovation

Companies such as Enevate are developing silicon-based battery solutions capable of achieving extremely fast charging, addressing one of the biggest consumer concerns associated with EV adoption.

Consumer electronics represent the fastest-growing segment as smartphone and wearable manufacturers seek differentiation through improved battery performance.

Regional Market Outlook

Asia Pacific

Asia Pacific remains the largest silicon anode battery market due to:

- Strong battery manufacturing capabilities

- High EV penetration

- Government-supported research programs

China leads regional growth, while Japan continues to contribute through advanced battery engineering expertise from companies such as Panasonic.

India is also emerging as a future growth market through initiatives such as the Production Linked Incentive (PLI) scheme for advanced chemistry batteries.

Europe

Europe represents approximately 19% of the market in 2025, supported by:

- Strong EV adoption

- Battery sustainability regulations

- Domestic gigafactory investments

Germany remains the largest European market due to its automotive industry leadership.

The EU Battery Regulation, including digital battery passport requirements from 2027, is expected to encourage adoption of advanced battery technologies with improved traceability and performance.

North America

North America is positioned as the fastest-growing market through 2033.

Growth factors include:

- Domestic battery manufacturing investments

- Government incentives

- Strong startup ecosystem

- Automotive partnerships

The region’s silicon anode industry is transitioning from research-stage development toward commercial-scale manufacturing.

Competitive Landscape

The silicon anode battery market features a combination of established battery companies and innovative technology startups.

Key companies include:

- Amprius Technologies Inc.

- Sila Nanotechnologies Inc.

- Group14 Technologies Inc.

- Enovix Corporation

- Nexeon Ltd.

- NanoGraf Corporation

- Enevate Corporation

- Panasonic Energy Co., Ltd.

- Samsung SDI Co., Ltd.

- LG Energy Solution Ltd.

- StoreDot Ltd.

- OneD Battery Sciences

- Sicona Battery Technologies

Companies are focusing on:

- Strategic partnerships

- Intellectual property development

- Large-scale manufacturing

- Automotive supply agreements

Recent Industry Developments

November 2025: Umicore partnered with HS Hyosung Advanced Materials to develop silicon-carbon anode materials for EV batteries.

September 2025: Sila Nanotechnologies began operations at its automotive-scale silicon anode production facility in Washington.

May 2025: BASF and Group14 Technologies launched a silicon-carbon battery solution supporting rapid charging performance.

March 2025: Amprius Technologies delivered advanced silicon anode cells with 315 Wh/kg energy density to an electric mobility manufacturer.

January 2024: Enovix partnered with Group14 Technologies to integrate silicon-carbon composite materials into advanced battery architectures.

Future Outlook of Silicon Anode Battery Market

The silicon anode battery market is positioned for exceptional growth as industries transition toward higher-performance energy storage solutions. While cost and durability challenges remain, ongoing advancements in silicon-carbon composites, manufacturing processes, and battery engineering are rapidly improving commercial viability.

Electric vehicles will remain the primary growth engine, but consumer electronics, aerospace, defense, and residential energy storage will create additional demand opportunities.

With increasing investments from battery manufacturers, governments, and technology companies, silicon anode batteries are expected to become a foundational technology in the next generation of lithium-ion batteries, reshaping the global energy storage landscape between 2026 and 2033.